Argentina Macro Daily(Beta Mode)

Peso Holds as BCRA Revives China Swap

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,352,708.00 | -0.01% |

| USD/ARS | 1,428.50 | +0.26% |

| EUR/ARS | 1,655.20 | +0.11% |

| Gold | 4,366.50 | +0.89% |

| Brent Crude | 81.31 | -2.24% |

| Soybean | 1,126.50 | +0.65% |

| Bitcoin | 66,581.97 | +0.44% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

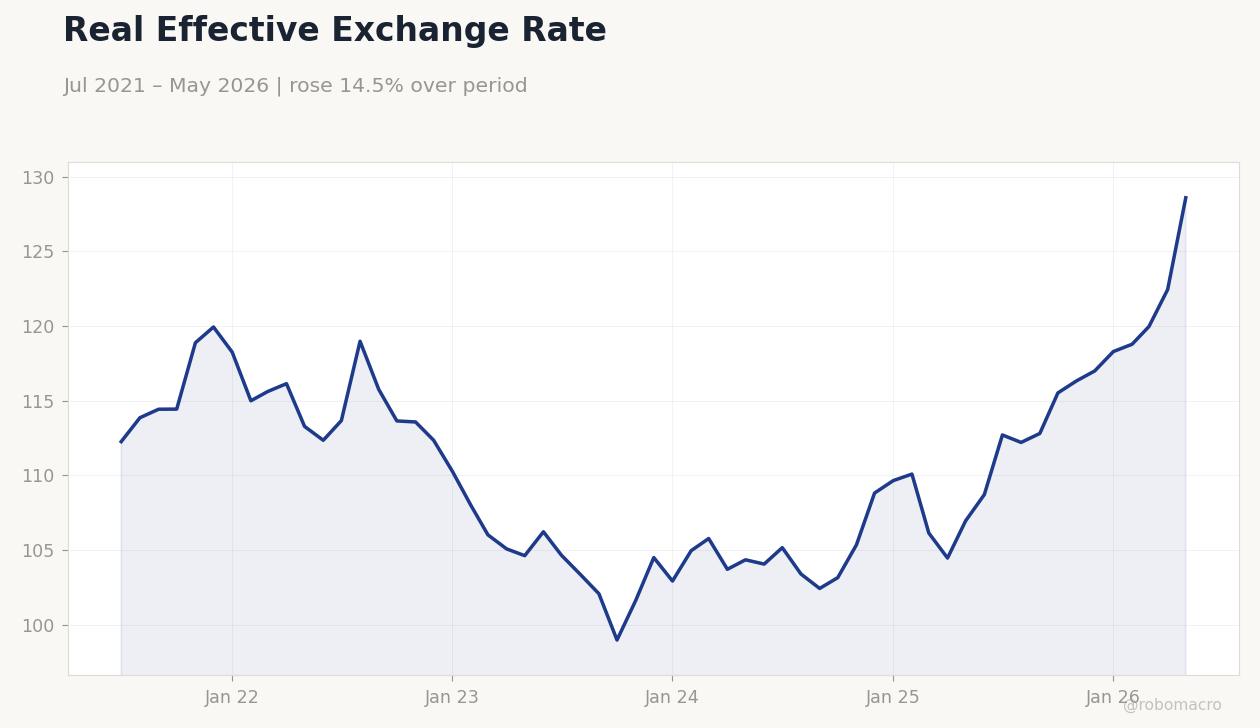

Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL closed flat at 3,352,708 while USD/ARS rose 0.26% to 1,428.50 on thin volumes.

- Argentina’s central banker met Chinese counterpart to discuss currency swap reactivation amid US pressure.

- Soybean futures gained 0.65% to 1,126.50 as export-duty removal expectations lifted farm liquidity.

Yesterday's Recap

Argentine markets showed limited movement on June 15. The MERVAL index slipped 0.01% to 3,352,708 with bank and energy shares offsetting broader weakness. USD/ARS climbed 0.26% to 1,428.50 while EUR/ARS advanced 0.11% to 1,655.20.

Gold rose 0.89% to 4,366.50 on safe-haven demand, whereas Brent crude dropped 2.24% to 81.31 after larger US inventory builds. Soybean prices increased 0.65% to 1,126.50, supporting export revenue forecasts. Argentina’s top central banker held talks in Shanghai on reviving the yuan swap line, a step that could ease reserve pressure without immediate IMF disbursements.

The Day Ahead

No major data releases are scheduled for June 16-17 according to the FinanceFlow calendar. Traders will monitor BCRA money-market survey results for clues on rate expectations. Focus remains on follow-up statements from the Shanghai meetings regarding swap reactivation size and timing.

Soybean export flows and fiscal cash-flow data will be watched for signs of improved liquidity after the planned July 1 duty cut. Markets also await any IMF mission updates on the current programme review.

Other Economic Notes

The Treasury continues to place inflation-linked bonds at declining real yields, signalling improved debt-market access. Elimination of soybean-meal export duties from July is projected to lift farm liquidity while trimming fiscal revenue by around 0.3% of GDP annually. Private analysts have lifted 2026 GDP forecasts toward 4.8% after stronger Q1 national accounts.

Net international reserves have posted six straight weekly gains, reducing immediate pressure on the crawling peg.

Global Macro News

Australia’s central bank held its cash rate at 4.35% and warned that further hikes cannot be ruled out given sticky inflation. The Bank of Japan raised its policy rate, lifting Asian currencies and supporting commodity demand. US-Iran deal progress eased rate-hike fears, sending global stocks and bonds higher.

<i>↓ p.2</i>