Argentina Macro Daily(Beta Mode)

MERVAL Slips as Peso Holds Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,248,428.00 | -0.89% |

| USD/ARS | 1,477.00 | -0.15% |

| EUR/ARS | 1,677.31 | -0.13% |

| Gold | 4,045.20 | +0.36% |

| Brent Crude | 73.02 | -2.98% |

| Soybean | 1,149.25 | +1.93% |

| Bitcoin | 59,999.00 | +0.46% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

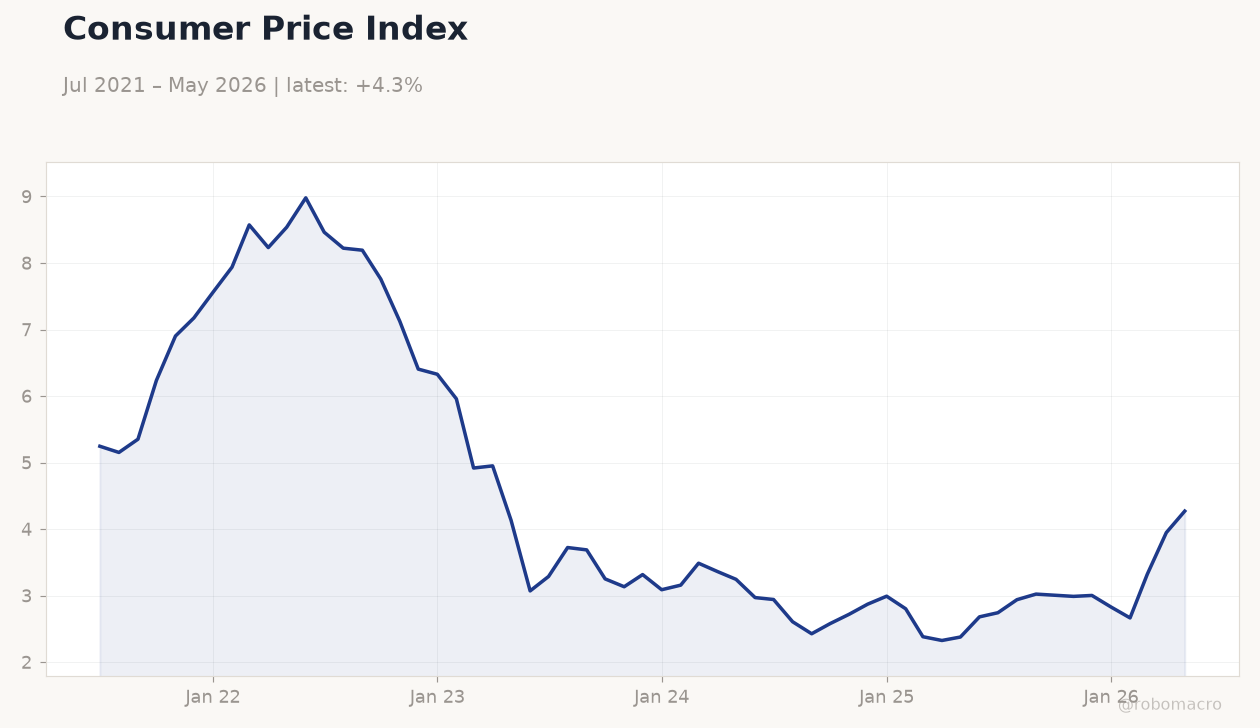

Consumer Price Index | Type: macro_line | Index: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27

Consumer Price Index | Type: macro_line | Index: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL falls 0.89% to 3,248,428 amid thin trading and global risk-off sentiment.

