Brazil Macro Daily(Beta Mode)

PMI Dips, Oil Plunges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 188,259.00 | +0.05% |

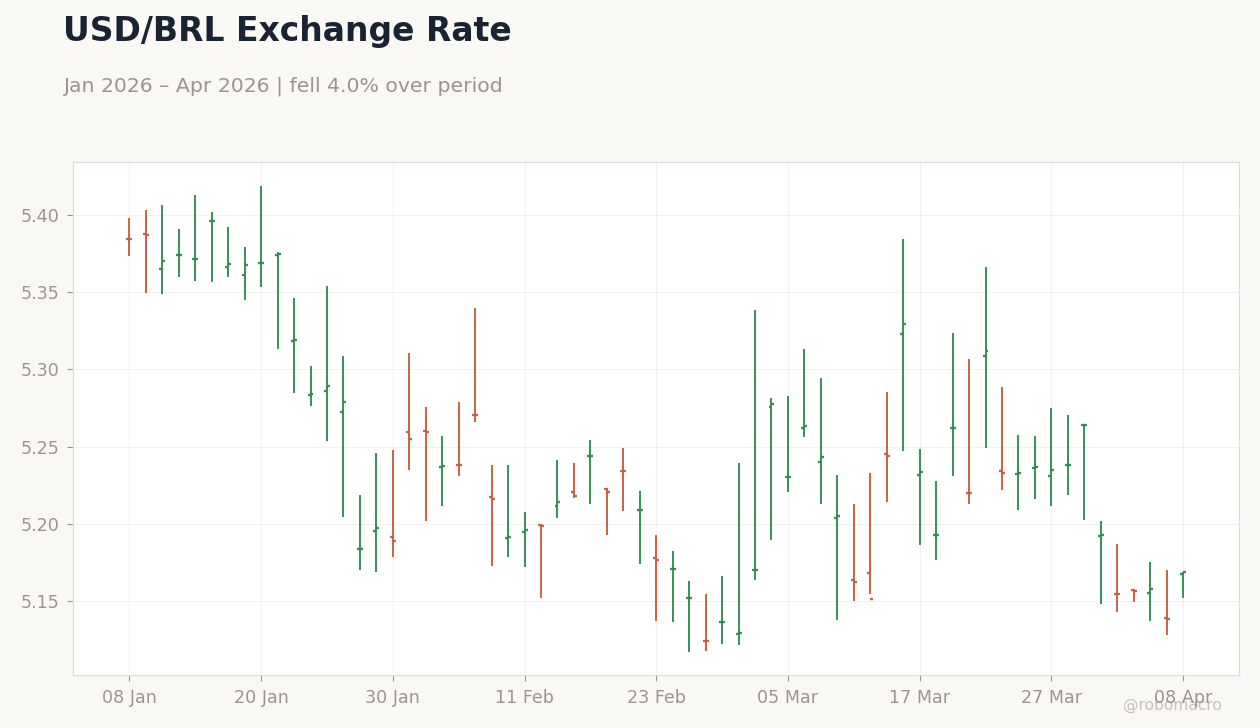

| USD/BRL | 5.17 | +0.59% |

| EUR/BRL | 6.04 | +2.00% |

| Vale | 15.91 | +5.36% |

| Petrobras | 20.75 | -0.29% |

