Argentina Macro Daily(Beta Mode)

Argentina Q1 Growth Beats Forecasts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,291,883.00 | +1.14% |

| USD/ARS | 1,470.50 | +0.62% |

| EUR/ARS | 1,672.11 | +0.12% |

| Gold | 4,073.80 | -1.36% |

| Brent Crude | 75.58 | -1.95% |

| Soybean | 1,143.25 | +2.35% |

| Bitcoin | 62,321.93 | -0.55% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

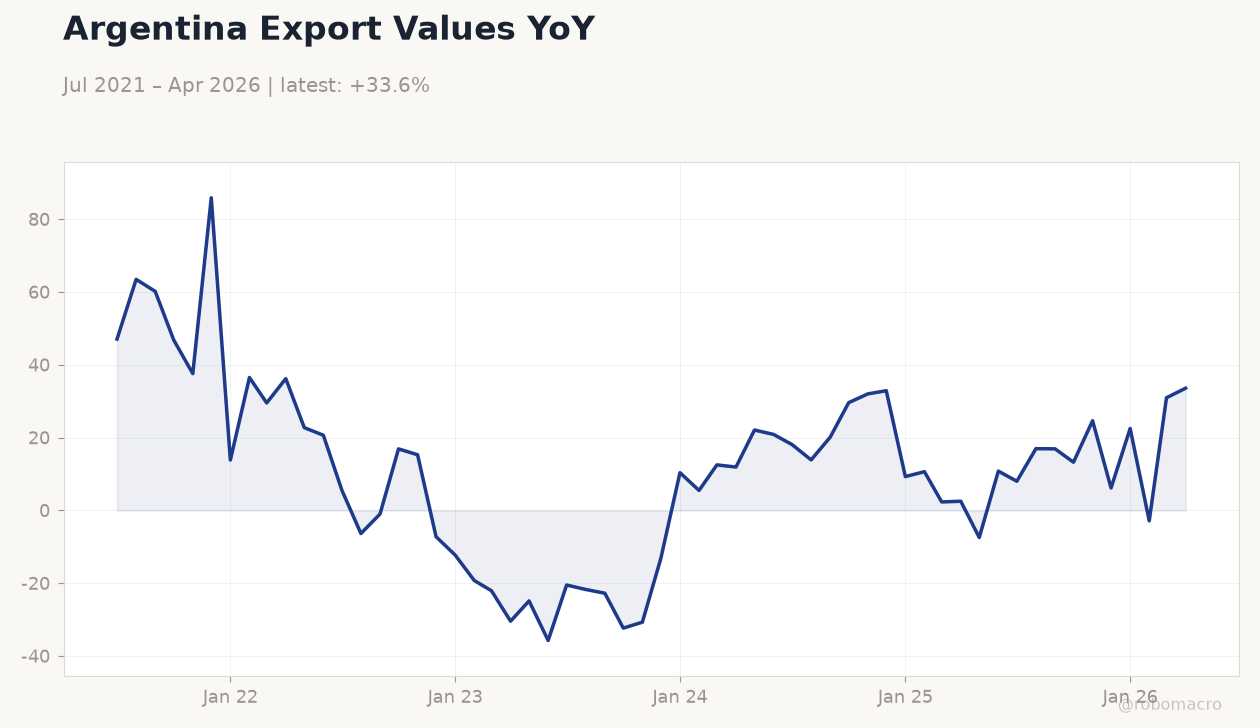

Argentina Export Values YoY | Type: macro_line | Exports YoY %: 33.56 (2026-04-01) | Range: -35.75–85.86 | Trend(6pt): 47.07,-1.007,-30.72,9.285,30.93,33.56

Argentina Export Values YoY | Type: macro_line | Exports YoY %: 33.56 (2026-04-01) | Range: -35.75–85.86 | Trend(6pt): 47.07,-1.007,-30.72,9.285,30.93,33.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Argentina Q1 GDP exceeded expectations despite rising unemployment and lagging wages

- MERVAL advanced 1.14% to 3,291,883 while USD/ARS climbed 0.62% to 1,470.50

- Soybean prices jumped 2.35% supporting export proceeds and reserve accumulation

Yesterday's Recap

Argentine economic activity proved resilient in the first quarter, with GDP growth surpassing consensus forecasts even as unemployment increased and real wages continued to lag inflation. The MERVAL index closed 1.14% higher at 3,291,883 on selective buying in banks and energy names. USD/ARS rose 0.62% to 1,470.50 while EUR/ARS gained 0.12% to 1,672.11.

Soybean futures surged 2.35% to 1,143.25 on favorable South American weather and renewed export program expectations. Brent crude fell 1.95% to 75.58 and gold declined 1.36% to 4,073.80. No major data releases occurred on the calendar, leaving market moves driven by external commodity flows and positioning ahead of month-end.

The Day Ahead

No scheduled Argentine data releases or policy events are listed for the coming session. Attention will center on weekly BCRA reserve updates and any Treasury debt operations. Traders will monitor USD/ARS blue-chip swap levels for signs of month-end demand.

Soybean export flows remain in focus given the recent price strength. Broader EM risk sentiment and global commodity moves will likely dictate local equity and FX direction.

Other Economic Notes

The first-quarter growth outperformance highlights underlying resilience in agriculture and services even as fiscal consolidation continues. Persistent wage-inflation gaps suggest limited immediate consumption impulse, keeping pressure on the current account. Export proceeds from higher soybean prices should aid reserve rebuilding at the BCRA.

Markets continue to watch for any adjustment to the crawling-peg pace amid the milder inflation backdrop observed in recent prints.

Global Macro News

The Thai central bank held its policy rate unchanged for another meeting while lifting its growth outlook, signaling steady external demand conditions. Switzerland’s central bank also kept rates on hold, citing ongoing currency risks that could affect emerging-market funding. Australia’s deputy governor noted further work remains to bring inflation to target, supporting a cautious global rate path.

<i>↓ p.2</i>