Argentina Macro Daily(Beta Mode)

MERVAL Climbs as USD/ARS Eases 0.1%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| MERVAL | 3,157,091.00 | +1.13% |

| USD/ARS | 1,488.00 | -0.10% |

| EUR/ARS | 1,701.89 | +0.42% |

| Gold | 4,189.50 | +1.87% |

| Brent Crude | 71.85 | +0.07% |

| Soybean | 1,131.75 | +0.49% |

| Bitcoin | 61,925.89 | +0.72% |

| Argentina 10Y | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

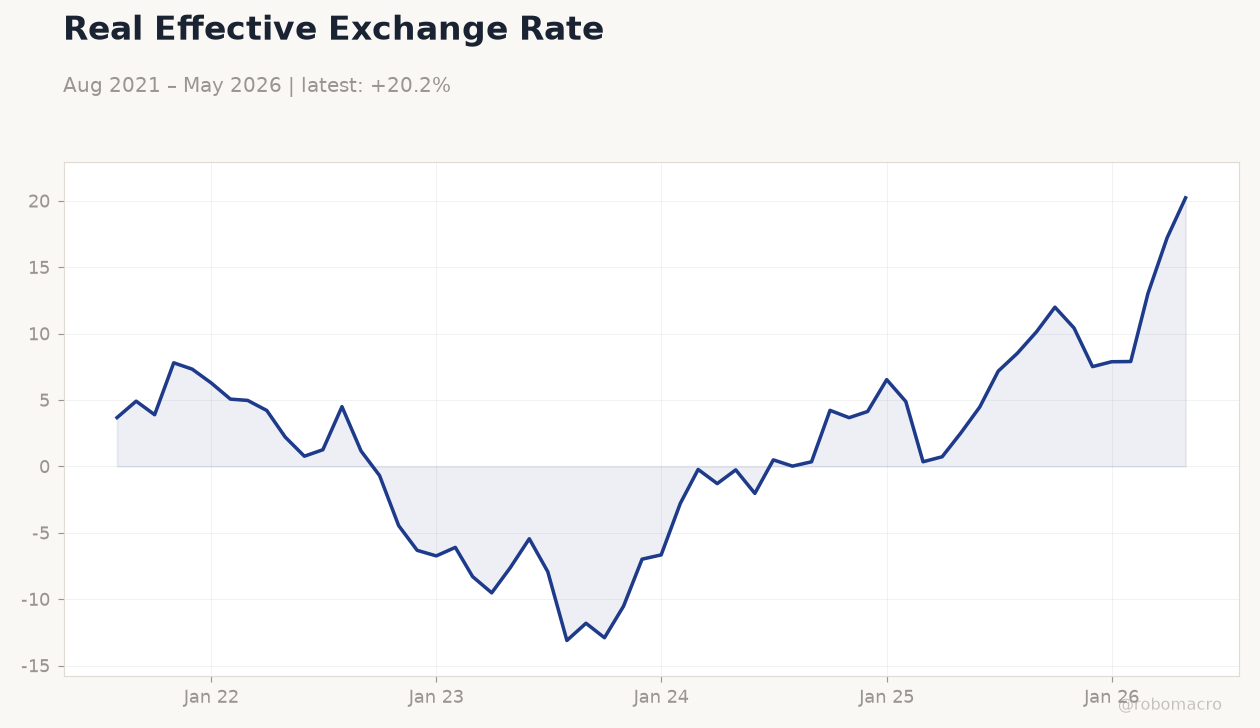

Real Effective Exchange Rate | Type: macro_line | REER Index: 20.23 (2026-05-01) | Range: -13.11–20.23 | Trend(6pt): 3.673,-0.6914,-6.99,4.884,17.21,20.23

Real Effective Exchange Rate | Type: macro_line | REER Index: 20.23 (2026-05-01) | Range: -13.11–20.23 | Trend(6pt): 3.673,-0.6914,-6.99,4.884,17.21,20.23

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MERVAL advanced 1.13% to 3,157,091 on financial and energy buying.

- USD/ARS declined 0.10% to 1,488 while EUR/ARS rose 0.42%.

- Gold jumped 1.87% to 4,189.50, reinforcing safe-haven demand.

Yesterday's Recap

Argentine equity markets posted solid gains with the MERVAL rising 1.13 percent, driven by renewed interest in financial and energy names. The official USD/ARS rate eased 0.10 percent to 1,488, narrowing parallel-market premia. EUR/ARS climbed 0.42 percent to 1,701.89 in line with euro strength against the dollar.

Brent crude edged 0.07 percent higher to 71.85 dollars per barrel while soybean futures added 0.49 percent to 1,131.75. Bitcoin gained 0.72 percent to 61,925.89, providing ancillary risk-on sentiment. The Argentina 10-year bond yield remained unquoted, leaving duration markets without fresh pricing.

Net reserve accumulation continued at a measured pace, supporting peso stability. Genneia filed for the first Argentine IPO in New York since 2019, signaling improved external market access for local issuers.

The Day Ahead

The economic calendar remains empty through the July 4 holiday period, leaving markets focused on global risk signals. Traders will monitor soybean export registrations and any Treasury bill rollover announcements. Liquidity in the official FX market is expected to stay thin ahead of the weekend.

Global equity and commodity moves will likely dictate local sentiment given the absence of domestic data. Attention stays on reserve levels and any BCRA interventions in the spot market. Lower oil prices and steady soybean demand offer supportive external conditions for Argentine assets.

Other Economic Notes

Genneia’s filing for a New York IPO marks the first Argentine corporate listing attempt in the US since 2019, signaling improved external market access. The Cocos fintech acquisition of Warren expands Argentine digital finance reach into Brazil, highlighting capital export from local tech founders. Fiscal consolidation efforts continue to anchor investor views, with soybean export volumes remaining a key hard-currency source.

Broader EM bond inflows into Asia suggest risk appetite may extend to Argentine assets if global yields stabilize.

Global Macro News

South Korea’s central bank projected easing July inflation, reducing pressure on regional rates. Vietnam’s central bank balances growth and dong stability amid external headwinds. <i>↓ p.2</i>