| WTI Crude | 95.19 | -15.72% |

| Gold | 4,824.90 | +3.60% |

| Bitcoin | 71,759.05 | -0.25% |

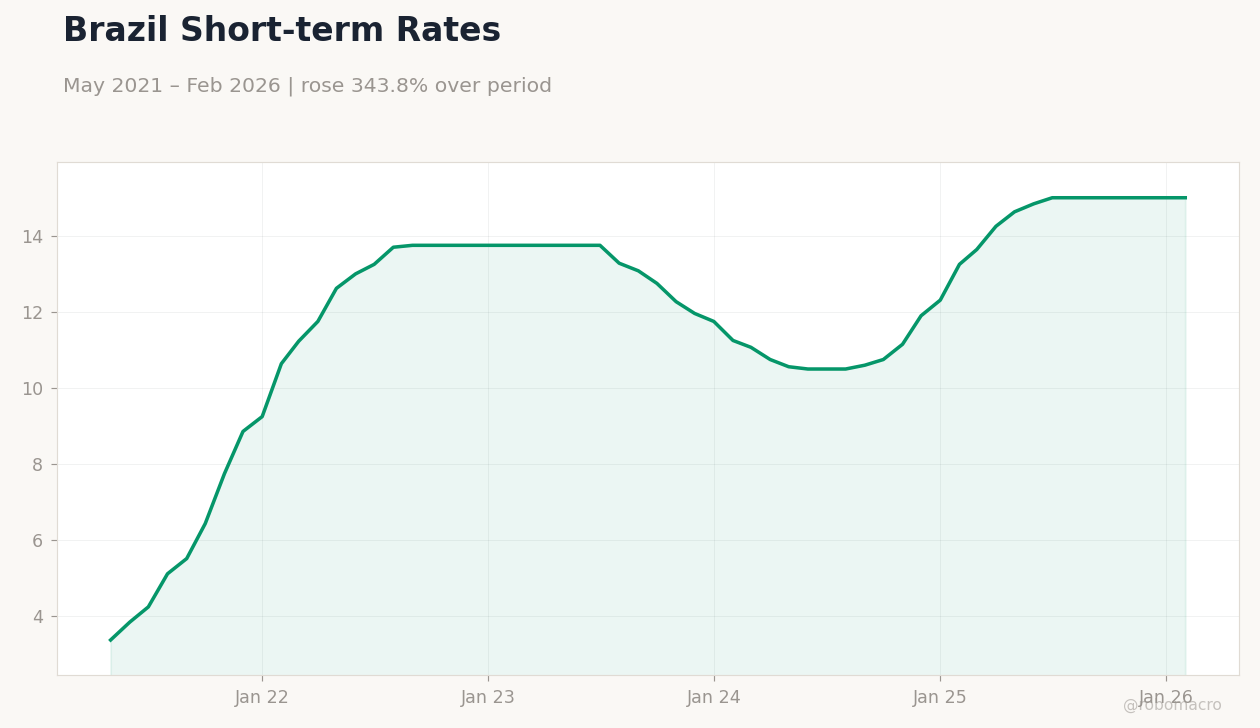

| Brazil Short-term Rate | 15.00% | +0.00% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Services PMI | 53.10 | - | 50.10 |

