Argentina Macro Daily(Beta Mode)

Merval Gains, Peso Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 2,866,257.00 | +0.90% |

| USD/ARS | 1,416.00 | +1.69% |

| YPF | 43.00 | +0.14% |

| MercadoLibre | 1,839.28 | +0.22% |

| Globant | 42.40 | -1.03% |

| Soybeans | 1,188.75 | +0.98% |

| Gold | 4,642.10 | -0.71% |

| Bitcoin | 76,823.60 | -0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

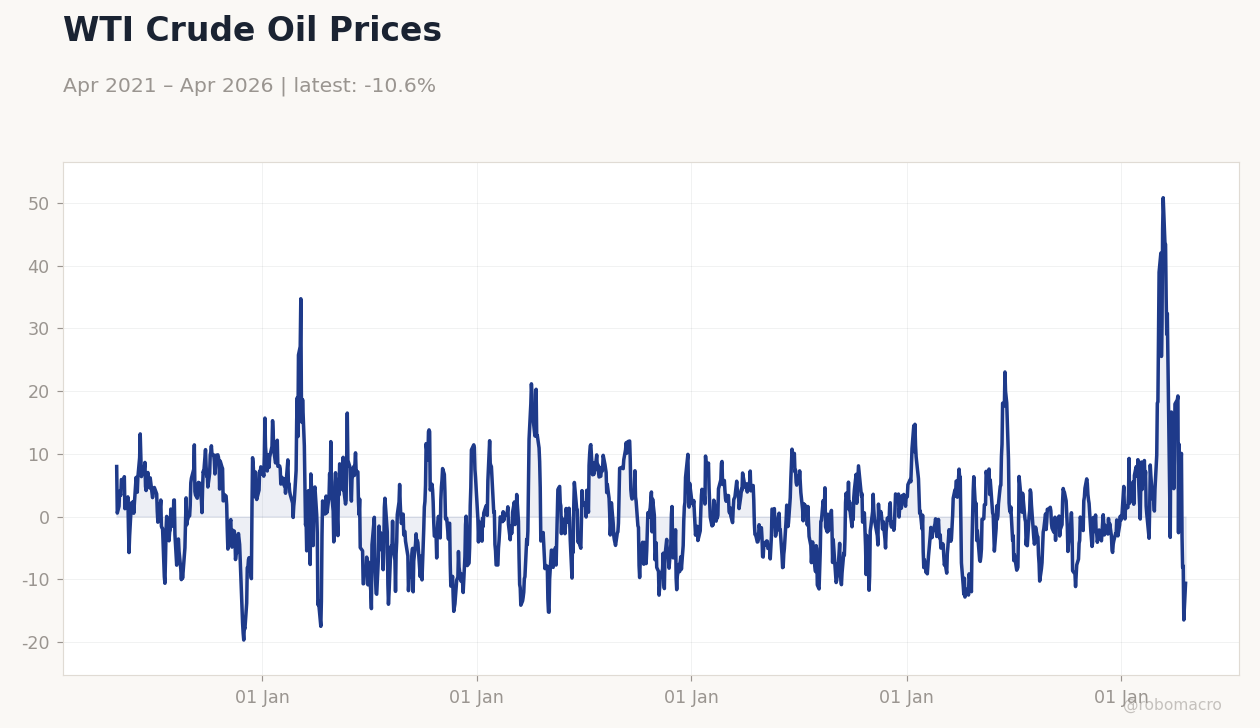

WTI Crude Oil Prices | Type: macro_line | WTI USD/bbl: -10.64 (2026-04-20) | Range: -19.68–50.81 | Trend(6pt): 7.973,-4.578,-2.666,9.522,-16.48,-10.64

WTI Crude Oil Prices | Type: macro_line | WTI USD/bbl: -10.64 (2026-04-20) | Range: -19.68–50.81 | Trend(6pt): 7.973,-4.578,-2.666,9.522,-16.48,-10.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Merval rose 0.90% to 2,866,257 amid commodity support, while USD/ARS surged 1.69% to 1,416 on depreciation pressures.

- YPF up 0.14% to 43.00 and soybeans +0.98% to 1,188.75, but Globant fell 1.03% to 42.40.

- Falklands tensions escalated with Argentina's claims and reports of potential US stance shift; asylum case adds headline noise.

Yesterday's Recap

Argentine markets displayed mixed results, with the Merval index advancing 0.90% to 2,866,257, supported by gains in select equities and broader commodity trends. The USD/ARS rate increased 1.69% to 1,416, underscoring ongoing peso weakness under the crawling peg and reserve dynamics. YPF shares gained 0.14% to 43.00, reflecting optimism around energy sector prospects, while MercadoLibre rose 0.22% to 1,839.28 amid e-commerce strength.

Globant dropped 1.03% to 42.40 due to tech sector pressures. Commodities offered backing, with soybeans up 0.98% to 1,188.75 boosting export outlooks, though gold declined 0.71% to 4,642.10 and Bitcoin fell 0.70% to 76,823.60. No significant data releases were reported, but headlines on Argentina's Falklands sovereignty push and a Mexican asylum seeker's case introduced geopolitical uncertainty without major market disruptions.

The Day Ahead

With no economic events on the calendar, focus shifts to potential BCRA updates on FX management or reserves amid recent peso movements. Geopolitical developments, including Falklands disputes and the asylum process for Fernando ‘N’, may generate headlines, though direct economic impacts appear limited. Traders could monitor global commodity prices, especially energy and agriculture, for influences on stocks like YPF.

Broader sentiment may track emerging market currency trends and any IMF-related commentary on Argentina's programme adherence.

Other Economic Notes

Argentina faces persistent challenges with currency stability and inflation under its IMF-backed reforms, as peso depreciation highlights vulnerabilities in the crawling peg system. Energy sector potential, including Vaca Muerta, supports export growth amid global demand. Geopolitical risks from the Falklands issue could weigh on investor confidence and foreign relations, potentially affecting capital flows.

Global Macro News

Emerging markets grapple with inflation and currency strains from oil shocks, as seen in the Philippines where the peso hit a record low of P61 per dollar, echoing Argentina's ARS pressures. (cont...)