Argentina Macro Daily(Beta Mode)

Peso Weakens as MERVAL Falls on Quiet Trade

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,121,855.00 | -1.48% |

| USD/ARS | 1,489.00 | +0.34% |

| EUR/ARS | 1,694.59 | +0.05% |

| Gold | 4,076.80 | +0.21% |

| Brent Crude | 70.70 | -1.22% |

| Soybean | 1,154.00 | +2.46% |

| Bitcoin | 61,194.08 | +1.98% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

10Y Treasury Yield | Type: macro_line | Percent: 4.44 (2026-06-30) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.44

10Y Treasury Yield | Type: macro_line | Percent: 4.44 (2026-06-30) | Range: 1.19–4.98 | Trend(6pt): 1.37,3.83,3.88,4.23,4.38,4.44

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL falls 1.48% to 3,121,855 amid light volumes and global EM caution.

- USD/ARS climbs 0.34% to 1,489, extending gradual peso depreciation.

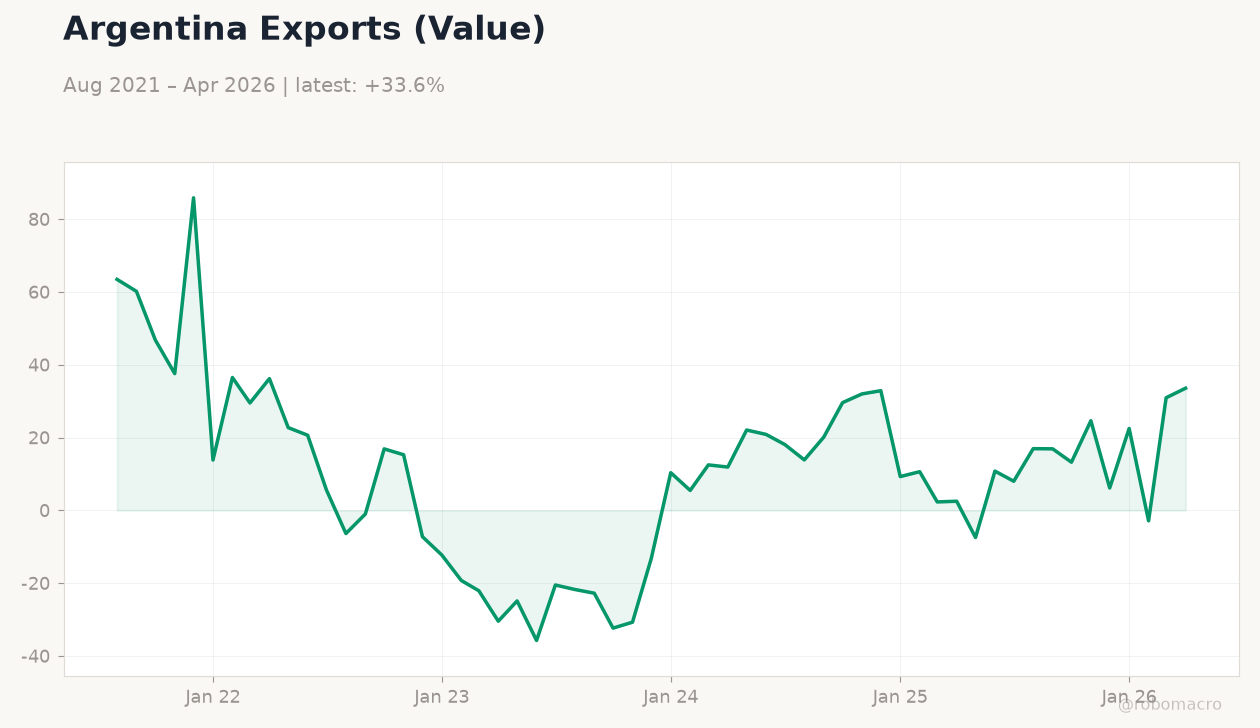

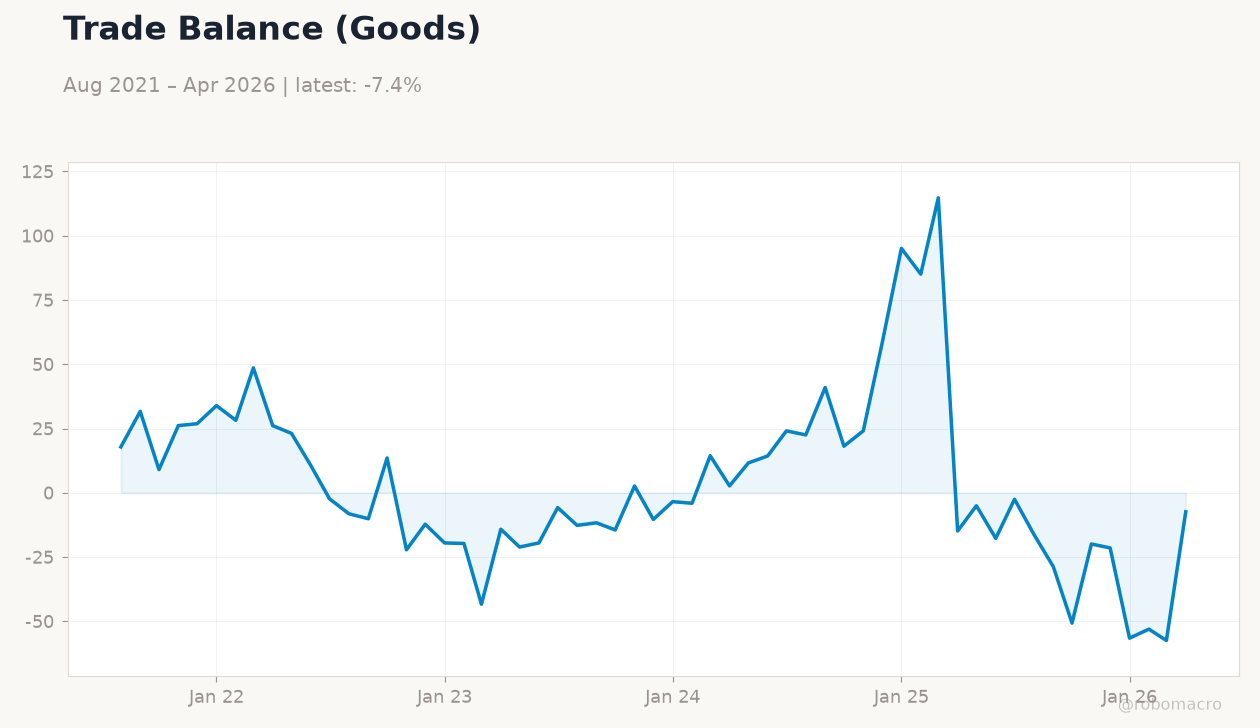

- Soybean futures surge 2.46%, lifting Argentine export revenue prospects.

Yesterday's Recap

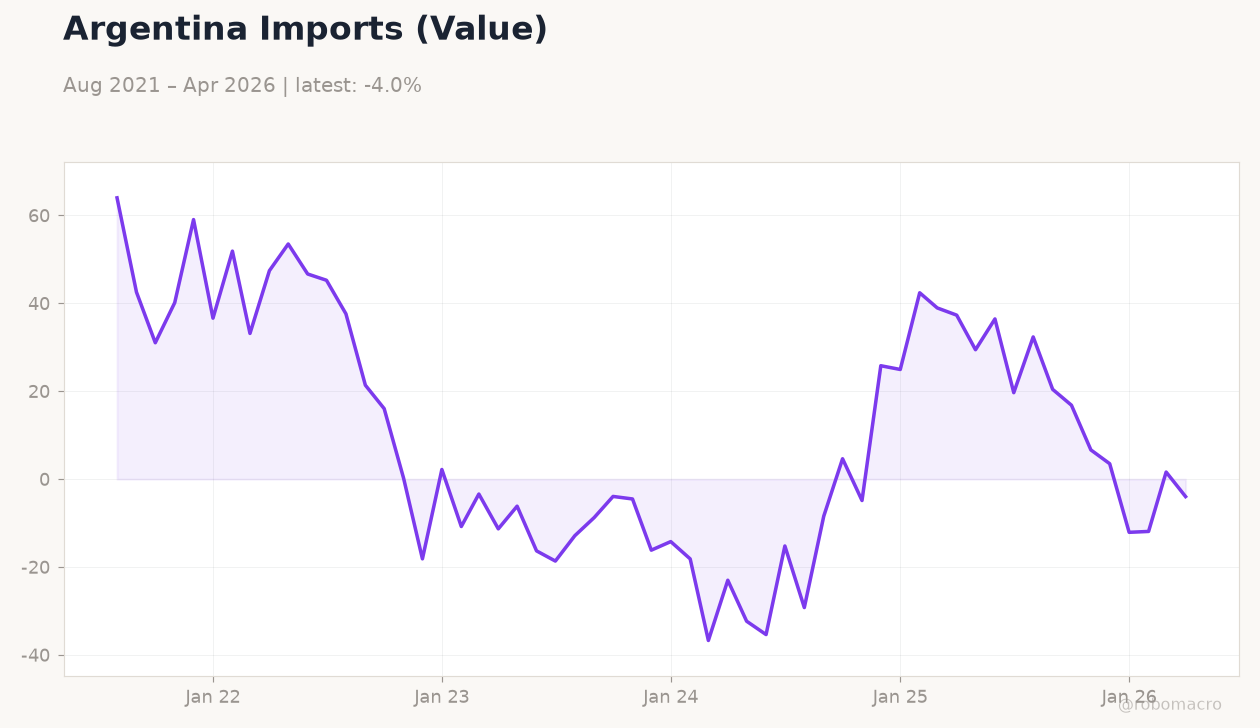

Argentine markets operated without fresh domestic data releases, leaving price action driven by equity and currency flows. The MERVAL index declined 1.48% to 3,121,855, with banking and industrial names leading losses on reduced holiday-adjusted turnover. The official USD/ARS rate advanced 0.34% to 1,489, reflecting ongoing demand for dollars despite BCRA sales.

