Argentina Macro Daily(Beta Mode)

Peso Slides as MERVAL Climbs on Soybean Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,291,883.00 | +1.14% |

| USD/ARS | 1,463.00 | +0.84% |

| EUR/ARS | 1,676.37 | +0.84% |

| Gold | 4,214.20 | -0.23% |

| Brent Crude | 79.01 | -1.05% |

| Soybean | 1,145.75 | +2.05% |

| Bitcoin | 64,142.35 | +1.43% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

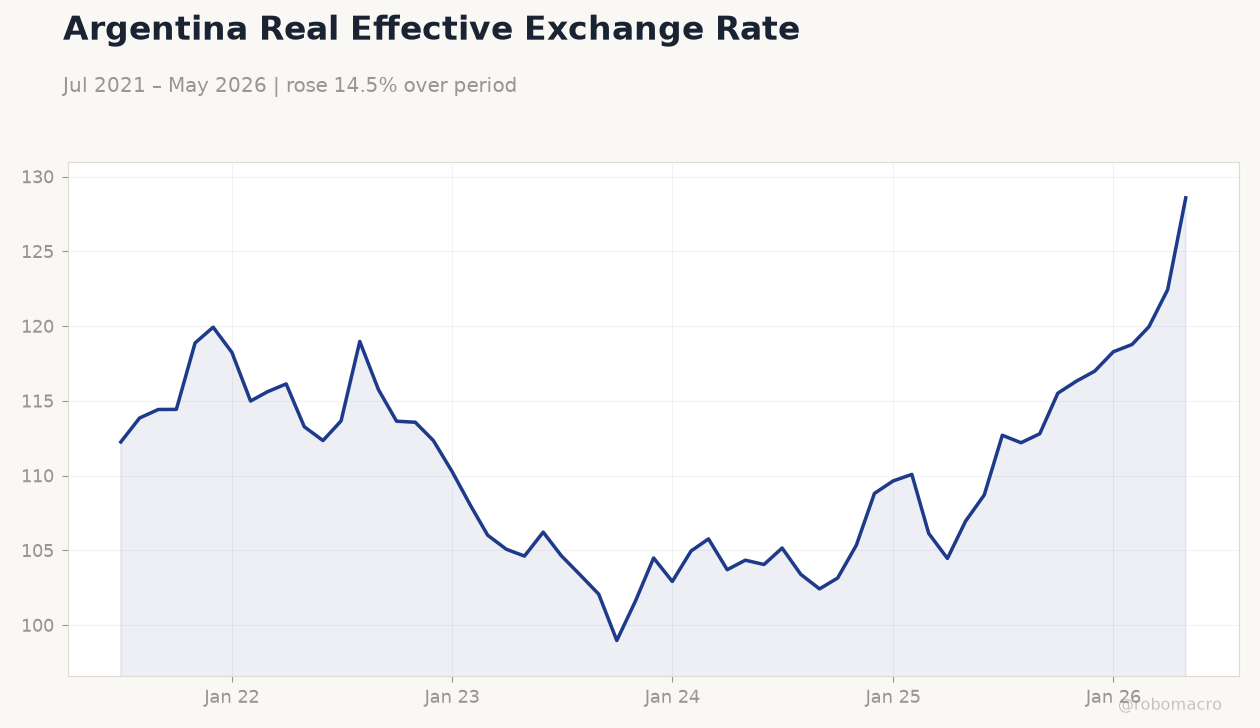

Argentina Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Argentina Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL rose 1.14% to 3,291,883 on selective buying in financials.

- USD/ARS climbed 0.84% to 1,463, extending the peso’s gradual depreciation.

- Soybean futures jumped 2.05% to 1,145.75, boosting export-tax receipts.

Yesterday's Recap

Argentine equities advanced modestly as the MERVAL index closed 1.14 percent higher at 3,291,883 amid thin trading volumes. The official USD/ARS rate increased 0.84 percent to 1,463, reflecting continued BCRA-managed depreciation under the crawling peg. EUR/ARS matched the move, finishing at 1,676.37.

Brent Crude fell 1.05 percent to 79.01 while gold slipped 0.23 percent, offering limited safe-haven support for the peso. Soybean prices surged 2.05 percent on firm Chinese demand and Argentine crop concerns, lifting expected tax collections. Bitcoin gained 1.43 percent, adding mild risk-on tone to local sentiment.

No major data prints occurred, leaving currency and commodity flows as the dominant drivers.

The Day Ahead

Attention centers on BCRA weekly monetary aggregates and reserve updates due later today. Markets will monitor soybean export proceeds and their contribution to net international reserves ahead of July debt obligations. Treasury inflation-linked bond auctions remain in focus for domestic financing signals.

Global carry-trade flows may shift following recent Bank of Japan tightening, with potential spillovers to Argentine assets. Fiscal cash-flow data and IMF Article IV commentary are also expected to shape near-term peso positioning.

Other Economic Notes

Recent analyses question whether the reported fiscal surplus reflects structural reform or temporary expenditure compression. Export-tax collections from soybeans continue to underpin Treasury liquidity despite external price volatility. Persistent inflation and reserve accumulation targets limit BCRA flexibility on the crawling-peg pace.

External financing via CAF and IDB loans has eased immediate rollover pressure but does not address medium-term debt dynamics.

Global Macro News

Russia’s central bank cut its policy rate after GDP contracted, illustrating divergent EM easing cycles. The Swiss National Bank held rates steady while raising its inflation forecast due to geopolitical factors. Both the Philippine and Indonesian central banks delivered hikes to anchor inflation expectations, tightening regional liquidity.

<i>↓ p.2</i>