Brazil Macro Daily(Beta Mode)

Brazil Q1 GDP Holds at 1.3% as March Cools

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 176,976.00 | -0.17% |

| USD/BRL | 5.01 | -0.93% |

| EUR/BRL | 5.82 | -0.84% |

| Vale | 16.31 | -0.06% |

| Petrobras | 20.70 | +3.86% |

| WTI Crude | 103.12 | -5.10% |

| Gold | 4,548.90 | -0.08% |

| Bitcoin | 76,961.63 | +0.01% |

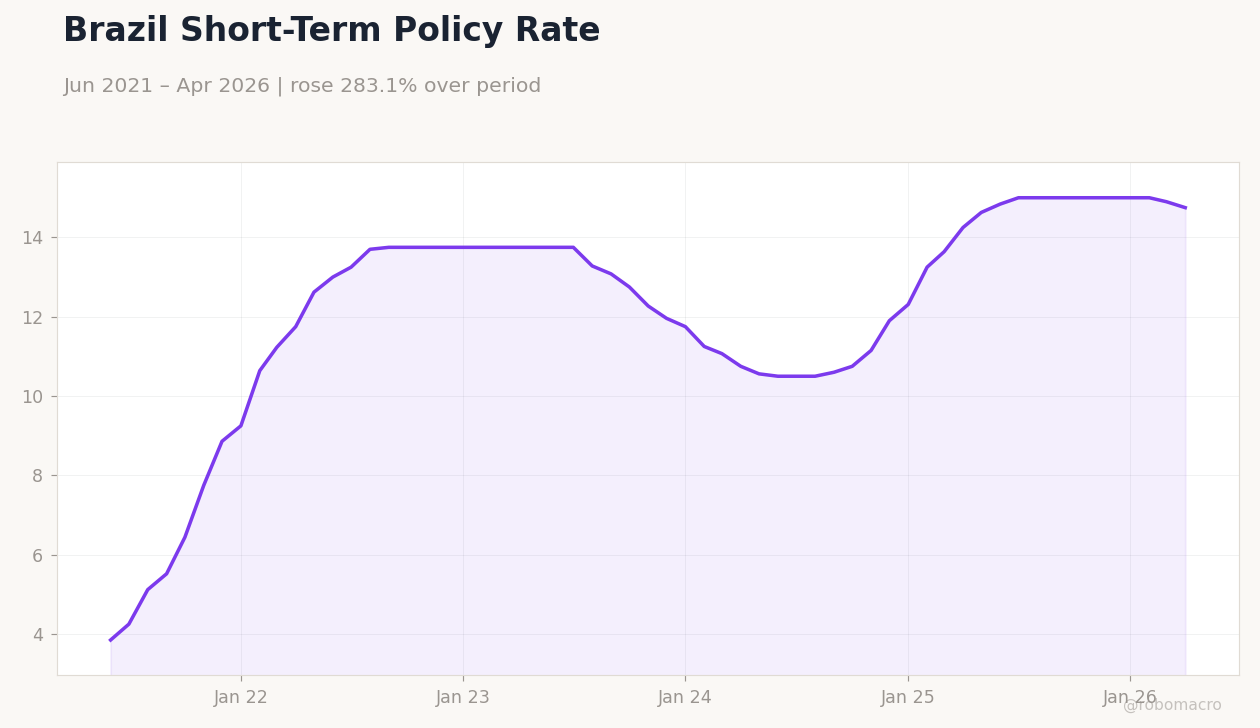

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

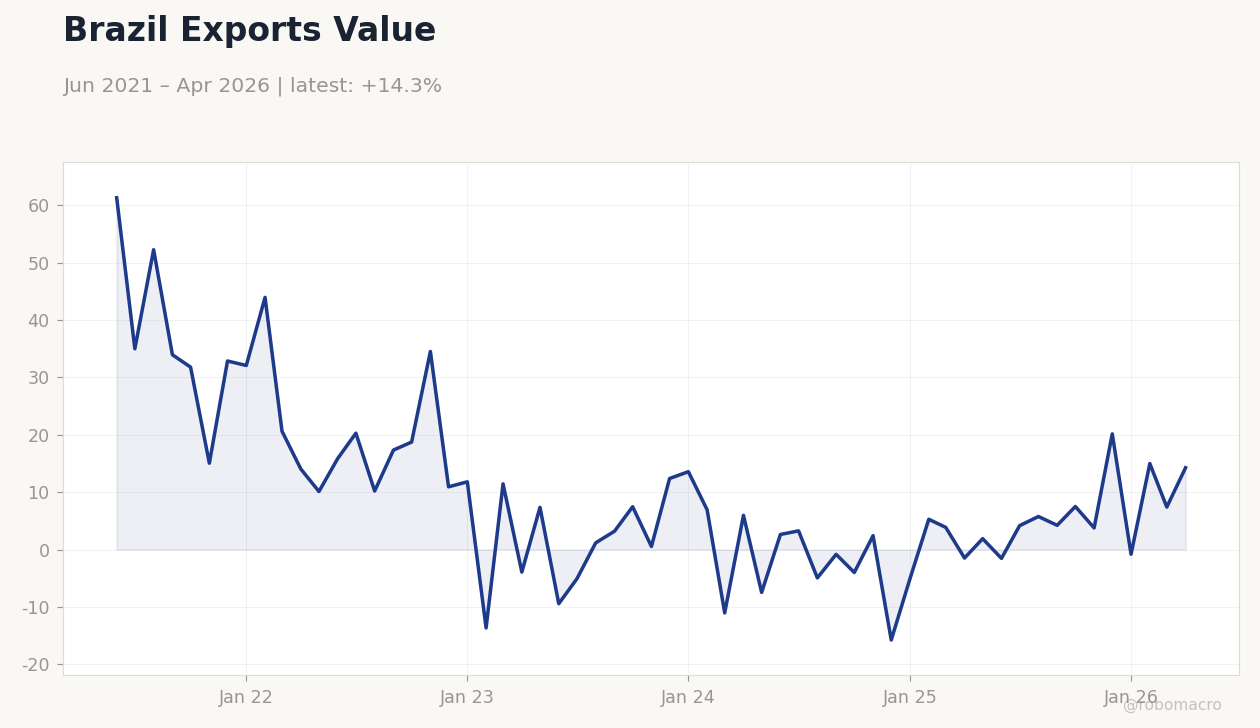

Brazil Exports Value | Type: macro_line | USD mn: 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Brazil Exports Value | Type: macro_line | USD mn: 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brazil’s economy expanded 1.3% in Q1, though March activity fell sharply and signaled cooling momentum into an election year.

- BRL strengthened notably with USD/BRL falling 0.93% to 5.01 while Bovespa slipped 0.17% to 176,976 amid mixed commodity moves.

- Markets now price higher Selic through 2026 as analysts lift inflation and rate forecasts for the tenth straight week.

Yesterday's Recap

Brazil reported 1.3% Q1 GDP growth that beat some expectations yet came with a steep March contraction that points to fading momentum. Bovespa closed down 0.17% at 176,976 while Petrobras shares jumped 3.86% to 20.70. USD/BRL dropped 0.93% to 5.01 and EUR/BRL fell 0.84% to 5.82, reflecting broad BRL support from softer inflation prints and steady commodity exports.