EUR/ARS rose a modest 0.05% to 1,694.59 in line with euro strength elsewhere. Brent Crude dropped 1.22% to 70.70, while soybean prices jumped 2.46% to 1,154, supporting the trade surplus outlook. Gold edged 0.21% higher and Bitcoin gained 1.98%, providing limited offsets.

The Argentina 10Y benchmark showed no movement in the absence of new supply.

The Day Ahead

No economic releases or policy events are scheduled through July 3, keeping the local calendar empty. Traders will monitor soybean export registrations and daily BCRA reserve updates for any reserve-building signals. Global commodity moves and EM bond flows are expected to set the tone for peso and equity trading.

Attention may shift to any Treasury bill reopenings that could test external funding appetite. The absence of auctions reduces immediate supply pressure on local curves. Markets await the next BCRA monetary aggregates print for clues on liquidity conditions.

Other Economic Notes

Fiscal consolidation remains the anchor for Argentina’s macro stability, with primary surpluses reinforcing zero-deficit credibility. Soybean and corn export volumes continue to drive reserve accumulation and sustain consecutive trade surpluses. The crawling-peg framework has helped moderate core goods inflation, lowering the risk of near-term rate hikes.

Private-sector wage agreements settling below union demands further support disinflation momentum. IMF program adherence keeps multilateral disbursements on track and bolsters external buffers.