Brazil Macro Daily(Beta Mode)

Unemployment Beats as GDP Data Looms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 175,063.00 | -0.39% |

| USD/BRL | 5.03 | -0.80% |

| EUR/BRL | 5.85 | -0.59% |

| Vale | 16.55 | +0.24% |

| Petrobras | 18.83 | -0.69% |

| WTI Crude | 87.42 | -1.66% |

| Gold | 4,558.60 | +1.32% |

| Bitcoin | 73,761.93 | +0.31% |

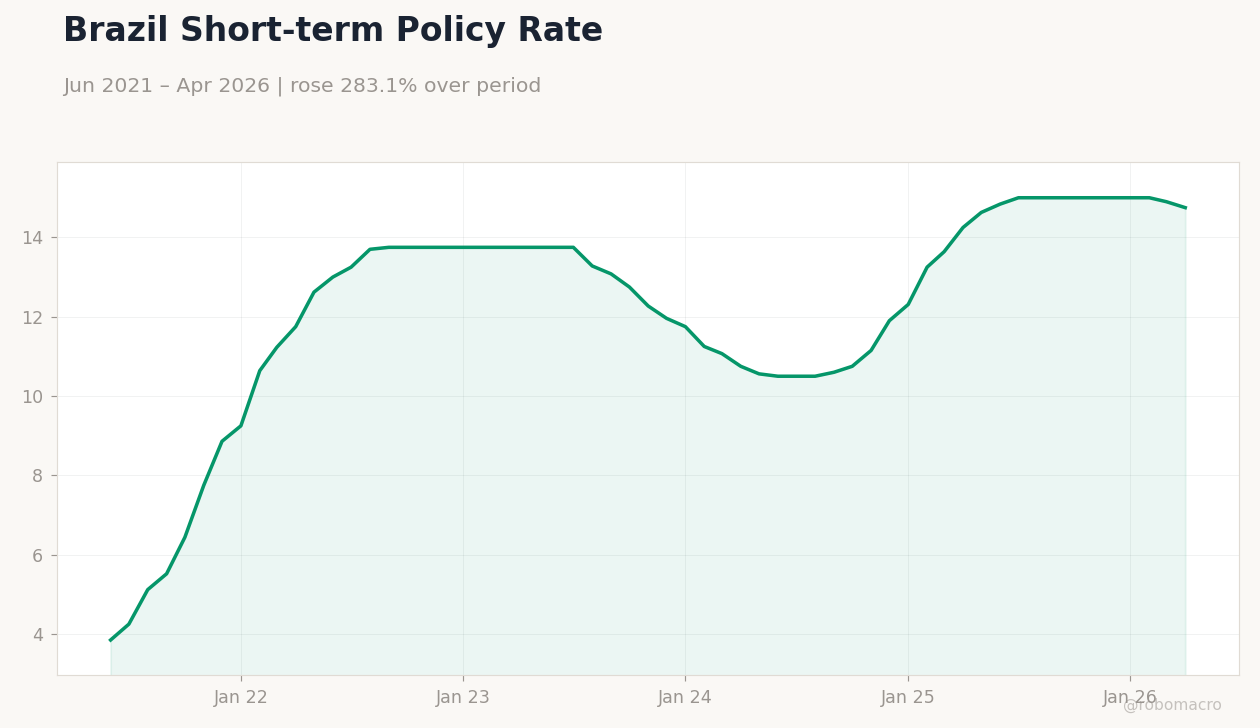

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 6.10 | 5.90 | 5.80 |

Brazil Exports Value | Type: macro_line | Exports (USD mn): 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Brazil Exports Value | Type: macro_line | Exports (USD mn): 14.26 (2026-04-01) | Range: -15.76–61.3 | Trend(6pt): 61.3,10.2,7.464,-15.76,14.99,14.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.10 | 1 | 04:00 |

| GDP Growth Year-over-Year | 1.80 | 1.80 | 04:00 |

- Unemployment rate falls to 5.8%, beating consensus and signaling labor-market resilience.

- Bovespa slips 0.39% while USD/BRL strengthens 0.80% on firmer real yields.

- Selic remains at 14.75% as BCB flags rising 2028 inflation expectations.

Yesterday's Recap

Brazil’s headline unemployment rate declined to 5.8% in April, undershooting the 5.9% consensus and extending the prior month’s improvement. The print reinforced views of a still-tight labor market despite earlier concerns over formal job creation missing forecasts. Bovespa closed 0.39% lower at 175,063 amid profit-taking in Petrobras, which fell 0.69%.

USD/BRL dropped 0.80% to 5.03, reflecting BRL strength as the short-term rate eased 1.01% to 14.75%. Vale edged 0.24% higher on stable iron-ore prices while WTI crude fell 1.66% to 87.42. Gold rose 1.32% to 4,558.60, providing a modest hedge for commodity-linked assets.

No COPOM speakers emerged to alter the hold stance priced into the curve.

The Day Ahead

Markets will receive first-quarter GDP figures at 04:00 ET, with quarter-over-quarter growth expected to rebound to 1.0% from 0.1% and year-over-year growth holding at 1.8%. Analysts attribute the pickup to fiscal stimulus and a manufacturing rebound that lifted industrial output. A print in line with or above consensus would support BRL and trim any residual 2026 easing bets.

No other high-impact Brazilian releases are scheduled through the weekend. Traders will also monitor Petrobras gasoline price adjustments effective tomorrow for any pass-through to May inflation.

Other Economic Notes

Formal job creation in April undershot all analyst estimates, raising questions about the durability of recent employment gains. Central bank director Nilton David highlighted growing concern over 2028 inflation expectations, underscoring the need to keep policy restrictive. Fiscal accounts showed a wider primary deficit revision for 2026 that markets largely viewed as already priced.

Commodity export revenues remain supportive, with the April trade surplus hitting a monthly record on soy and oil shipments.

Global Macro News

China’s May manufacturing PMI beat expectations, lifting iron-ore futures and providing a tailwind for Vale. WTI crude declined 1.66% on softer global demand signals despite OPEC+ supply discipline. <i>↓ p.2</i>