Brazil Macro Daily(Beta Mode)

Bovespa Rises as Real Firms on Commodity Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 177,356.00 | +1.77% |

| USD/BRL | 5.00 | -1.08% |

| EUR/BRL | 5.79 | -1.20% |

| Vale | 16.35 | +2.12% |

| Petrobras | 19.83 | -2.84% |

| WTI Crude | 99.01 | +0.76% |

| Gold | 4,533.50 | +0.05% |

| Bitcoin | 77,835.26 | +0.49% |

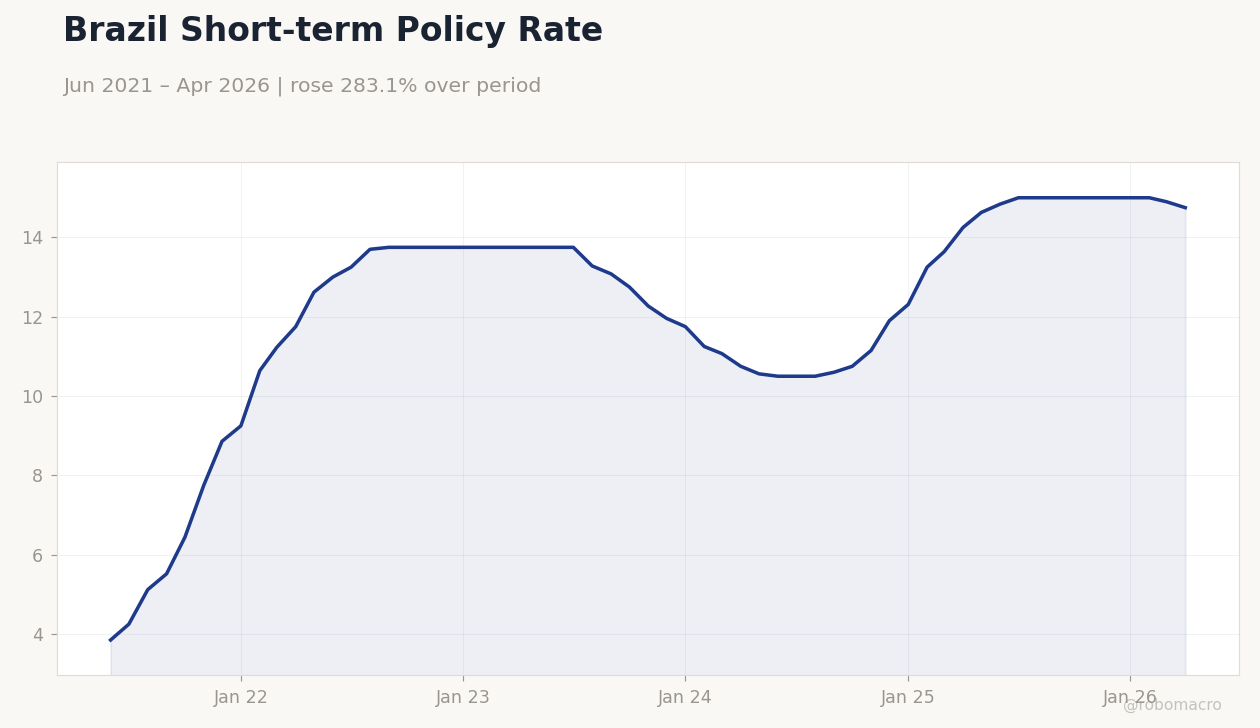

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Brazil Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bovespa rises 1.77% to 177,356 driven by Vale gains and firmer iron-ore prices

- USD/BRL falls 1.08% to 5.00 while short-term rates ease to 14.75%

- Lower pension backlog boosts fiscal spending and supports near-term growth outlook

Yesterday's Recap

Brazilian equities advanced sharply with the Bovespa closing 1.77% higher at 177,356 as Vale shares climbed 2.12% on resilient iron-ore demand. The real strengthened notably, sending USD/BRL down 1.08% to 5.00 and EUR/BRL 1.20% lower to 5.79. Petrobras shares declined 2.84% despite WTI crude rising 0.76% to 99.01, reflecting profit-taking after recent oil strength.

Short-term Brazilian rates eased 1.01% to 14.75% while gold held steady near 4,533.50. News that lower pension backlogs are driving higher public spending added to positive fiscal sentiment. A new federal measure expanding waste use in biofuel production reinforced Brazil’s circular-economy push and long-term energy strategy.

Markets also noted Brazil’s readiness to increase oil exports to Japan amid steady global demand.

The Day Ahead

The domestic calendar remains light with no major data releases scheduled for May 22. Attention will stay on ongoing fiscal developments and the Treasury’s debt issuance schedule. Global oil-market signals and any updates on U.S.-Iran talks could influence Petrobras and broader commodity names.

Investors will monitor iron-ore futures and Chinese import data for further equity direction. Biofuel policy implementation details may surface and affect energy-related credits.

Other Economic Notes

A recent study underscores the need for a fresh investment cycle to sustain Brazil’s growth momentum beyond current commodity tailwinds. Fiscal accounts benefit from reduced pension processing delays, trimming near-term borrowing requirements. The government’s biofuel initiative integrates circular-economy principles and targets lower carbon intensity in transport by 2030.

These measures support Brazil’s external accounts while commodity exports remain the dominant growth driver.

Global Macro News

WTI crude held above 99 amid tighter OPEC+ compliance and firm Chinese demand, aiding Brazil’s oil export outlook. The Russian ruble’s strong performance highlights how high commodity revenues and capital controls can stabilize emerging-market currencies. <i>↓ p.2</i>