Brazil Macro Daily(Beta Mode)

Oil Shocks Fuel Brazil Inflation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 195,734.00 | -0.55% |

| USD/BRL | 4.99 | +0.07% |

| EUR/BRL | 5.86 | -0.18% |

| Vale | 17.78 | +2.01% |

| Petrobras | 20.45 | -4.88% |

| WTI Crude | 83.85 | -11.45% |

| Gold | 4,857.60 | +1.51% |

| Bitcoin | 74,770.42 | +1.24% |

| Brazil Short-term Rate | 14.90% | -0.67% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

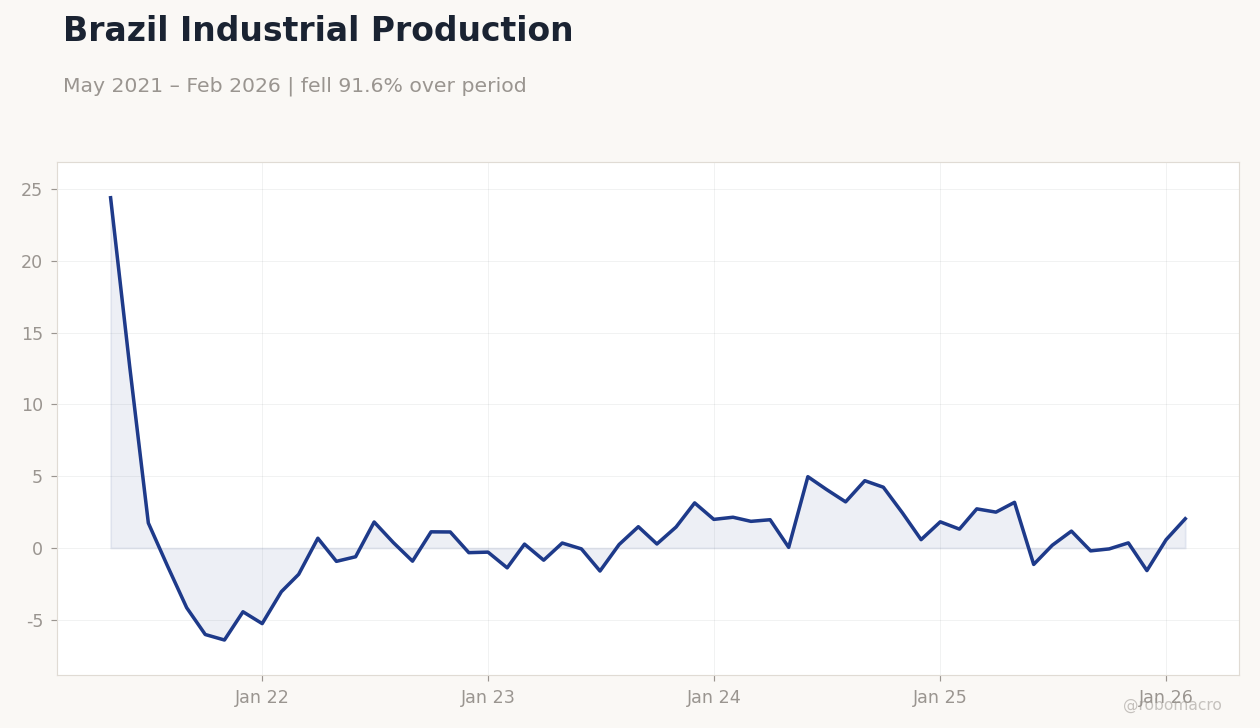

Brazil Industrial Production | Type: macro_line | Ind Prod % YoY: 2.039 (2026-02-01) | Range: -6.408–24.4 | Trend(6pt): 24.4,1.812,1.483,2.437,0.577,2.039

Brazil Industrial Production | Type: macro_line | Ind Prod % YoY: 2.039 (2026-02-01) | Range: -6.408–24.4 | Trend(6pt): 24.4,1.812,1.483,2.437,0.577,2.039

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Oil-driven inflation pressures rise amid Iran conflict, boosting Petrobras but weighing on rates.

- Critical minerals push gains traction with Spain deal and Lula's export focus.

- Markets mixed: Bovespa dips, Real stable despite global volatility.

Yesterday's Recap

Brazilian markets closed mixed on April 19, with the Bovespa index falling 0.55% to 195,734.00 amid broader risk aversion. Petrobras shares dropped sharply by 4.88% to 20.45, pressured by a steep 11.45% decline in WTI crude to 83.85, reflecting global supply concerns. In contrast, Vale stock rose 2.01% to 17.78, supported by firming commodity demand despite iron ore export uncertainties.

The USD/BRL edged up 0.07% to 4.99, while EUR/BRL slipped 0.18% to 5.86, showing mild Real resilience. Brazil's short-term rate eased 0.67% to 14.90%, signaling market bets on potential easing amid disinflation hopes. No major data releases occurred, keeping focus on external shocks like oil volatility.

Overall, equities reflected commodity sector divergences, with no long-term rate data available to gauge bond moves.

The Day Ahead

The calendar remains quiet on April 20 with no scheduled economic releases or events in Brazil. Investors will monitor global oil prices and geopolitical developments for indirect impacts on inflation and exports. Attention turns to potential ad-hoc announcements from the government on critical minerals strategies.

Broader market sentiment may hinge on international news, including any updates from the IMF on energy shock handling. Tomorrow, April 21, also shows no events, extending the lull in domestic data flow. Traders should watch for any unscheduled BCB commentary on rate paths.

Other Economic Notes

Brazil's economy faces headwinds from oil-driven inflation shocks as the Iran conflict persists, complicating fiscal sustainability and export growth. President Lula emphasized tapping critical minerals to avoid missing global opportunities, aligning with a new strategic agreement with Spain to attract investments and dominate key technologies. Endorsement of IMF guidance on energy shocks highlights efforts to mitigate volatility in commodity-dependent sectors like soybeans and iron ore.

Global Macro News

Global markets grapple with the Iran war's fallout, lifting Brazil via higher oil prices but fueling domestic inflation, as noted by the IMF. US instability could brighten Brazil's outlook by diverting investments to emerging markets, per MoneyWeek analysis. (cont...)