Andeans Macro Daily(Beta Mode)

Copper Rally Lifts Chile, Peru Equities

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MSCI Colombia | 9.02 | +0.00% |

| MSCI Chile | 39.53 | +0.61% |

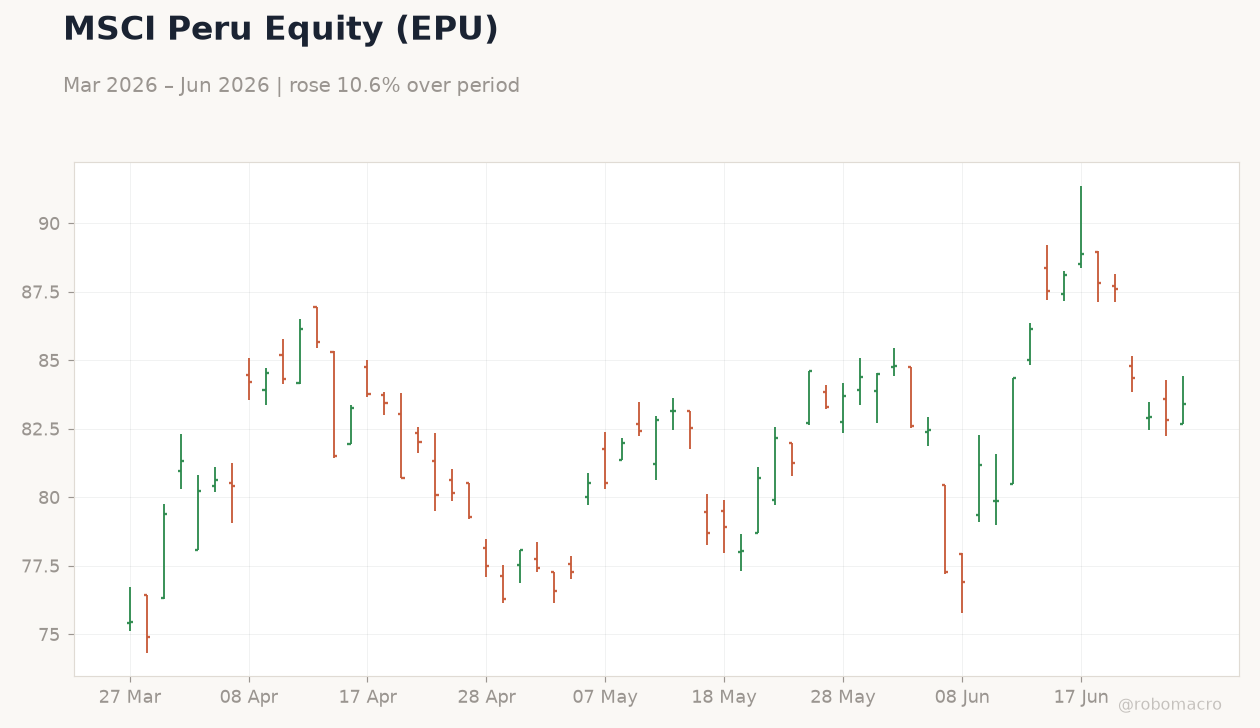

| MSCI Peru | 83.40 | +0.71% |

| USD/COP | 3,442.77 | -0.09% |

| USD/CLP | 921.85 | +0.22% |

| USD/PEN | 3.41 | -0.42% |

| Copper | 6.19 | +0.73% |

| Gold | 4,049.80 | -0.71% |

| Brent Crude | 72.95 | +1.33% |

| Bitcoin | 59,822.24 | +0.49% |

| Colombia 10Y Govt Yield | - | - |

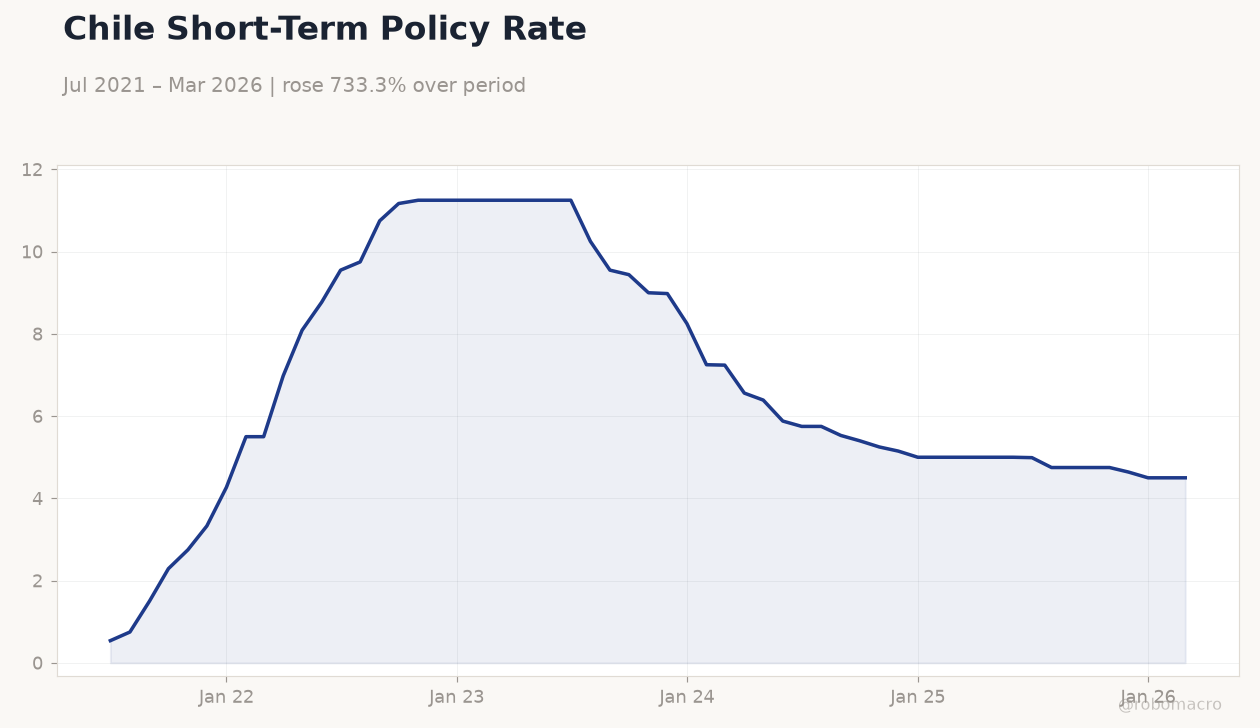

| Chile Short-term Rate | 4.50% | +0.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chile Short-Term Policy Rate | Type: macro_line | Chile Policy Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Chile Short-Term Policy Rate | Type: macro_line | Chile Policy Rate %: 4.5 (2026-03-01) | Range: 0.54–11.25 | Trend(5pt): 0.54,10.75,9,5,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI Chile and Peru advance on firmer copper prices while Colombia equities hold steady.

- USD/COP and USD/PEN ease modestly as Brent crude climbs above $72.

- BCCh policy rate stays at 4.50% with no immediate cut signals from recent data.

Yesterday's Recap

Andean equity markets posted selective gains on June 28. MSCI Chile rose 0.61% to 39.53 while MSCI Peru climbed 0.71% to 83.40, tracking a 0.73% advance in copper to $6.19 per pound. MSCI Colombia remained flat at 9.02.

In FX markets, USD/COP fell 0.09% to 3,442.77 and USD/PEN declined 0.42% to 3.41, supported by a 1.33% rise in Brent crude to $72.95. USD/CLP edged 0.22% higher to 921.85. Gold slipped 0.71% to $4,049.80, offering limited support to Peruvian miners.

