Argentina Macro Daily(Beta Mode)

S&P Lifts YPF on Austerity, Reserves

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,352,708.00 | -0.01% |

| USD/ARS | 1,428.50 | -0.28% |

| EUR/ARS | 1,656.93 | -0.07% |

| Gold | 4,359.80 | +3.44% |

| Brent Crude | 83.06 | -4.89% |

| Soybean | 1,108.00 | -0.49% |

| Bitcoin | 65,945.81 | +0.36% |

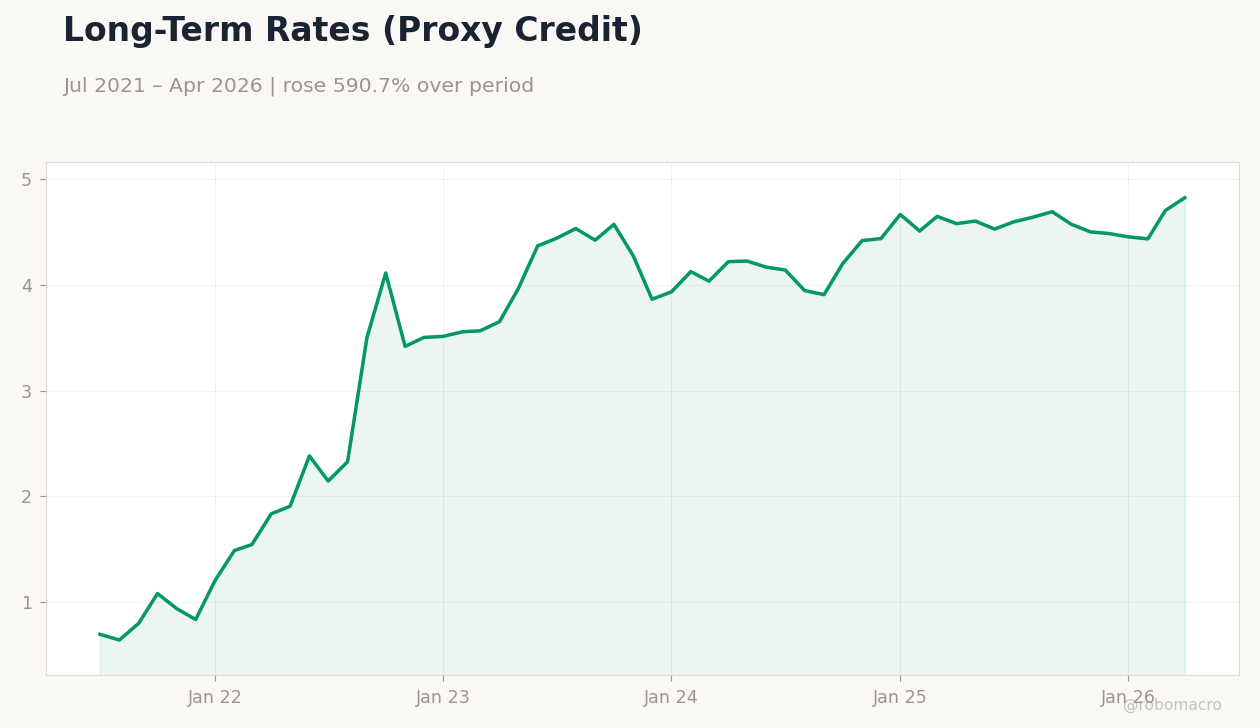

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

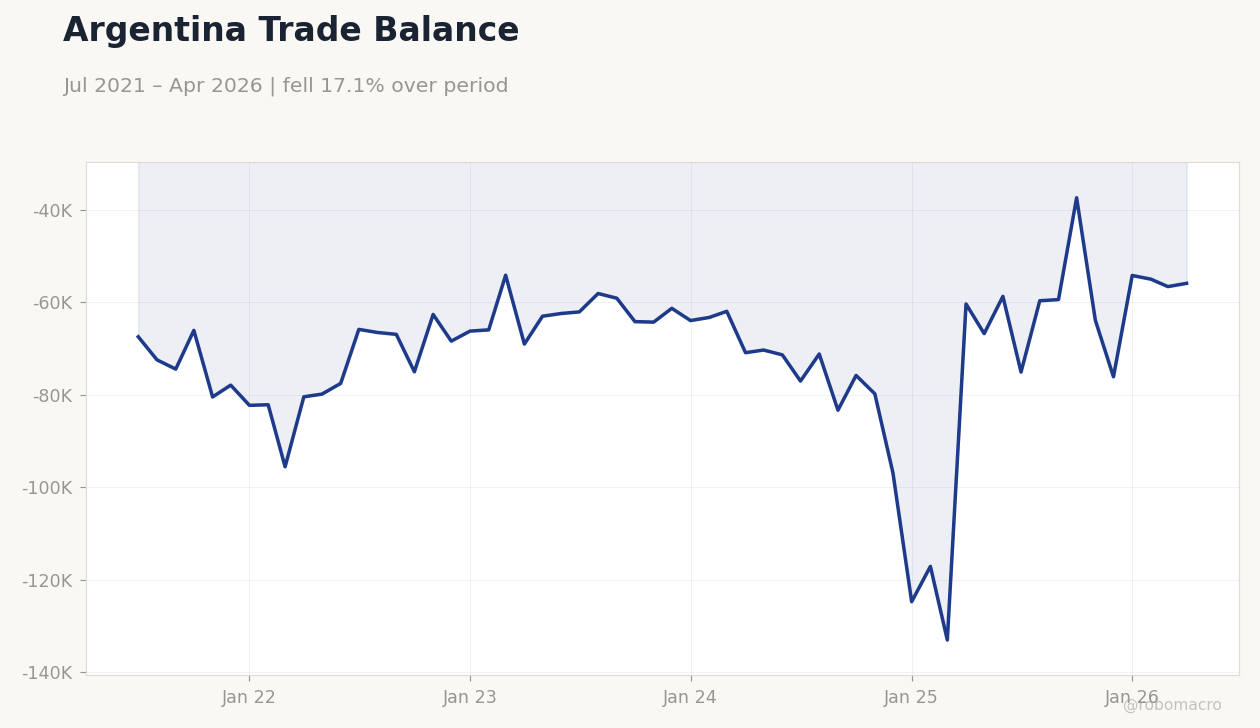

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- S&P raised ratings on YPF and seven other Argentine firms, citing fiscal discipline and BCRA reserve gains.

- MERVAL held steady at 3,352,708 while USD/ARS eased 0.28% to 1,428.50 on thin volumes.

- Brent Crude dropped 4.89% and soybeans fell 0.49%, weighing on export revenue prospects.

Yesterday's Recap

Argentine markets traded in narrow ranges with MERVAL slipping just 0.01%. The peso firmed modestly against the dollar as USD/ARS closed at 1,428.50. S&P’s upgrade of YPF and other credits highlighted ongoing primary surplus delivery and reserve accumulation at the BCRA.

IMPSA secured a hydroelectric contract in Venezuela, offering a modest boost to engineering exports. Gold rose 3.44% amid global safe-haven flows while Brent Crude declined sharply on higher OPEC+ supply signals. No major domestic data prints occurred, leaving investor focus on external drivers and fiscal execution.

Soybean prices edged lower, tempering near-term FX inflow expectations from the agricultural sector.

The Day Ahead

The calendar shows no scheduled Argentine releases or BCRA announcements. Traders will monitor global central bank meetings for spillovers into emerging-market yields. Attention remains on IMF amortization flows and any updates to reserve data.

Export registrations for soybeans and corn will provide the next visible read on FX supply. Markets expect quiet price action until external catalysts emerge later in the week.

Other Economic Notes

The government continues to post consecutive primary surpluses, supporting sovereign and corporate credit trajectories. Reserve gains have reduced immediate intervention pressure on the BCRA and improved net FX buffers. Fiscal-responsibility legislation advancing through Congress caps real spending growth, a step viewed positively by rating agencies.

Export competitiveness hinges on soybean and grain prices, which remain sensitive to Brazilian weather and global demand. External debt markets have priced in sustained austerity, narrowing spreads on Argentine paper.

Global Macro News

The ECB raised rates as Middle East tensions lifted inflation expectations across Europe. Bundesbank lowered its 2026 German GDP forecast to 0.5% while lifting its inflation projection to 2.9%. <i>↓ p.2</i>