Brazil Macro Daily(Beta Mode)

Vale Surges, Crude Rallies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 187,953.00 | +0.26% |

| USD/BRL | 5.17 | -0.53% |

| EUR/BRL | 5.95 | -0.85% |

| Vale | 15.91 | +5.36% |

| Petrobras | 20.75 | -0.29% |

| WTI Crude | 107.14 | +7.01% |

| Gold | 4,654.80 | -2.68% |

| Bitcoin | 66,463.04 | -2.37% |

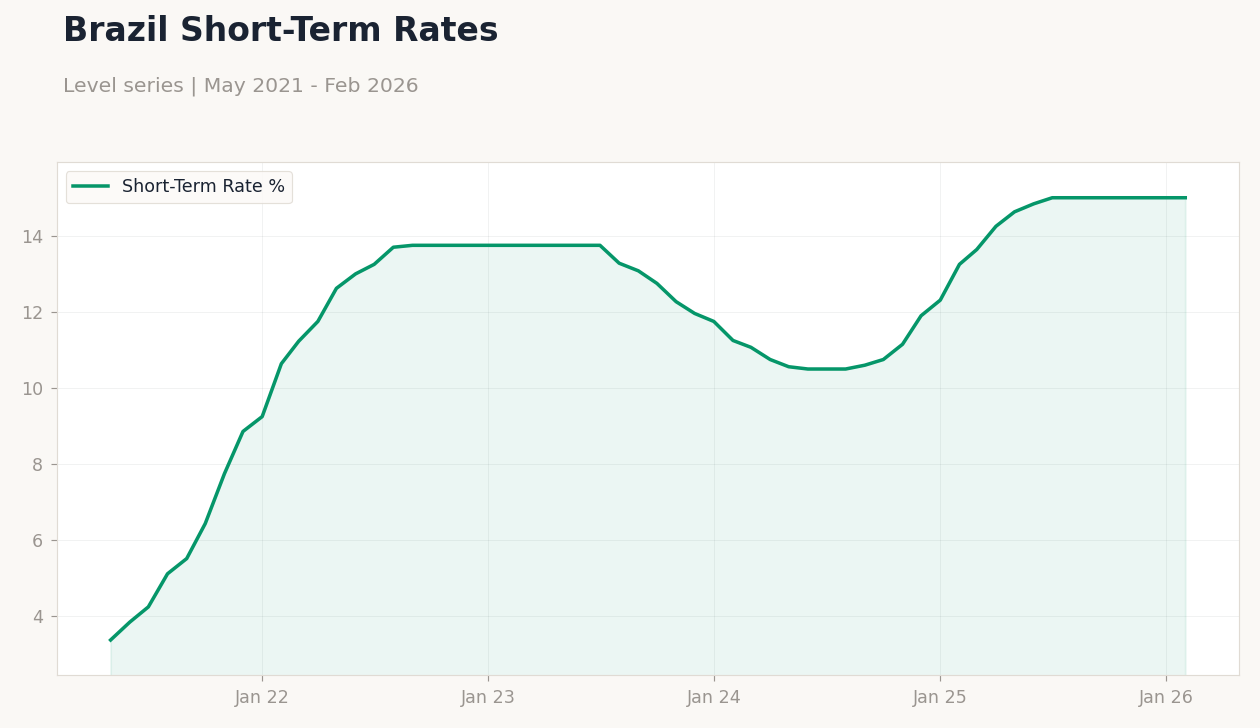

| Brazil Short-term Rate | 15.00% | +0.00% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Exports Value | Type: macro_line | Exports USD: 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 49.25,20.28,3.199,2.423,-0.4707,15.6

Brazil Exports Value | Type: macro_line | Exports USD: 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 49.25,20.28,3.199,2.423,-0.4707,15.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | 1.80 | 0.70 | 04:00 |

- Bovespa gained modestly amid commodity strength, with Vale leading on iron ore optimism.

- USD/BRL weakened as global risk appetite improved, supporting EM currencies.

- No major data releases yesterday, but focus shifts to today's industrial production print.

Yesterday's Recap

Brazilian markets showed resilience with Bovespa closing at 187,953, up 0.26%, driven by commodity exporters. Vale surged 5.36% to 15.91, buoyed by rising iron ore demand from China amid stimulus expectations. Petrobras dipped 0.29% to 20.75 despite WTI crude jumping 7.01% to 107.14 on global supply concerns.

USD/BRL fell 0.53% to 5.17, reflecting broader EM currency strength, while EUR/BRL declined 0.85% to 5.95. Gold prices dropped 2.68% to 4,654.80, pressuring mining-related assets slightly. Bitcoin slid 2.37% to 66,463.04, but overall risk-on sentiment prevailed without key data releases.

Brazil's short-term rate held steady at 15.00%, with no shifts in long-term yields reported.

The Day Ahead

Investors eye Brazil's industrial production month-over-month at 04:00 ET, with consensus at 0.7% versus previous 1.8%. A softer print could signal manufacturing slowdown, potentially weighing on Bovespa and strengthening calls for Selic easing. No other major releases are scheduled, keeping focus on this medium-impact indicator for insights into Q1 growth momentum.

Tomorrow brings no events, so markets may digest global cues post-release. The data could influence commodity export outlooks, especially for iron ore and oil sectors.

Other Economic Notes

Investments in technology are poised to boost Brazil's productivity and industrial gains, as highlighted in recent studies emphasizing innovation and wealth retention. Fiscal sustainability remains a concern amid debates over spending caps, with potential budget loosening for 2026 risking deficit expansion. Commodity exports, including soybeans and iron ore, continue to support the trade balance despite high interest rates curbing domestic demand.

Global Macro News

Rising WTI crude prices to 107.14 bolster Brazil's oil sector, with Petrobras positioned to benefit from export revenues amid Middle East tensions. China's state insurer is leveraging Brazil's high benchmark rates for export financing, enhancing bilateral trade flows and supporting BRL stability. (cont...)