Argentina Macro Daily(Beta Mode)

Argentina Secures $5bn in Multilateral Loans

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,291,883.00 | +1.14% |

| USD/ARS | 1,461.00 | +0.66% |

| EUR/ARS | 1,669.17 | +3.48% |

| Gold | 4,135.20 | -1.12% |

| Brent Crude | 77.48 | -0.54% |

| Soybean | 1,148.00 | +2.89% |

| Bitcoin | 62,312.00 | -2.56% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

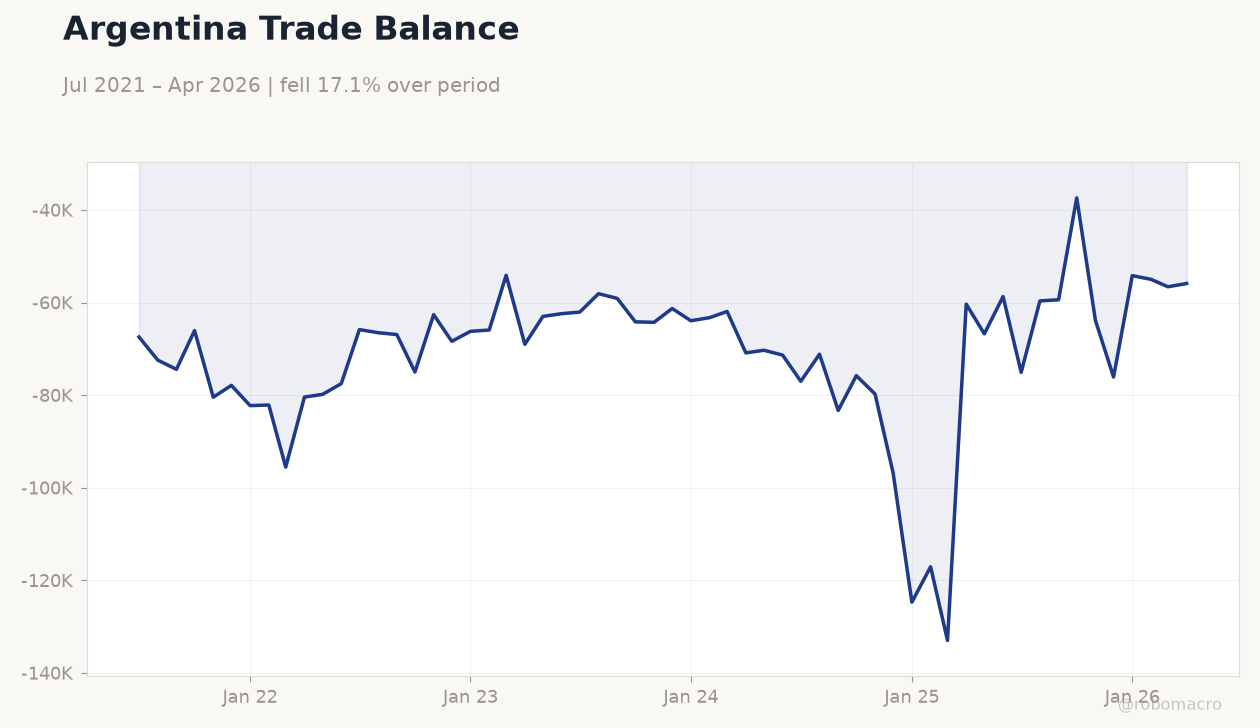

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL advances 1.14% while USD/ARS climbs 0.66% on peso softening

- Government secures up to $5bn in multilateral loans to cut Treasury costs

- Soybean futures surge 2.89%, bolstering export receipts and reserve outlook

Yesterday's Recap

Equity markets extended gains as the MERVAL closed at 3,291,883, supported by banks and energy names. The peso weakened modestly, with USD/ARS rising to 1,461 and EUR/ARS jumping 3.48% to 1,669.17. Argentina’s authorization of $5bn in new multilateral borrowing from institutions including CAF and IDB aims to strengthen net reserves ahead of the next IMF review.

Soybean prices climbed sharply to 1,148, aiding export registrations and fiscal revenue. Gold fell 1.12% to 4,135.20 while Brent Crude eased 0.54% to 77.48, reflecting softer external demand. No major domestic data releases occurred, leaving market focus on reserve accumulation and debt management.

Bitcoin declined 2.56% to 62,312 amid broader risk-off sentiment.

The Day Ahead

Attention turns to weekly BCRA reserve and monetary aggregate updates expected later this week. Treasury LETRAS auctions at 1-, 3- and 6-month tenors will test rollover demand for roughly AR$2.8tn. Markets will monitor soybean export registrations and any further multilateral disbursement announcements.

Global API crude stock data and FOMC minutes may influence commodity-linked ARS flows. Investors await signals on fiscal primary surplus progress following the new borrowing facility.

Other Economic Notes

The $5bn multilateral facility directly supports fiscal consolidation by lowering domestic financing needs and preserving the primary surplus target. Improved real tax collection in recent months reflects stronger formal employment trends. Soybean export strength continues to anchor the current account and limit devaluation pressure on the peso.

Energy tariff adjustments effective July will further reduce subsidy outlays and reinforce fiscal credibility under the IMF programme.

Global Macro News

High policy rates across Latin America continue to weigh on regional growth, prompting calls for fiscal support as an alternative adjustment tool. South Korean chip bonuses have added to local inflation concerns, illustrating how sector-specific wage pressures can complicate central bank decisions elsewhere. <i>↓ p.2</i>