WTI crude plunged 5.10% to 103.12, weighing on energy names, while the short-term rate held at 14.75% after a 1.01% daily decline. Iron-ore and soybean export outlooks remained constructive despite the March slowdown, keeping fiscal and trade-balance narratives intact. No major data releases occurred yesterday, leaving markets to digest the GDP print and analyst revisions to 2026 rate and inflation paths.

The Day Ahead

The calendar stays light with no scheduled releases or COPOM events through tomorrow. Focus shifts to follow-up commentary on Q1 GDP components and any retail-sales or industrial-production surprises that could alter growth forecasts. Analysts will continue revising 2026 Selic and inflation projections after the latest Focus survey lift.

BRL and front-end yields may react to any fresh fiscal or drought-relief spending updates. Markets will also monitor global oil and iron-ore price swings for export revenue implications. No speeches from COPOM members are listed, keeping policy signals quiet until the next inflation print.

Other Economic Notes

Brazil already holds ample capital for green-economy projects yet still lacks efficient matching between investors and bankable initiatives. Energy-transition potential remains high given rare natural assets, but execution capacity and regulatory clarity continue to lag. Fiscal space faces renewed pressure after the R$15 billion drought-relief supplement widened the 2026 primary-deficit projection.

These themes reinforce the need for structural reforms to convert resource wealth into sustained productivity gains.