Argentina Macro Daily(Beta Mode)

Merval Drops After MSCI Keeps Status Quo

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,248,428.00 | -0.89% |

| USD/ARS | 1,479.00 | +0.55% |

| EUR/ARS | 1,681.65 | +0.46% |

| Gold | 4,006.70 | +0.41% |

| Brent Crude | 72.52 | -1.65% |

| Soybean | 1,137.75 | +2.62% |

| Bitcoin | 61,541.60 | +0.90% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

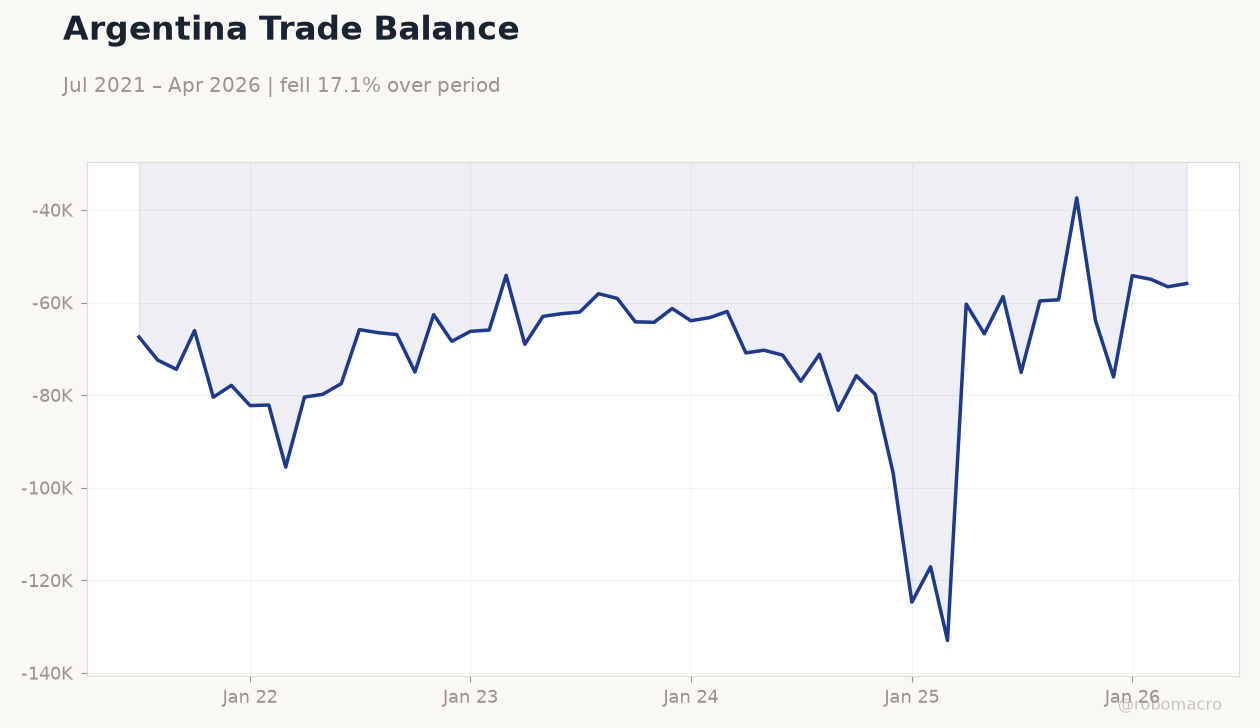

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Argentina Trade Balance | Type: macro_line | USD mn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Merval falls 0.89% while USD/ARS climbs 0.55% to 1,479

- Soybean prices jump 2.62% on renewed export demand

- Treasury readies $16.2 trillion peso auction and $266 million Bonar 2028 sale

Yesterday's Recap

The S&P Merval closed 0.89% lower at 3,248,428 after MSCI confirmed no change in Argentina’s market classification, triggering a nearly 6% drop in the dollar-denominated index that broke below the 2,000 level. The official USD/ARS rate rose 0.55% to 1,479 while the euro-ARS pair gained 0.46% to 1,681.65. Soybean futures surged 2.62% to 1,137.75, bolstering prospects for export receipts.

Brent crude fell 1.65% to 72.52. The Treasury announced plans to roll over 16.2 trillion pesos via eight instruments and raise 266 million dollars through the Bonar 2028.

The Day Ahead

The Treasury will auction inflation-linked CER bonds, dual-currency notes and dollar-linked instruments on Friday to meet the 16.2 trillion peso target. Market participants will monitor soybean export registrations for signs of accelerated sales ahead of the July harvest peak. No INDEC releases are scheduled through the weekend, leaving the focus on fiscal flows and reserve data due next week.

Traders will also track any BCRA intervention signals in the spot market as the crawling peg remains at 1% monthly.

Other Economic Notes

Persistent recession pressures continue to push off-duty police into second jobs as rideshare drivers, highlighting strained household finances and security risks. The government’s supplementary budget trims primary spending by 0.4% of GDP, a move viewed positively by the IMF mission now in Buenos Aires. Improved access to voluntary markets was signaled by the recent placement of 650 million dollars in 2031 notes at 7.75%.

Soybean export strength offers a partial offset to weak industrial and construction readings.

Global Macro News

Bank of Japan board member Tamura signaled further rate hikes toward neutral as inflation risks overshooting the 2% target. Korea’s household debt-to-GDP ratio now exceeds the average of major economies, raising financial-stability concerns. The Bank of Canada faces a policy dilemma of weak growth alongside sticky inflation.

Thailand’s central bank kept rates unchanged while lifting its economic outlook. UK GDP data showed modest expansion. Philippine and Korean equities fell on growth worries and a firmer greenback, indirectly pressuring EM currencies.