Brazil Macro Daily(Beta Mode)

Copom Minutes Highlight Inflation Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 182,733.00 | -1.45% |

| USD/BRL | 5.22 | -0.39% |

| EUR/BRL | 6.01 | -0.67% |

| Vale | 14.95 | -1.25% |

| Petrobras | 20.33 | +2.57% |

| WTI Crude | 96.08 | +1.69% |

| Gold | 4,461.80 | +1.97% |

| Bitcoin | 67,920.00 | -1.27% |

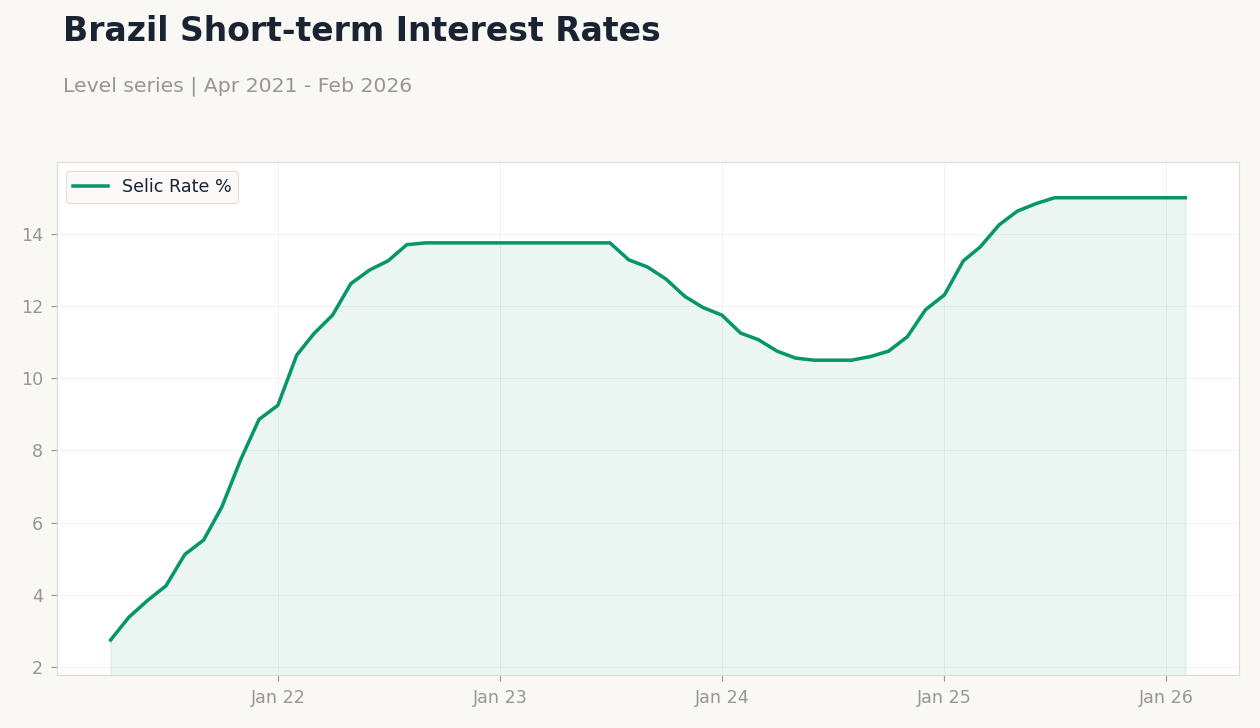

| Brazil Short-term Rate | 15.00% | +0.00% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | - |

