Argentina Macro Daily(Beta Mode)

Milei Loosens Peso Controls on Reserve Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,072,011.00 | +5.05% |

| USD/ARS | 1,412.00 | +0.11% |

| EUR/ARS | 1,636.16 | -0.32% |

| Gold | 4,429.20 | -0.41% |

| Brent Crude | 94.25 | -0.04% |

| Soybean | 1,193.00 | +0.65% |

| Bitcoin | 73,401.30 | -1.27% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

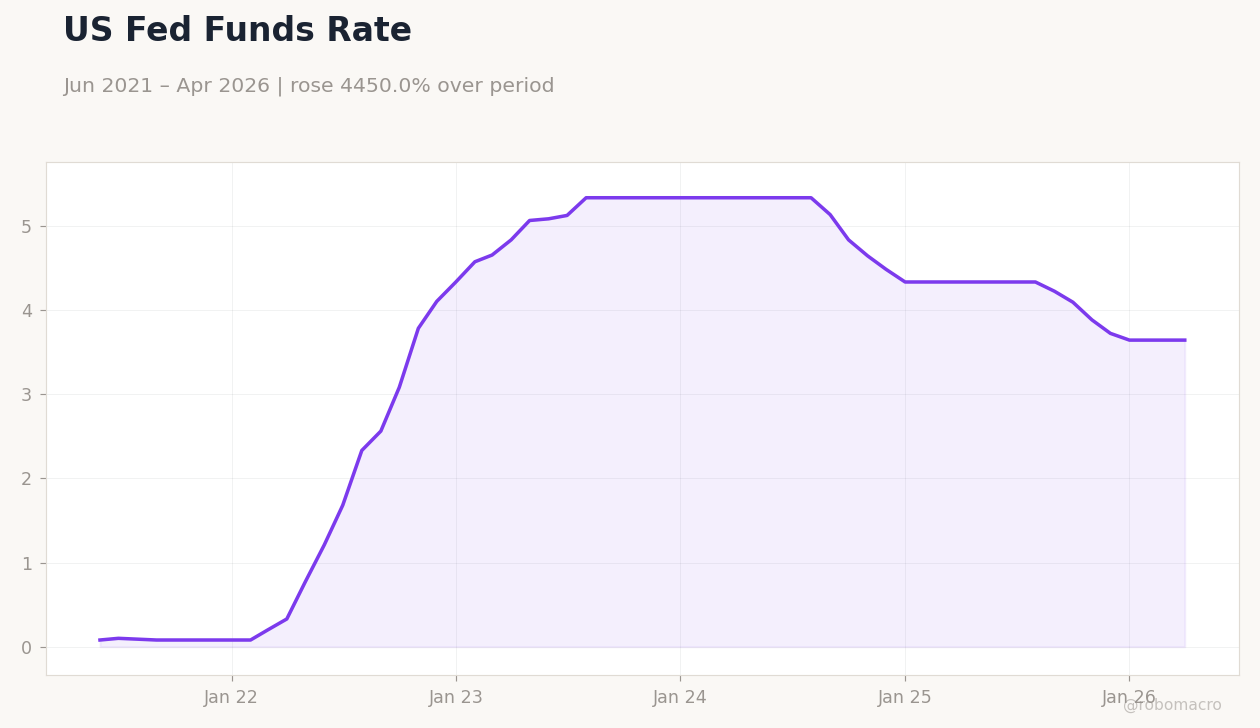

US CPI YoY | Type: macro_line | % YoY: 3.947 (2026-04-01) | Range: 2.325–8.979 | Trend(6pt): 5.296,8.223,3.251,2.871,3.32,3.947

US CPI YoY | Type: macro_line | % YoY: 3.947 (2026-04-01) | Range: 2.325–8.979 | Trend(6pt): 5.296,8.223,3.251,2.871,3.32,3.947

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BCRA reserves reach seven-year peak, enabling Milei to loosen peso controls and narrow parallel-market gaps.

- MERVAL surges 5.05% to 3,072,011 on deregulation optimism while USD/ARS rises 0.11% to 1,412.

