Brazil Macro Daily(Beta Mode)

Credit Stimulus Delays Brazil Rate Cuts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 177,284.00 | -0.61% |

| USD/BRL | 5.07 | +1.31% |

| EUR/BRL | 5.90 | +1.22% |

| Vale | 16.32 | -1.57% |

| Petrobras | 19.93 | +0.76% |

| WTI Crude | 101.76 | -3.47% |

| Gold | 4,558.10 | +0.05% |

| Bitcoin | 76,989.61 | -0.57% |

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Policy Rate | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Brazil Policy Rate | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bovespa fell 0.61% to 177,284 while USD/BRL rose 1.31% to 5.07 on credit stimulus concerns.

- Brazil short-term rate held at 14.75% as markets priced slower easing amid fiscal support measures.

- Bank of America highlighted Brazil as top EM opportunity outside China with record capital inflows.

Yesterday's Recap

Bovespa closed lower at 177,284 amid broad equity weakness, with Vale dropping 1.57% to 16.32 while Petrobras gained 0.76% to 19.93. USD/BRL climbed to 5.07 as the real underperformed peers on fresh credit stimulus headlines. The short-term rate remained at 14.75%, reflecting limited immediate policy shift.

WTI crude fell 3.47% to 101.76, pressuring commodity-linked names despite steady iron-ore demand from China. Gold held near 4,558 with minimal movement. News flow centered on potential credit measures that could delay Selic cuts, while Lula prepared for economy talks with Trump.

Carry-trade flows supported the real against more volatile currencies despite the day's losses.

The Day Ahead

Markets will monitor any follow-up statements on credit stimulus and its inflation impact. Lula's scheduled White House discussion with Trump on trade and investment could shape sentiment toward Brazilian assets. BofA's constructive view on $96 billion inflows and $11 trillion US capital pool may support equity positioning.

Fiscal anchor debates remain in focus after recent primary deficit data. No major releases are scheduled, leaving room for global risk factors to drive BRL and Bovespa moves. Participants will watch for any clarification on the timing of potential rate adjustments.

