Argentina Macro Daily(Beta Mode)

MERVAL Climbs as Soybeans Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,123,411.25 | +0.88% |

| USD/ARS | 1,477.00 | -0.02% |

| EUR/ARS | 1,682.13 | +0.22% |

| Gold | 4,065.10 | -0.33% |

| Brent Crude | 73.36 | +1.90% |

| Soybean | 1,147.75 | +1.91% |

| Bitcoin | 59,936.16 | +0.68% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

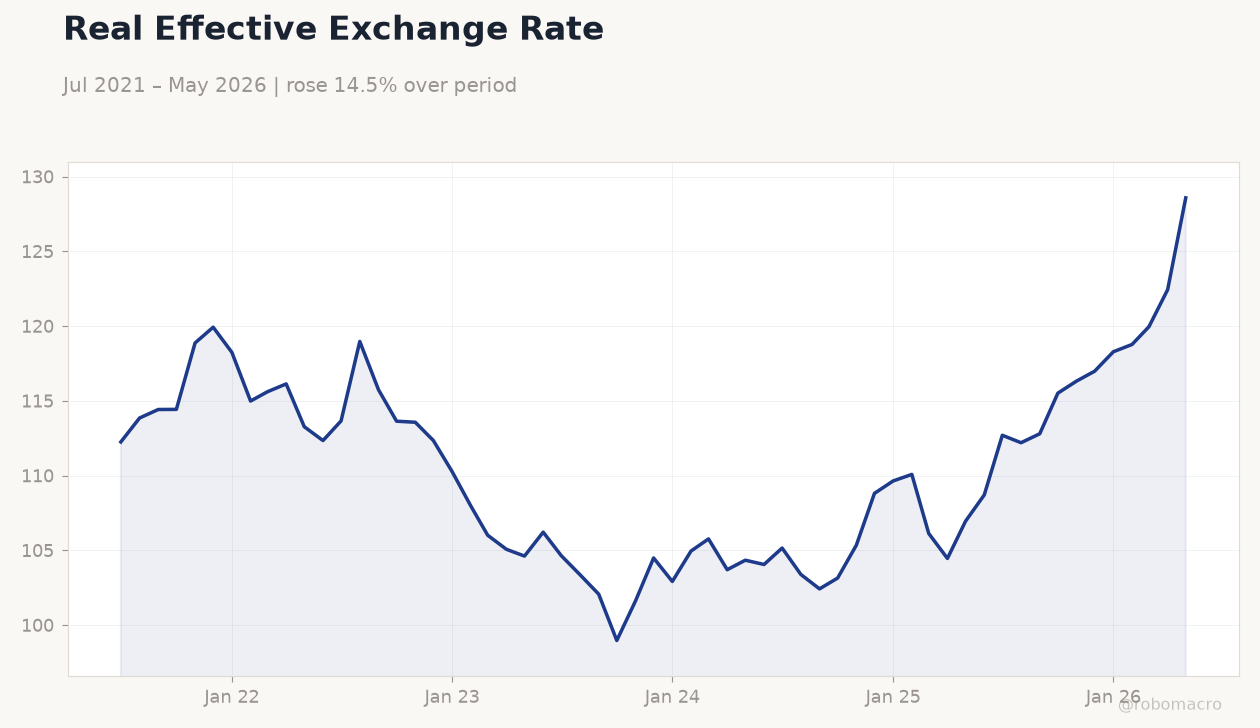

Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Real Effective Exchange Rate | Type: macro_line | Index: 128.6 (2026-05-01) | Range: 98.97–128.6 | Trend(6pt): 112.3,115.7,101.6,109.6,120,128.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL rose 0.88% to 3,123,411.25 on firm commodity prices.

- USD/ARS stayed near 1,477.00 with a 0.02% dip.

- Soybean prices jumped 1.91%, bolstering export revenues.

Yesterday's Recap

Argentine equities advanced as the MERVAL closed 0.88% higher at 3,123,411.25, tracking gains in soybeans and Brent crude. The official USD/ARS rate edged 0.02% lower to 1,477.00 while EUR/ARS climbed 0.22% to 1,682.13. Gold slipped 0.33% to 4,065.10, offering limited support to peso holdings.

No INDEC releases or BCRA interventions were reported, leaving markets to focus on external commodity signals. Bitcoin added 0.68% to 59,936.16, providing minor diversification flows. The Argentina 10Y bond showed no quoted change amid thin trading.

Overall activity remained subdued with no fresh fiscal or reserve data. Export-tax collections continue to benefit from the soybean rally, supporting primary fiscal balance targets. The government maintains its commitment to reserve accumulation without fresh capital controls.

IMF Article IV recommendations remain focused on a more flexible FX regime and sustained surpluses. Broader indexation trends show gradual cooling, aiding disinflation momentum.

The Day Ahead

The calendar stays empty through 30 June, with no INDEC or BCRA releases scheduled. Markets will monitor soybean futures and any Treasury auction updates for USD-linked notes. Traders expect limited peso volatility absent new reserve or inflation prints.

Global oil and grain movements will likely dictate ARS crosses. Attention may shift to early July policy signals once the quiet period ends.

Other Economic Notes

Export-tax collections continue to benefit from the soybean rally, supporting primary fiscal balance targets. The government maintains its commitment to reserve accumulation without fresh capital controls. IMF Article IV recommendations remain focused on a more flexible FX regime and sustained surpluses.

Broader indexation trends show gradual cooling, aiding disinflation momentum.

Global Macro News

The ECB cut its key rate, easing external financing conditions for emerging markets including Argentina. <i>↓ p.2</i>