Argentina Macro Daily(Beta Mode)

S&P Upgrade Lifts Argentina Bonds as Inflation Cools

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,353,008.00 | +6.34% |

| USD/ARS | 1,432.00 | -0.09% |

| EUR/ARS | 1,656.88 | +0.22% |

| Gold | 4,241.00 | +3.68% |

| Brent Crude | 86.48 | -4.32% |

| Soybean | 1,111.75 | -0.29% |

| Bitcoin | 63,419.52 | -0.22% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

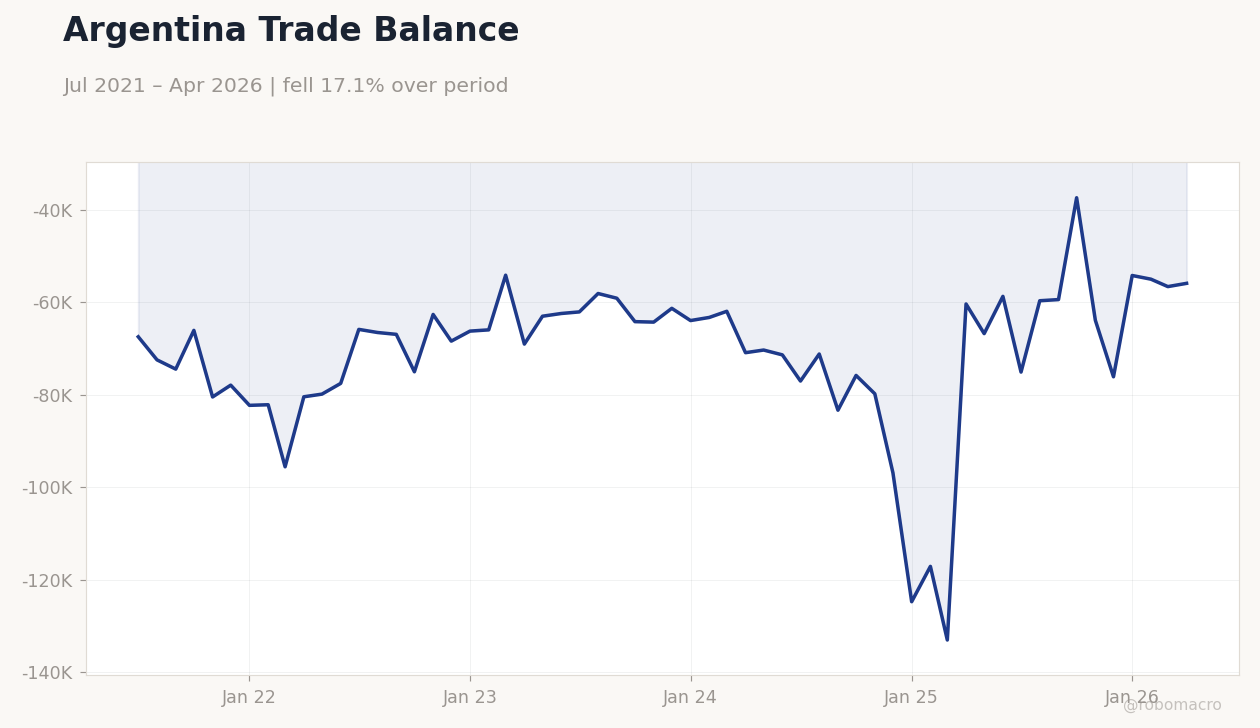

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- S&P lifts Argentina’s sovereign rating to B- citing fiscal adjustment and improved liquidity, sending 2035 bonds to record highs.

- May inflation reaches eight-month low, bolstering President Milei’s disinflation narrative and trimming rate-hike odds.

- MERVAL jumps 6.34% to 3,353,008 while USD/ARS slips 0.09% to 1,432 amid thin trading.

Yesterday's Recap

Argentina’s dollar bonds rallied after S&P upgraded the sovereign credit rating to B-. The 2035 notes hit a fresh record high as investors priced in stronger fiscal credibility and better external liquidity. MERVAL surged 6.34% to close at 3,353,008, extending its year-to-date advance.

USD/ARS eased 0.09% to 1,432 in quiet spot trading while EUR/ARS rose 0.22%. May inflation printed at its lowest level since September, reinforcing expectations that the BCRA’s current policy stance is now restrictive in real terms. Gold climbed 3.68% while Brent crude dropped 4.32%, reflecting shifting global risk sentiment.

The Day Ahead

No major Argentine data releases are scheduled for today. Markets will focus on any BCRA communications or reserve updates tomorrow. The weekly monetary-policy survey and trade-balance figures are due next week.

Investors continue to monitor IMF program compliance and potential CAF-IDB disbursements. Peso stability and soybean export proceeds remain the key domestic drivers.

Other Economic Notes

The government secured a $1.2 bn syndicated loan from CAF and IDB to cover 2026 financing needs. Fiscal primary surplus reached 0.9% of GDP in May, beating the IMF target. Industrial production posted its first positive year-on-year reading in 14 months.

Treasury placements of inflation-linked bonds attracted solid demand at a 7.8% real yield. These developments underscore ongoing fiscal consolidation and improving external buffers.

Global Macro News

The ECB raised rates for the first time since 2023 to counter Iran-war-related inflation pressures, tightening global financial conditions. Türkiye’s central bank kept its policy rate at 37% for a third consecutive meeting amid persistent price pressures. The Philippine peso strengthened to a one-month high while the Indian economy retained its status as the fastest-growing major market.

Commodity price swings, especially in gold and Brent, directly affect Argentina’s terms of trade and reserve accumulation. <i>↓ p.2</i>