Andeans Macro Daily(Beta Mode)

Chile, Peru Equities Drop Despite Copper Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 39.35 | -1.25% |

| MSCI Peru | 82.93 | -1.71% |

| USD/COP | 3,432.15 | -0.31% |

| USD/CLP | 920.11 | +0.21% |

| USD/PEN | 3.41 | -0.35% |

| Copper | 6.18 | +1.85% |

| Gold | 4,066.70 | +0.90% |

| Brent Crude | 73.17 | -2.78% |

| Bitcoin | 59,336.45 | -0.65% |

| Colombia 10Y Govt Yield | - | - |

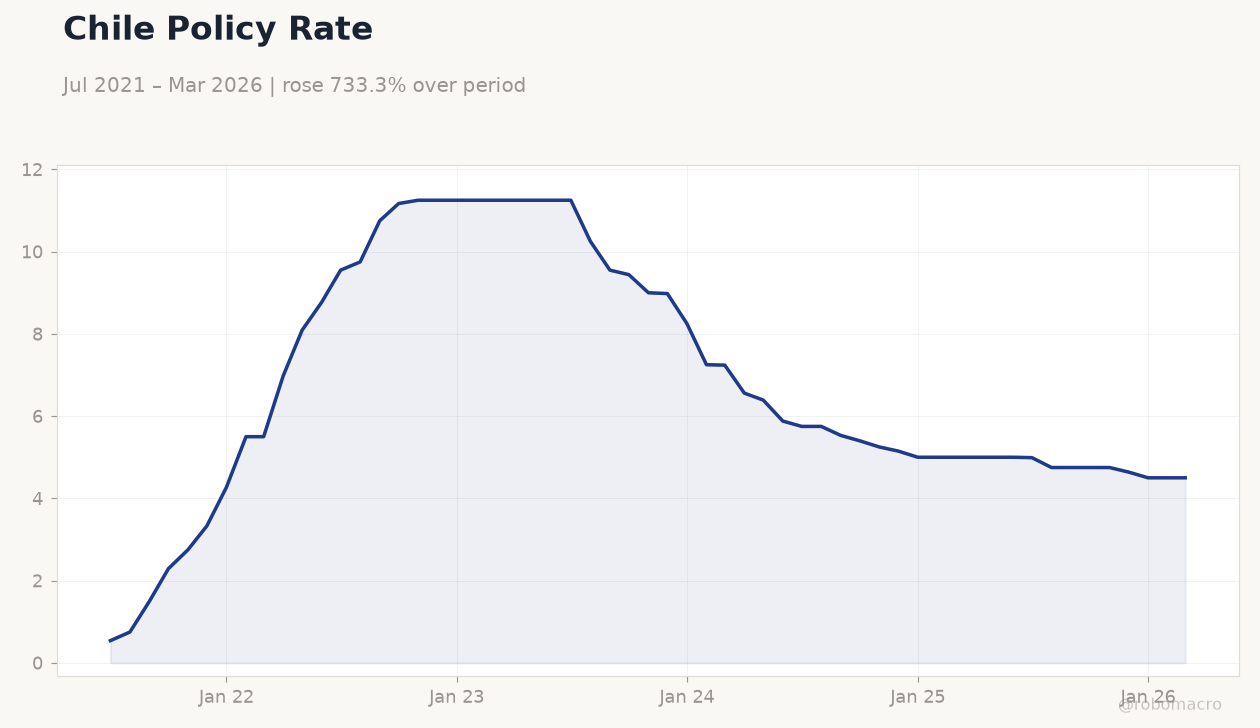

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Policy Rate | Type: macro_line | Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile fell 1.25% and MSCI Peru declined 1.71% as local equities faced selling pressure.

- Copper rose 1.85% to 6.18 while Brent crude dropped 2.78% to 73.17, widening commodity divergence.

- USD/CLP gained 0.21% while USD/COP eased 0.31% and USD/PEN fell 0.35%, reflecting mixed FX flows.

Yesterday's Recap

Andean equity markets closed lower on June 25. MSCI Chile dropped 1.25% to 39.35 amid broad regional equity weakness. MSCI Peru fell 1.71% to 82.93 despite firmer copper prices.

MSCI Colombia held steady at 9.02. Copper advanced 1.85% to 6.18, lifting mining-related revenues for Chile and Peru. USD/CLP rose 0.21% to 920.11 while USD/COP eased 0.31% to 3,432.15 and USD/PEN declined 0.35% to 3.41.

Gold climbed 0.90% to 4,066.70 and Brent crude fell 2.78% to 73.17, trimming Colombia’s oil-linked fiscal buffer. Chile’s short-term rate remained at 4.50%. No economic events were recorded in the region on June 25.

The Day Ahead

No major data releases are scheduled for June 26 across Colombia, Chile or Peru. Markets will track copper and oil price action for valuation cues. Chile’s mining sector remains sensitive to further copper gains that support fiscal revenue.

Peru’s trade balance will benefit from sustained metal prices. Colombia’s fiscal outlook stays tied to Brent levels near 73. Traders will monitor any BanRep or BCCh comments for policy hints.

ECB Deposit Rate stands at 2.25%.

Other Economic Notes

Copper strength at 6.18 bolsters Chile’s and Peru’s external accounts and FX reserve accumulation. Brent at 73.17 leaves Colombia’s fiscal position neutral with limited upside to COP. Gold at 4,066.70 offers modest support to Peru’s central bank reserves.

Regional equity underperformance contrasts with commodity gains, highlighting valuation compression in Chile and Peru. Lithium output trends in Chile continue to draw limited price reaction given elevated inventories. Eurozone Unemployment registered 6.70%.

Global Macro News

The IMF noted solid US growth and endorsed steady Fed rates, supporting a firmer dollar tone that weighed on some EM currencies. Chinese copper buyers signaled tolerance for higher prices under potential tariffs, underpinning the red metal. Korea’s household debt-to-GDP ratio exceeded the major-economy average, highlighting global leverage risks.

<i>↓ p.2</i>