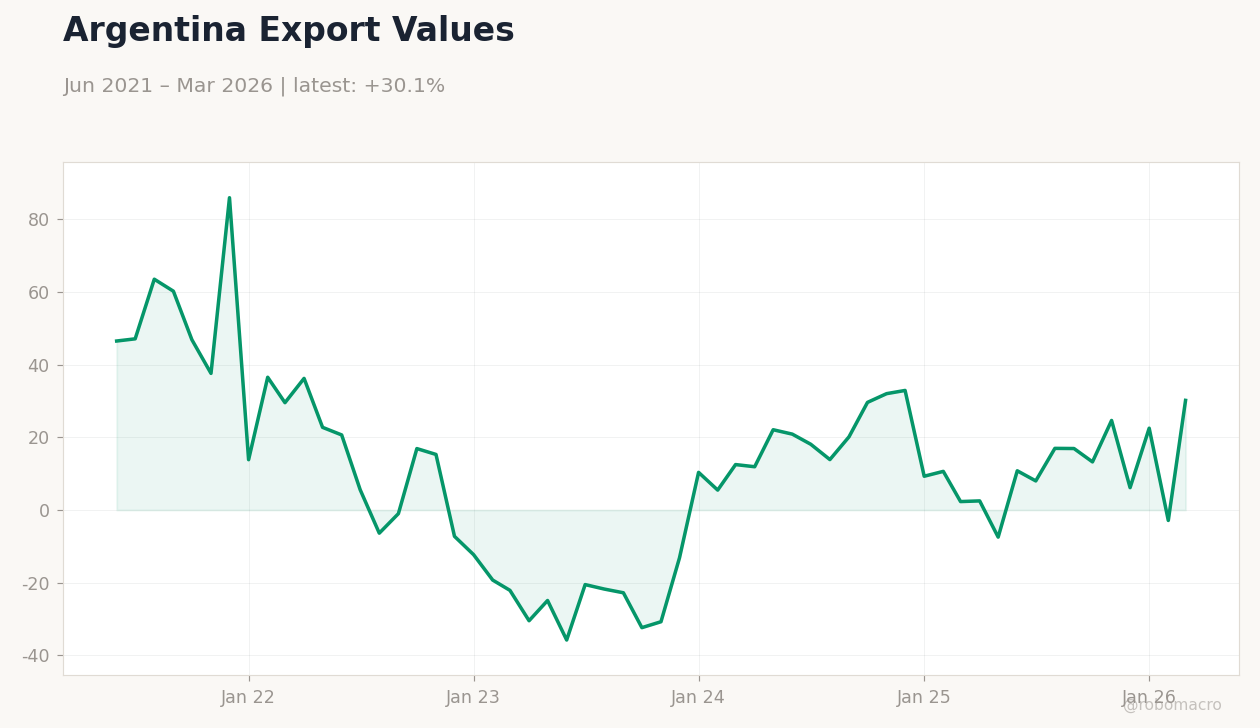

- Soybean prices climb 0.65% to 1,193 amid South American supply concerns, supporting export inflows.

Yesterday's Recap

Argentine markets advanced as President Milei signaled greater peso flexibility after central-bank reserves climbed to the highest level since 2019. The MERVAL posted a 5.05% gain, driven by energy and bank stocks on faster deregulation expectations. USD/ARS ticked up 0.11% to 1,412 while the euro-ARS cross eased 0.32%.

Brent crude held near 94.25 with minimal change, and gold slipped 0.41% to 4,429.20. No major data releases occurred, leaving focus on reserve accumulation and export proceeds. Soybean futures rose 0.65%, reinforcing the dollar-inflow narrative that underpins the policy shift.

The Day Ahead

Markets will monitor ongoing reserve data and any BCRA spot interventions after last week’s modest accumulation. Attention centers on soybean export registrations under the extended dólar agro program at the 1,300 rate. IMF staff discussions on the fifth review continue, with emphasis on subsidy reform pace and reserve targets.

No INDEC or BCRA releases are scheduled, shifting focus to global commodity prices and U.S.-Iran developments that could affect oil and risk sentiment. Traders will watch for further narrowing of the CCL-official gap.

Other Economic Notes

Segemar data show 26,142 identified mineral deposits despite only 20% of territory explored, highlighting untapped mining potential that could boost future exports. Fiscal primary balance recorded a modest April surplus aided by higher export duties. Industrial production remains in contraction territory, underscoring the need for sustained deregulation to revive activity.

The government’s decision to extend the export program through July aims to lock in an estimated 1.8 billion dollars in additional soybean and corn sales.

Global Macro News

Fresh U.S.-Iran tensions lifted oil prices and weighed on global equities, creating mixed signals for Argentine commodity exporters. South Korea and New Zealand central banks held rates as expected, reinforcing a cautious global policy backdrop. <i>↓ p.2</i>