Brazil Macro Daily(Beta Mode)

BCB Minutes Highlight Inflation Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 186,754.00 | +0.62% |

| USD/BRL | 4.91 | -1.45% |

| EUR/BRL | 5.78 | -0.78% |

| Vale | 15.93 | +0.57% |

| Petrobras | 21.77 | -1.09% |

| WTI Crude | 94.06 | -8.03% |

| Gold | 4,711.10 | +3.41% |

| Bitcoin | 81,984.54 | +1.31% |

| Brazil Short-term Rate | 14.90% | -0.67% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | - |

Brazil Short-Term Policy Rate | Type: macro_line | Selic Rate %: 14.9 (2026-03-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.9

Brazil Short-Term Policy Rate | Type: macro_line | Selic Rate %: 14.9 (2026-03-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-05-06) | |||

| S&P Global Services PMI | 50.10 | - | 05:00 |

| Thursday (2026-05-07) | |||

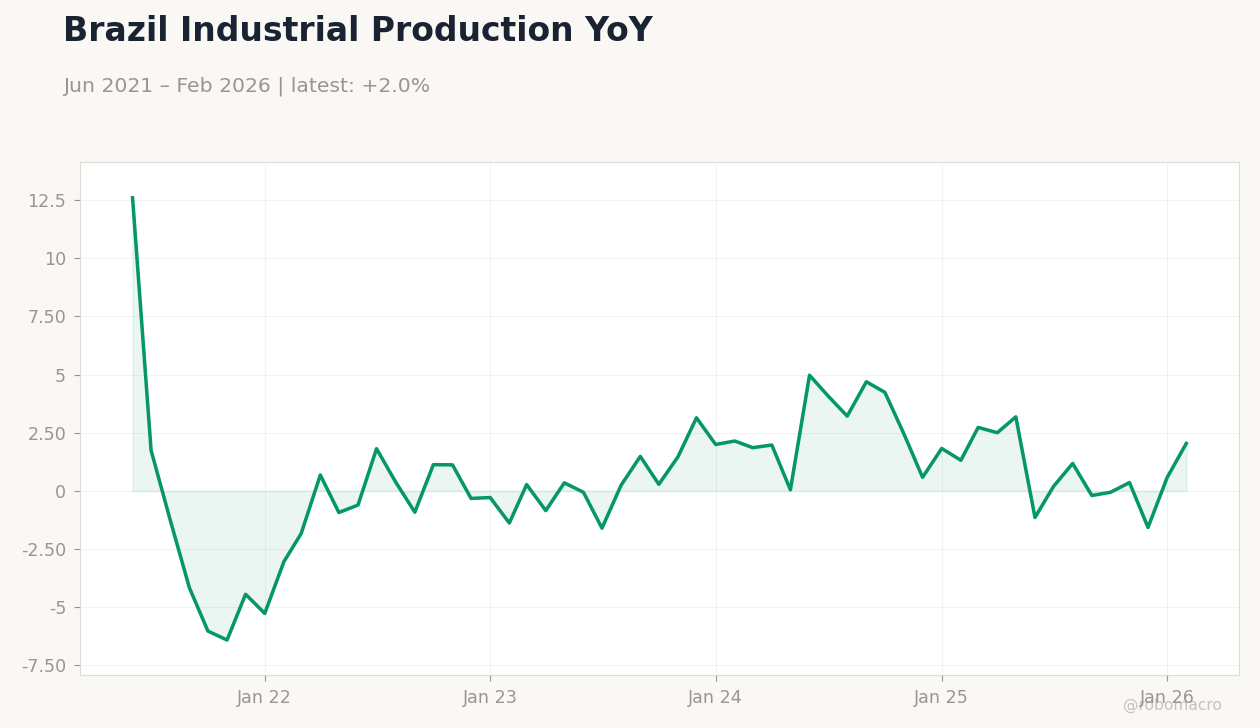

| Industrial Production Month-over-Month | 0.90 | -0.10 | 04:00 |

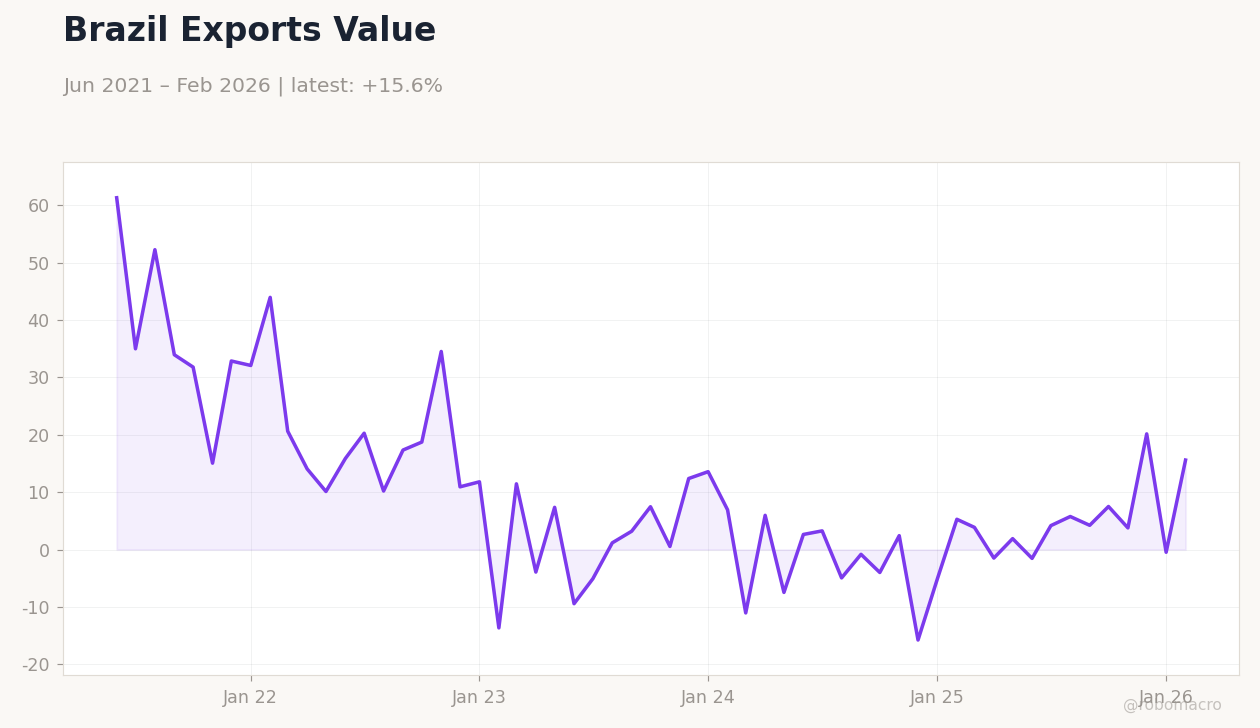

| Trade Balance | 6,410m | 10,900m | 10:00 |

| Friday (2026-05-08) | |||

| Inflation Rate Month-over-Month | 0.88 | - | 04:00 |

| Inflation Rate Year-over-Year | 4.14 | - | 04:00 |

- BCB Copom minutes stress vigilance on supply shocks from Iran conflict, holding Selic at 14.90%.

- Bovespa gains 0.62% on commodity strength, USD/BRL drops 1.45% amid fiscal optimism.

- Debt relief and fuel tax tweaks aim to stabilize revenues despite global tensions.

Yesterday's Recap

The BCB released Copom meeting minutes, underscoring elevated inflation risks from potential supply shocks linked to the Iran conflict, with the committee voting to hold the Selic rate at 14.90%. Brazilian markets displayed strength, as the Bovespa index advanced 0.62% to 186,754, supported by mining sector gains including Vale up 0.57% to 15.93. Petrobras declined 1.09% to 21.77, mirroring an 8.03% drop in WTI crude to 94.06 due to oil market volatility.

