Argentina Macro Daily(Beta Mode)

MERVAL Up, Risk at 523bp

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 2,747,310.00 | +0.33% |

| USD/ARS | 1,391.50 | -0.04% |

| YPF | 44.17 | +1.47% |

| MercadoLibre | 1,607.37 | +2.90% |

| Globant | 34.08 | +4.06% |

| Soybeans | 1,192.75 | +1.55% |

| Gold | 4,557.90 | -2.57% |

| Bitcoin | 80,578.86 | -0.58% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

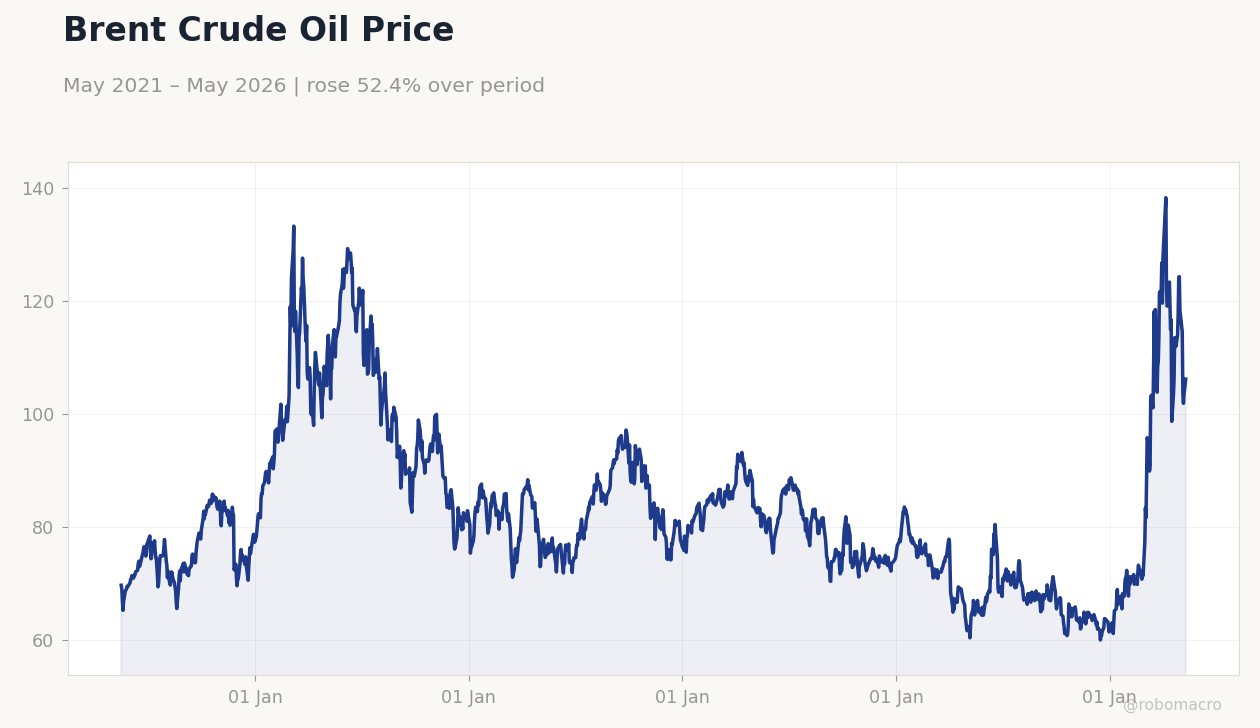

Brent Crude Oil Price | Type: macro_line | USD/bbl: 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(5pt): 69.62,107.2,83.66,76.23,106.1

Brent Crude Oil Price | Type: macro_line | USD/bbl: 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(5pt): 69.62,107.2,83.66,76.23,106.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL +0.33% to 2,747k amid ADR rally

- USD/ARS eases -0.04% to 1,391.50

- Country risk rises to 523bp; soybeans +1.55%

Yesterday's Recap

Argentina posted no data releases on May 14, leaving markets driven by global cues. The MERVAL index climbed 0.33% to 2,747,310, buoyed by energy and tech gains as Vaca Muerta sentiment held firm. YPF advanced 1.47% to 44.17 on steady crude prices, while MercadoLibre surged 2.90% to 1,607.37 and Globant jumped 4.06% to 34.08.

The official USD/ARS rate slipped 0.04% to 1,391.50, signaling contained FX pressures amid parallel rate stability. Soybeans rose 1.55% to 1,192.75, supporting agro export revenues critical for reserves. Gold tumbled 2.57% to 4,557.90 and Bitcoin fell 0.58% to 80,578.86, pressuring commodity-linked assets.

Country risk index stood at 523 basis points as of May 13 close, up 15bp from prior session lows.

The Day Ahead

Argentina's calendar remains empty on May 15, with no data or events scheduled. Tomorrow's docket is also blank, shifting focus to BCRA reserve updates and FX flows. Markets eye potential interventions if parallel spreads widen beyond 1,391.

Global commodities like soybeans will dictate exporter dollar inflows. Bank of Canada rate decision at 09:45 ET could sway CAD-linked soy trade dynamics.

Other Economic Notes

IMF staff-level talks in Buenos Aires near completion, with USD 8bn EFF contingent on 1.5% GDP primary surplus. Vaca Muerta shale output remains robust at ~500kb/d, bolstering energy FX earnings. Deregulation bill advances, eyeing soy export tax cuts to boost competitiveness.

Fiscal discipline underpins peso stabilization efforts.

Global Macro News

Bank of Canada holds rate announcement at 09:45 ET, with Business Outlook Survey at 11:30 ET; steady policy expected to support commodity demand via stable CAD. Market Participants Survey at 10:30 ET gauges inflation views, potentially influencing EM carry trades. Soybeans' 1.55% gain reflects China restocking, aiding Argentina's key export sector.

Gold's 2.57% drop signals risk-on flows, easing pressure on Argentine sovereign spreads. Bitcoin's mild decline underscores crypto volatility amid tighter global liquidity. <i>↓ p.2</i>