Brazil Macro Daily(Beta Mode)

BRL Strengthens as Equities Rise, Oil Drops

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 177,359.00 | +0.65% |

| USD/BRL | 5.02 | -0.19% |

| EUR/BRL | 5.81 | -0.55% |

| Vale | 16.48 | +0.06% |

| Petrobras | 19.90 | -0.65% |

| WTI Crude | 93.43 | -3.28% |

| Gold | 4,523.00 | +0.04% |

| Bitcoin | 76,652.14 | -0.81% |

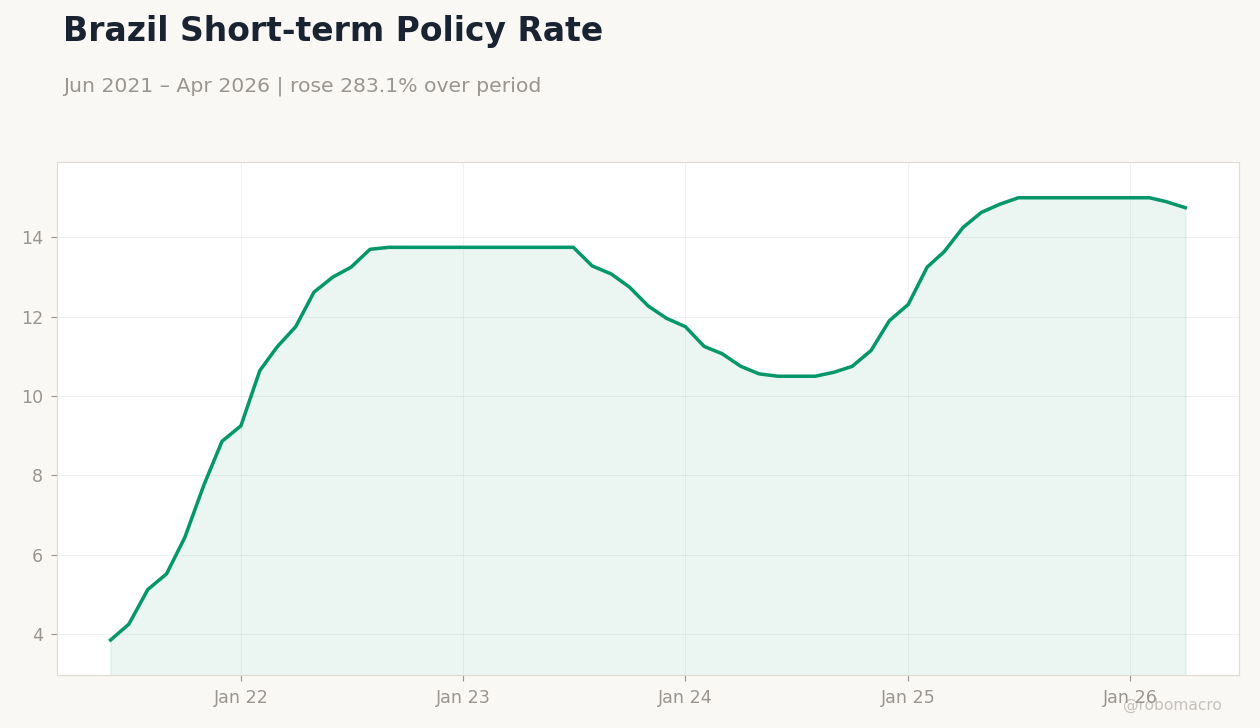

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Exports Value | Type: macro_line | Exports (YoY %): 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Brazil Exports Value | Type: macro_line | Exports (YoY %): 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-28) | |||

| Headline Unemployment Rate | 6.10 | - | 04:00 |

| Friday (2026-05-29) | |||

| GDP Growth Quarter-over-Quarter | 0.10 | - | 04:00 |

| GDP Growth Year-over-Year | 1.80 | - | 04:00 |

- Bovespa rises 0.65% to 177,359 on iron-ore support while oil falls 3.28%.

- USD/BRL drops to 5.02 as short-term rates ease 1.01% to 14.75%.

- Markets await May unemployment print amid Brazil’s widening debt arrears.

Yesterday's Recap

Equity and currency markets advanced on May 25 despite softer commodity prices. Bovespa closed at 177,359 after a 0.65% gain, led by Vale’s modest advance. USD/BRL fell 0.19% to 5.02 while EUR/BRL declined 0.55% to 5.81.

WTI crude dropped sharply to 93.43, pressuring Petrobras shares 0.65% lower to 19.90. The Brazil short-term rate eased to 14.75%, reflecting reduced near-term policy pressure. No macroeconomic releases occurred, leaving price action driven by external oil negotiations and iron-ore futures.

Gold held steady near 4,523 while Bitcoin slipped 0.81%.

The Day Ahead

IBGE will release the headline unemployment rate on May 28 at 04:00 ET. The print follows April’s 6.1% reading and carries medium market impact. On May 29, quarterly and annual GDP figures are due at the same hour.

Traders will assess whether labor-market resilience offsets the recent debt-servicing deterioration. No Copom speakers are scheduled before the releases. Markets currently assign low probability to near-term Selic adjustments.

Other Economic Notes

More than 82 million Brazilians remain behind on payments, swelling the debt stock and constraining consumption. The foreign minister signaled renewed efforts to diversify export destinations beyond traditional partners. Fiscal data showed a primary surplus in April, yet medium-term sustainability concerns persist.

Iron-ore output gains in China provided limited relief to Vale-linked revenues. These factors keep the yield curve sensitive to external commodity swings.

Global Macro News

Progress in US-Iran talks drove WTI crude down nearly 6% and eased imported inflation risks for Brazil. India’s officials moved to calm markets after oil spikes weighed on growth and the rupee. Sri Lanka raised rates 100 bp to defend its currency amid regional energy stress.

<i>↓ p.2</i>