Brazil Macro Daily(Beta Mode)

Brazil Inflation Tops Target on Food Costs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 175,744.00 | -0.48% |

| USD/BRL | 5.06 | +0.28% |

| EUR/BRL | 5.85 | -0.26% |

| Vale | 16.51 | +0.06% |

| Petrobras | 18.96 | -2.27% |

| WTI Crude | 90.63 | +2.20% |

| Gold | 4,420.20 | -0.61% |

| Bitcoin | 73,192.90 | -1.55% |

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

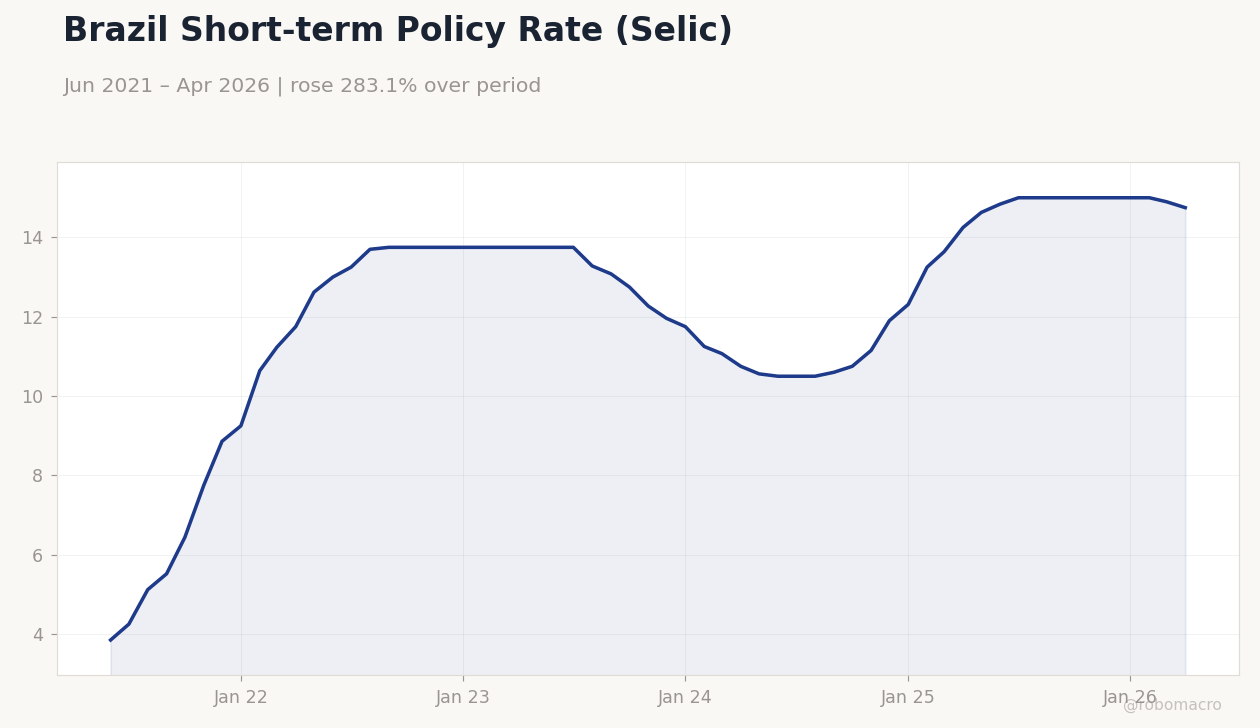

Brazil Short-term Policy Rate (Selic) | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Brazil Short-term Policy Rate (Selic) | Type: macro_line | Policy Rate %: 14.75 (2026-04-01) | Range: 3.85–15 | Trend(6pt): 3.85,13.7,12.75,11.9,15,14.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6.10 | 5.90 | 04:00 |

| Friday (2026-05-29) | |||

| GDP Growth Quarter-over-Quarter | 0.10 | 1 | 04:00 |

| GDP Growth Year-over-Year | 1.80 | 1.80 | 04:00 |

- May inflation hit 0.62%, breaching the BCB target ceiling amid food and housing pressures.

- Unemployment data due today with consensus at 5.9%, followed by Q1 GDP prints tomorrow.

- Selic steady at 14.75% as BCB maintains tight policy amid rising external deficit of $1.7bn.

Yesterday's Recap

Bovespa closed 0.48% lower at 175,744 while USD/BRL rose 0.28% to 5.06 amid broad dollar strength. Petrobras shares fell 2.27% to 18.96 as oil volatility weighed on sentiment. Brazil recorded a $1.7bn current account deficit in April, widening external imbalances.

May inflation printed 0.62%, the highest monthly reading since 2016 and above the upper bound of the BCB target range. Food and housing components drove the overshoot, prompting Itaú to flag risks that an oil price shock could push inflation further above forecasts. Short-term rates stood at 14.75%, reflecting market pricing of steady policy.

Vale held near flat at 16.51 despite firmer iron ore prices.

The Day Ahead

Markets will focus on the Headline Unemployment Rate release at 04:00 ET, expected to fall to 5.9% from 6.1%. Tomorrow brings Q1 GDP data with quarter-over-quarter growth forecast at 1.0% versus 0.1% prior and year-over-year at 1.8%. Analysts will assess whether stronger activity readings alter the inflation outlook.

BCB speakers have no scheduled appearances, leaving recent COPOM minutes as the main policy reference. Commodity flows will also matter given China’s suspension of Brazilian beef imports.

Other Economic Notes

Persistent double-digit Selic rates continue to anchor inflation expectations but weigh on credit growth and fiscal costs. The external deficit expansion highlights vulnerability to commodity price swings and terms-of-trade shocks. High real rates support BRL carry trades yet limit fiscal space for counter-cyclical measures.

Economists note that structural factors, including indexation and public spending rigidity, keep the neutral rate elevated. Petrobras investment announcements in Amazonas add to capex visibility but face execution risks.

Global Macro News

WTI crude rose 2.20% to 90.63, amplifying Itaú’s warning on second-round inflation effects for Brazil. China’s beef import suspension threatens soybean and meat export revenues, a key support for the trade balance. <i>↓ p.2</i>