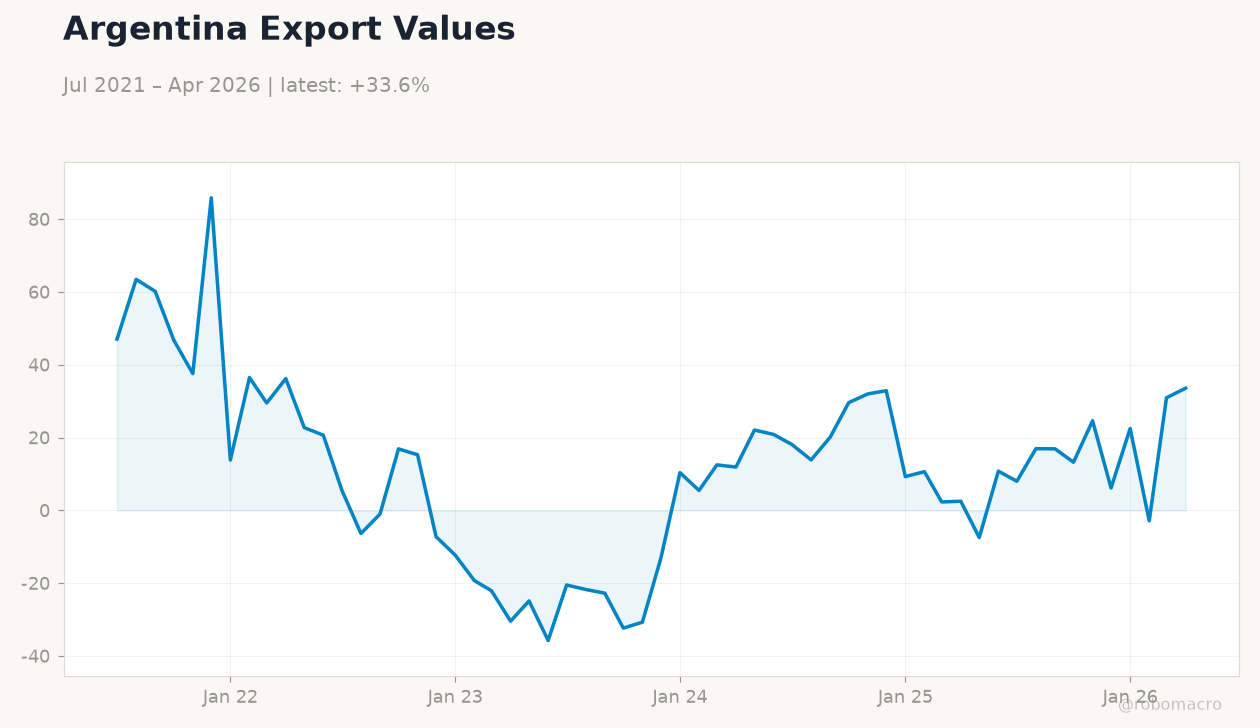

- USD/ARS eases 0.15% to 1,477 while soybean futures rise 1.93% on export support.

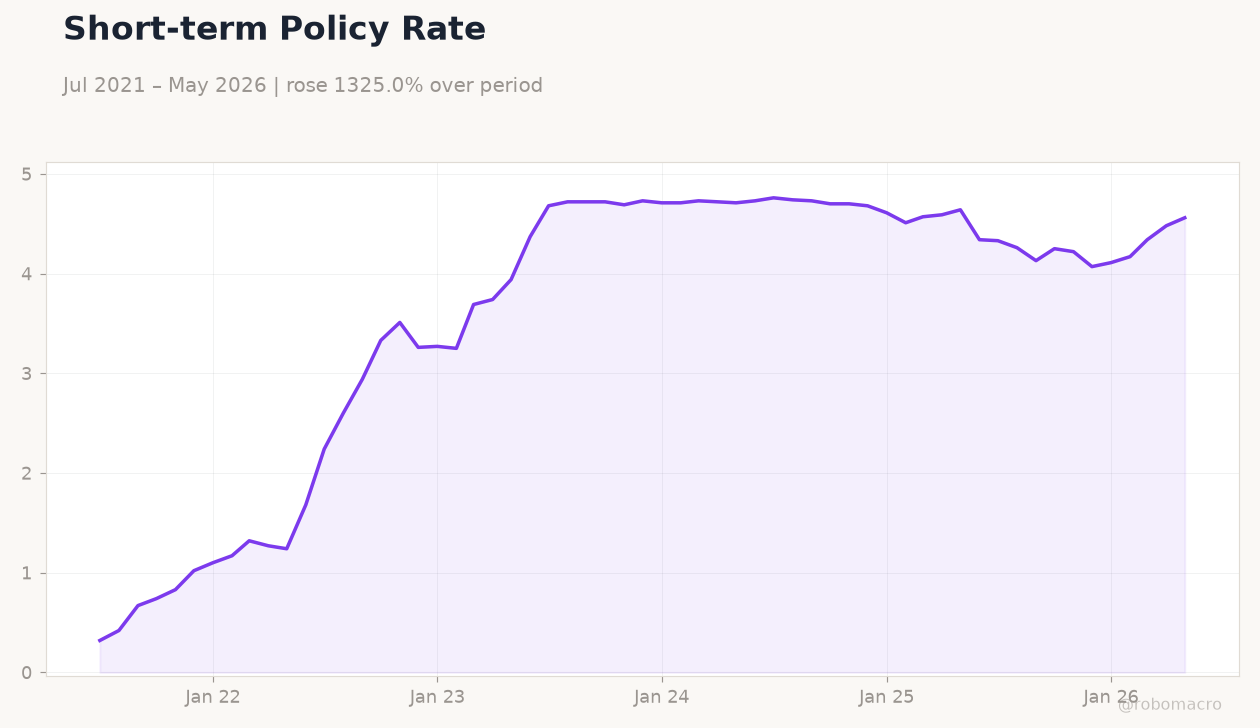

- BCRA policy remains on hold as reserves stay above target and inflation trends lower.

Yesterday's Recap

Argentine markets recorded modest losses with the MERVAL declining 0.89% to close at 3,248,428 on limited volume. The official USD/ARS rate eased 0.15% to 1,477 while the EUR/ARS pair fell 0.13% to 1,677.31. Soybean prices advanced 1.93% to 1,149.25, providing some support to export revenues and reserve accumulation.

Brent crude dropped 2.98% to 73.02, reducing import costs for the energy balance. Gold rose 0.36% to 4,045.20 as a safe-haven bid emerged. Bitcoin gained 0.46% to 59,999.

No major data releases occurred, leaving focus on the steady monetary base contraction and ongoing fiscal consolidation efforts. The Argentina 10Y benchmark showed no change, reflecting stable local demand for peso debt.

The Day Ahead

The calendar remains clear of scheduled releases through the weekend. Markets will monitor weekly BCRA monetary aggregates expected later today for signs of base expansion near 0.6%. Attention turns to month-end reserve targets due June 30, with soy-dollar inflows likely to keep reserves above 29 billion dollars.

Traders await any signals on the 1% monthly crawl rate ahead of July inflation data. IMF review timing remains a key watch item as primary surplus targets stay on track. Peso liquidity conditions should remain orderly given the absence of large debt maturities.

Other Economic Notes

Export tax collections continued to rise, bolstering Treasury cash flow ahead of July payments. The government extended average maturity of peso liabilities through dual-currency LETRAS placements at real yields near 2.8%. Fiscal consolidation remains on course, supporting IMF program compliance and potential mid-July review completion.

International reserves received steady inflows from soybean exports, keeping the BCRA within its quarterly targets. These developments reinforce market expectations for measured monetary easing later in the year.