Other Economic Notes

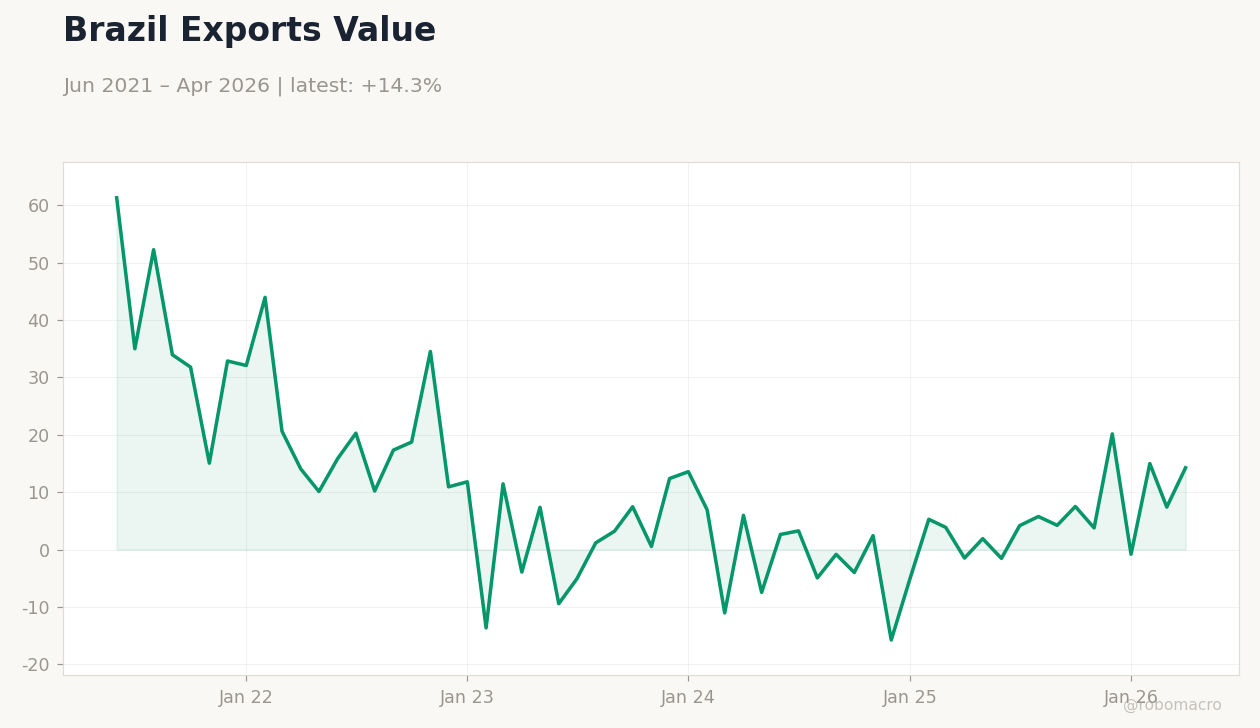

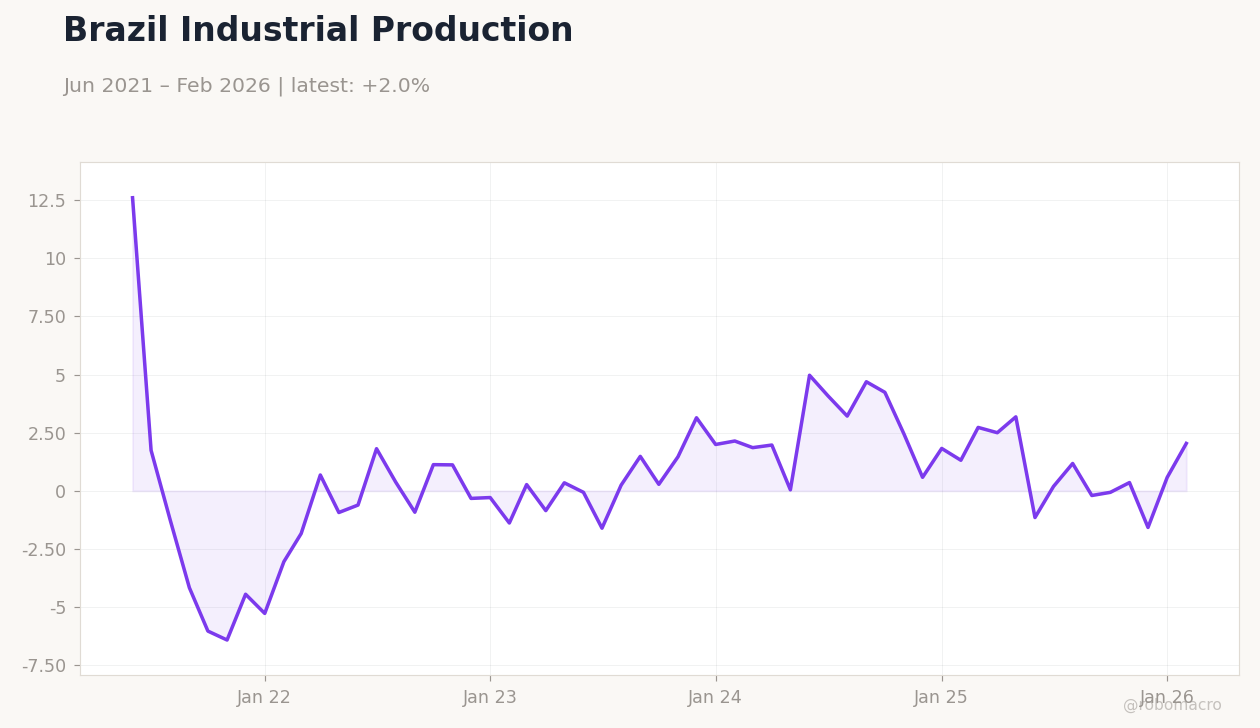

Credit stimulus measures risk extending the period of elevated borrowing costs, according to Valor International reporting. Primary deficit pressures continue to test the 2027 fiscal framework amid steady commodity export revenues. BofA analysts see Brazil entering its strongest expansion phase since 2011, driven by external demand for soybeans and iron ore.

Infrastructure projects tied to the Kubitschek-era legacy continue to underpin long-term growth narratives. Safe-haven flows have favored select Brazilian utilities and banks over cyclical sectors during global volatility.