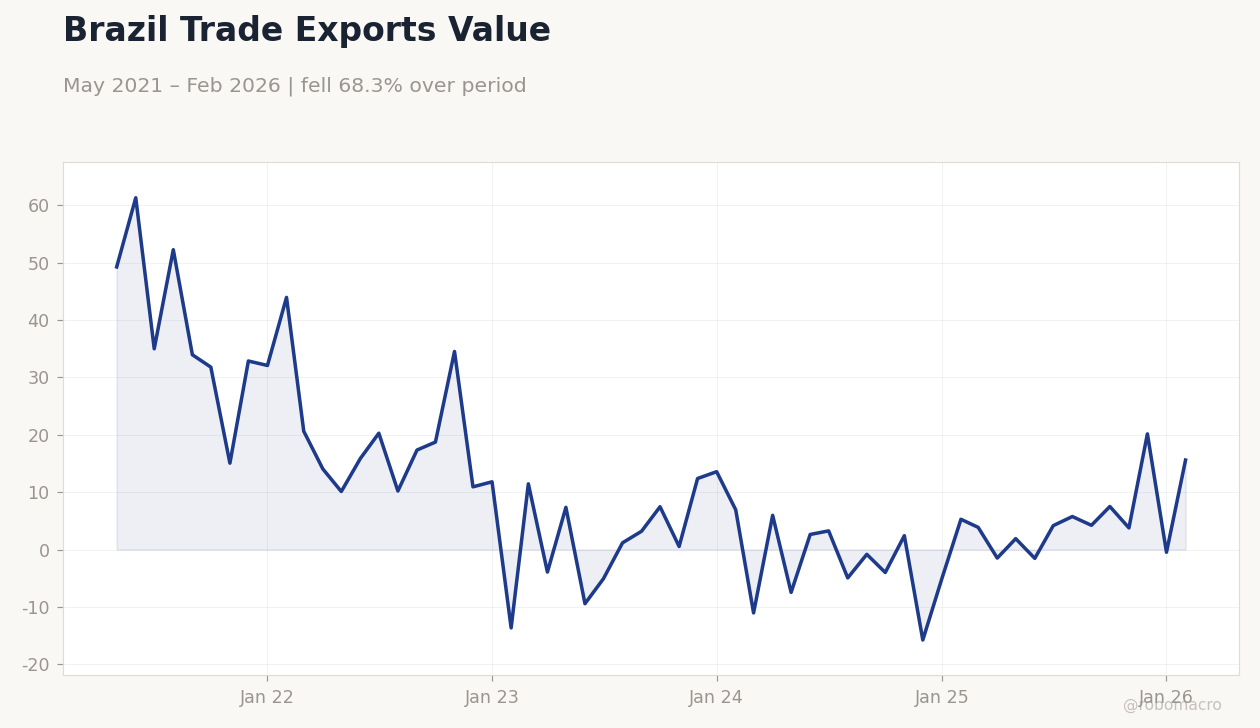

| Trade Balance | 4,210m | 7,400m | 6,400m |

Brazil Trade Exports Value | Type: macro_line | Exports (National Currency): 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 49.25,20.28,3.199,2.423,-0.4707,15.6

Brazil Trade Exports Value | Type: macro_line | Exports (National Currency): 15.6 (2026-02-01) | Range: -15.76–61.3 | Trend(6pt): 49.25,20.28,3.199,2.423,-0.4707,15.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-09) | |||

| Retail Sales Month-over-Month | 0.40 | - | 04:00 |

| Friday (2026-04-10) | |||

| Inflation Rate Month-over-Month | 0.70 | 0.78 | 04:00 |

| Inflation Rate Year-over-Year | 3.81 | 4.04 | 04:00 |

| Business Confidence Index | 46.60 | - | 06:00 |

- Services PMI fell to 50.1, entering contraction on weak demand.

- Trade surplus at $6.4B, below consensus but improved from prior.

- Oil drop pressures assets; Bovespa up slightly on mining gains.

Yesterday's Recap

Brazil's S&P Global Services PMI dropped to 50.1 in March from 53.1 previously, signaling the sector entered contraction for the first time in months and pointing to softening domestic demand. The trade balance for March reached $6.4 billion, missing the $7.4 billion consensus but rising from February's $4.21 billion, supported by commodity exports amid global fluctuations. The Bovespa index ended at 188,259.00 with a 0.05% gain, driven by mining firms like Vale, which rose 5.36% to 15.91 on iron ore momentum.

Petrobras declined 0.29% to 20.75, weighed down by a 15.72% plunge in WTI crude to 95.19 due to easing geopolitical tensions. USD/BRL increased 0.59% to 5.17, reflecting emerging market currency strains, while EUR/BRL advanced 2.00% to 6.04. Brazil's short-term rate remained at 15.00%, with no reported change in long-term rates.

Markets displayed resilience but stayed vulnerable to commodity volatility and fiscal uncertainties.

The Day Ahead

Tomorrow features Brazil's retail sales month-over-month for February, with a prior of 0.4% and no consensus, providing clues on consumer resilience under elevated rates. Friday includes the inflation rate month-over-month for March, expected at 0.78% versus prior 0.7%, and year-over-year inflation forecasted at 4.04% from 3.81%. The business confidence index is set for Friday with a prior of 46.6 and no consensus, gauging private sector views on economic outlook.

These data points may shape expectations for the Selic rate, particularly if inflation exceeds forecasts. No significant BCB activities are planned, though global sentiment could sway Brazilian markets.

Other Economic Notes

Brazil's exports to the US have fallen for the eighth consecutive period, as China strengthens its position as the leading trade partner, altering foreign trade patterns and highlighting dependence on commodities. The government is gearing up for its first euro-denominated debt issuance since 2014, engaging banks such as BBVA, BNP Paribas, BofA Securities, and UBS to access European investors. Labor concerns emerged with BYD added to a blacklist for slave-like conditions at its largest plant outside China, which could deter foreign investments in the sector.

Multiplan's CEO noted that high Selic rates are not impeding growth, emphasizing expansions and experiential strategies.