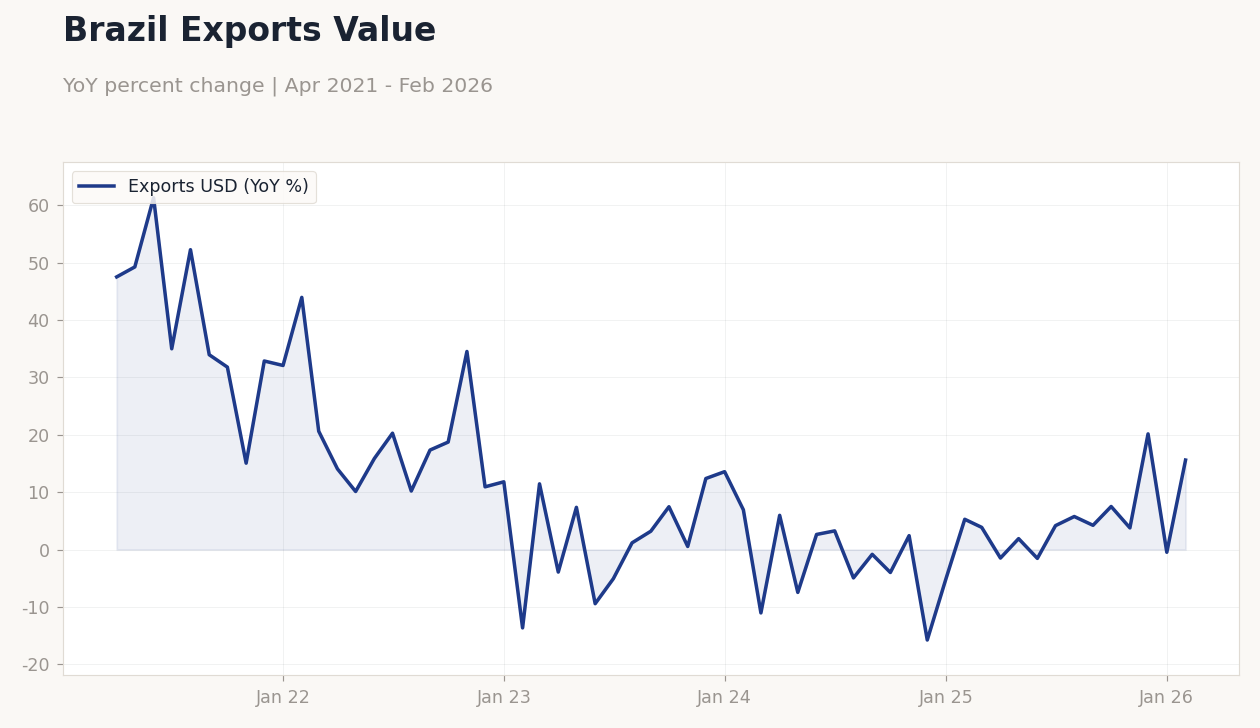

Brazil Exports Value | Type: macro_line | Exports USD: 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 47.51,15.87,1.174,-3.992,20.16,15.6

Brazil Exports Value | Type: macro_line | Exports USD: 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 47.51,15.87,1.174,-3.992,20.16,15.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 5.40 | 5.70 | 04:00 |

- BCB Copom minutes stressed inflation vigilance, holding Selic at 15.00%.

- Bovespa fell 1.45% to 182,733.00 on mining weakness; Petrobras rose 2.57%.

- USD/BRL dipped 0.39% to 5.22 amid stable rates and EM gains.

Yesterday's Recap

The BCB released Copom meeting minutes, emphasizing vigilance on inflation amid fiscal uncertainties, with no changes to the Selic rate at 15.00%. Brazilian equities weakened as the Bovespa index closed at 182,733.00, down 1.45%, pressured by declines in mining stocks like Vale, which fell 1.25% to 14.95. Currency markets saw the USD/BRL pair decline 0.39% to 5.22, supported by stable short-term rates and a slight dip in global risk aversion.

Petrobras bucked the trend, rising 2.57% to 20.33 on firmer WTI crude prices, which advanced 1.69% to 96.08. EUR/BRL weakened 0.67% to 6.01, aligning with broader EM currency gains. No major economic data prints occurred beyond the minutes, but markets digested their tone on sustained high rates.

Overall volumes were light, with investors eyeing upcoming unemployment figures.

The Day Ahead

Brazil's headline unemployment rate is due at 04:00 ET, with consensus expecting a rise to 5.7% from 5.4% prior, potentially signaling labor market softening amid high borrowing costs. A higher-than-expected print could pressure equities and the real, reinforcing BCB's cautious stance on rates. No other Brazilian events are scheduled, allowing focus on this key indicator for insights into domestic demand.

Globally, attention may shift to any spillover from US economic signals, though Brazil-specific catalysts remain dominant.

Other Economic Notes

Broader fiscal sustainability remains a concern, with high Selic rates at 15.00% straining public debt dynamics despite commodity export resilience in iron ore and soybeans. Inflation targeting faces headwinds from global energy prices, as evidenced by Petrobras' performance tied to WTI movements. Structural reforms in efficiency could bolster long-term growth, but near-term commodity volatility poses risks to export-driven sectors.

Global Macro News

Global warnings about an Iran war as a 'catastrophe' for the economy, issued by G7 ministers and Germany's defense minister, heightened oil price volatility, indirectly supporting Brazil's Petrobras amid WTI gains. (cont...)