Argentina Macro Daily(Beta Mode)

Merval Dips as USD/ARS Edges Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 2,570,733.00 | -0.36% |

| USD/ARS | 1,407.00 | +0.39% |

| YPF | 35.98 | +2.22% |

| MercadoLibre | 1,780.36 | +0.64% |

| Globant | 53.20 | +2.31% |

| Soybeans | 1,187.25 | +2.02% |

| Gold | 5,097.60 | +0.64% |

| Bitcoin | 70,646.09 | -0.28% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL index fell 0.36% amid cautious trading, while USD/ARS rose 0.39% reflecting ongoing peso pressures.

- Energy stocks like YPF gained 2.22% on Vaca Muerta optimism, offsetting broader equity declines.

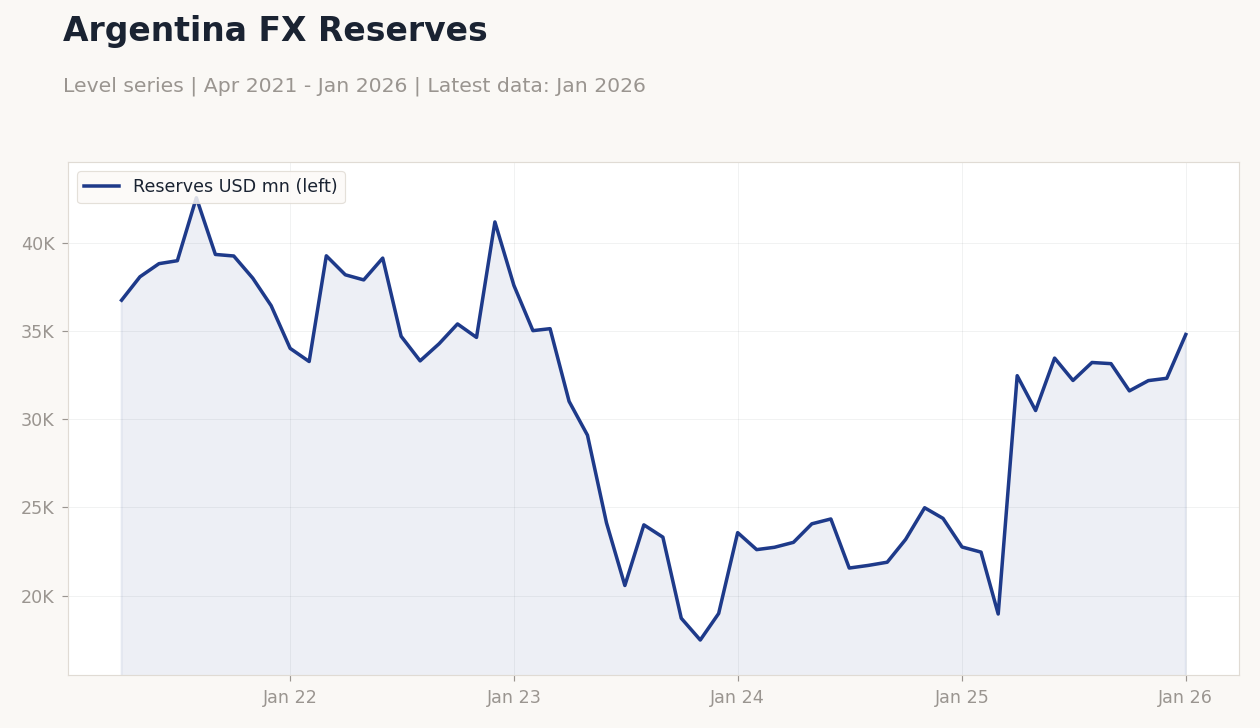

- Commodity boosts from soybeans (+2.02%) supported export outlooks, but BCRA reserve concerns lingered.

Yesterday's Recap

Argentine markets closed mixed on March 5, with the MERVAL index dropping 0.36% to 2,570,733 amid profit-taking after recent gains and global risk aversion. The USD/ARS official rate climbed 0.39% to 1,407, signaling mild depreciation under the crawling peg regime, while parallel rates likely widened the gap amid low FX liquidity. YPF shares rose 2.22% to 35.98, driven by positive Vaca Muerta shale developments and higher oil output reports, bolstering energy sector resilience.

MercadoLibre advanced 0.64% to 1,780.36 on e-commerce strength, and Globant surged 2.31% to 53.20, reflecting tech export momentum despite domestic challenges. Soybeans prices increased 2.02% to 1,187.25, aiding agricultural export revenues crucial for reserves. No major data releases occurred, but prior February CPI data at 8.2% YoY continued to influence sentiment, easing inflation fears.

Overall, bonds held steady with spreads stable, as markets eyed IMF compliance updates.

The Day Ahead

Today's calendar remains light with no scheduled economic releases or events for Argentina, allowing focus on ongoing BCRA FX interventions and parallel market dynamics. Traders will monitor any unscheduled announcements related to reserve management or capital controls amid persistent dollar shortages. Vaca Muerta project updates could emerge from industry sources, potentially impacting energy equities like YPF.

Attention may shift to global commodity trends, influencing soybean and gold prices key to export earnings. Broader peso stability will be watched closely, with any crawling peg adjustments signaling BCRA policy shifts. Markets anticipate quiet trading unless external shocks arise.

Other Economic Notes

Argentina's disinflation path shows progress with February CPI at 8.2% YoY, below expectations, driven by fiscal austerity and moderated food costs, though sustaining this amid wage pressures remains key. Vaca Muerta investments are accelerating industrial recovery, as January production rose 1.5% MoM, supporting GDP growth forecasts around 3% for 2026 despite external debt hurdles. IMF programme compliance is critical, with reserve targets under scrutiny to unlock further disbursements and ease capital controls.