The USD/BRL fell 1.45% to 4.91, bolstered by positive fiscal developments, while EUR/BRL decreased 0.78% to 5.78. Gold rose 3.41% to 4,711.10 as a safe haven, and Bitcoin increased 1.31% to 81,984.54. Brazil's short-term rate declined 0.67% to 14.90%, consistent with the BCB's steady policy approach.

Markets overall responded favorably to domestic fiscal adjustments amid external challenges.

The Day Ahead

Tomorrow features the S&P Global Services PMI at 05:00 ET, with a previous of 50.1, which may indicate service sector trends amid ongoing consumer activity. Thursday includes industrial production month-over-month at 04:00 ET, consensus -0.1% against prior 0.9%, potentially affecting manufacturing views if below expectations. Thursday's trade balance at 10:00 ET is forecasted at 10.9 billion versus previous 6.41 billion, reflecting export dynamics in commodities.

Friday brings inflation rate month-over-month and year-over-year at 04:00 ET, with priors of 0.88% and 4.14%, key for shaping BCB policy expectations. These data points could sway Selic forecasts and impact Bovespa performance in industrial segments.

Other Economic Notes

Brazil's debt renegotiation plan provides short-term relief for indebted firms, though eight million companies missing payments highlight strains from high borrowing costs. Efforts to adjust fuel tax rules seek to avert revenue shortfalls, aiding fiscal balance under elevated Selic conditions. Discrimination against LGBTI+ individuals costs the economy billions, affecting productivity and broader growth potential.

(cont...)