Argentina Macro Daily(Beta Mode)

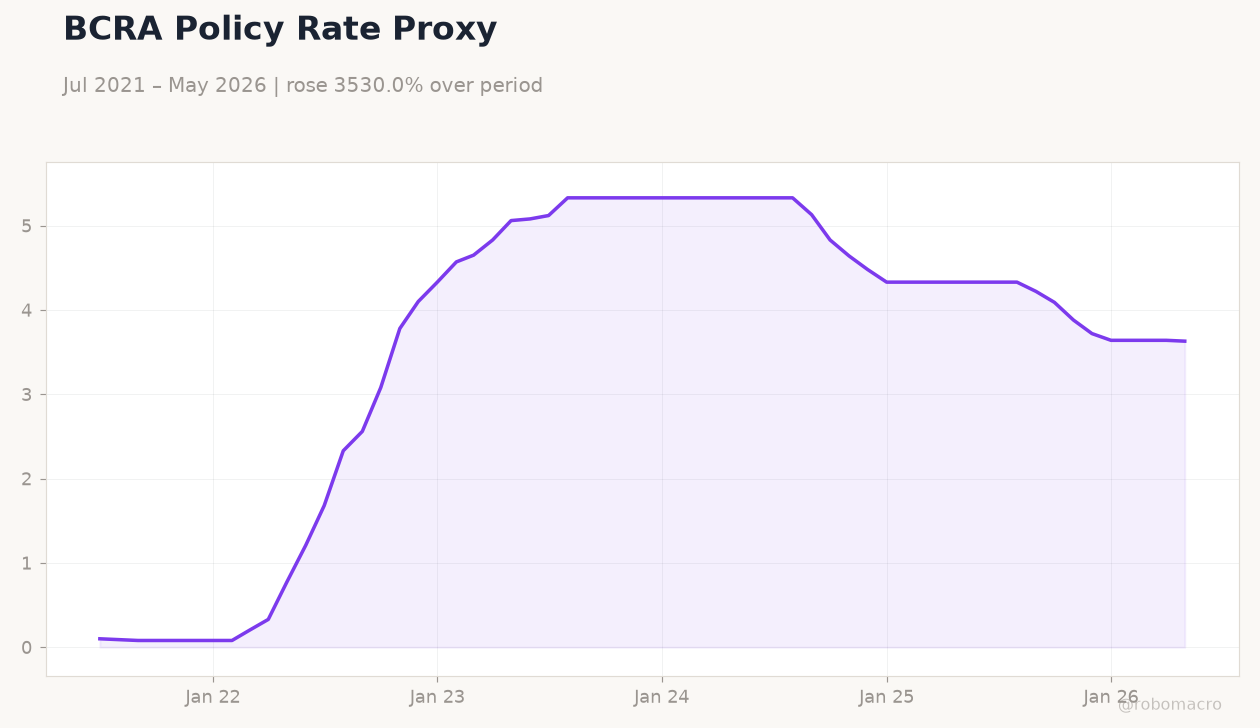

Stronger GDP Outlook Challenges BCRA

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,176,751.00 | +1.71% |

| USD/ARS | 1,479.19 | +0.13% |

| EUR/ARS | 1,684.20 | +0.35% |

| Gold | 4,029.20 | +0.17% |

| Brent Crude | 73.66 | +0.70% |

| Soybean | 1,137.75 | +2.62% |

| Bitcoin | 59,197.13 | -1.57% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

10Y-2Y Yield Spread | Type: macro_line | %: 4.38 (2026-06-26) | Range: 1.19–4.98 | Trend(6pt): 1.48,3.72,3.79,4.38,4.4,4.38 | %: 4.07 (2026-06-26) | Range: 0.17–5.19 | Trend(6pt): 0.25,4.07,4.2,3.97,4.09,4.07

10Y-2Y Yield Spread | Type: macro_line | %: 4.38 (2026-06-26) | Range: 1.19–4.98 | Trend(6pt): 1.48,3.72,3.79,4.38,4.4,4.38 | %: 4.07 (2026-06-26) | Range: 0.17–5.19 | Trend(6pt): 0.25,4.07,4.2,3.97,4.09,4.07

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL gains 1.71% to 3,176,751 on fiscal optimism

- USD/ARS rises 0.13% to 1,479.19 while soybean prices jump 2.62%

- Stronger GDP outlook complicates BCRA easing path

Yesterday's Recap

Equity markets advanced as the MERVAL posted a 1.71% gain, driven by bank and energy shares on renewed fiscal consolidation hopes. The official USD/ARS rate ticked 0.13% higher to 1,479.19, while the EUR/ARS climbed 0.35% to 1,684.20. Soybean futures surged 2.62% to 1,137.75, supporting export revenue expectations for Argentina.

Brent crude rose 0.70% to 73.66, adding mild upside to fiscal accounts. No major data releases occurred, leaving market focus on the Valor International report that a firmer GDP trajectory now pressures the BCRA to delay rate cuts. Gold edged 0.17% higher to 4,029.20 amid safe-haven demand.

Bitcoin fell 1.57% to 59,197.13, showing limited spillover to local assets.

The Day Ahead

Markets will monitor any follow-up comments from Economy Minister Caputo on IMF program compliance. Treasury operations and weekly BCRA reserve updates are expected to provide liquidity signals. Soybean export volumes and any fresh fiscal data will remain in focus for peso stability.

Global commodity moves, especially in grains and energy, will influence ARS flows. Investors await clarity on whether stronger growth alters the BCRA’s forward guidance timeline.

Other Economic Notes

Fiscal consolidation efforts continue to anchor investor sentiment despite the absence of fresh releases. Soybean price strength offers a positive impulse to trade balances and reserve accumulation. The peso’s modest depreciation keeps import costs contained while supporting export competitiveness.

Broader themes center on sustaining primary surpluses to meet IMF targets through year-end.

Global Macro News

The European Central Bank signaled a possible rate pause as inflation moderates, easing external pressure on emerging-market funding costs. Australia’s central bank flagged conflict and oil risks to inflation, supporting Brent’s modest advance. Bank of Korea intervention of 20 trillion won to defend its currency highlights ongoing EM FX volatility that can spill into ARS trading.

<i>↓ p.2</i>