Chile’s short-term rate held unchanged at 4.50%. No macroeconomic data releases occurred across the three countries. Chilean retail group Cencosud acquired Makro Colombia, while Canacol Energy secured a key restructuring decision from an Alberta court with Colombian consumer protections preserved.

The Day Ahead

Markets face a data-light session on June 30. Traders will monitor copper and oil price momentum for further direction in CLP and PEN. Colombian assets may respond to any updates on fiscal reform progress.

Regional equity flows could stay supported if metals prices hold gains. Central bank officials are not scheduled for public remarks. Liquidity conditions remain stable across Andean currencies.

Flagship Minerals advanced its Isidora gold project in Chile after completing pilot-scale metallurgical drilling.

Other Economic Notes

Copper strength continues to underpin fiscal revenues in Chile and Peru through higher mining royalties. Colombia benefits from elevated Brent prices via improved Ecopetrol cash flows and trade balances. Lithium output trends in northern Chile show no material shift.

Broader commodity price stability helps narrow projected current-account gaps in the region. Political developments in Colombia keep fiscal adjustment expectations in focus for investors. Midnight Sun expanded strike length at its Dumbwa copper project to 6.7 kilometres of near-surface mineralization.

Global Macro News

Firmer energy and industrial metals prices provide a supportive backdrop for Andean commodity exporters. The ECB deposit rate sits at 2.25%, keeping external financing conditions steady for emerging-market issuers. <i>↓ p.2</i>