Brazil Macro Daily(Beta Mode)

Brazil IP Data and US Tariffs in Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 174,198.00 | +1.16% |

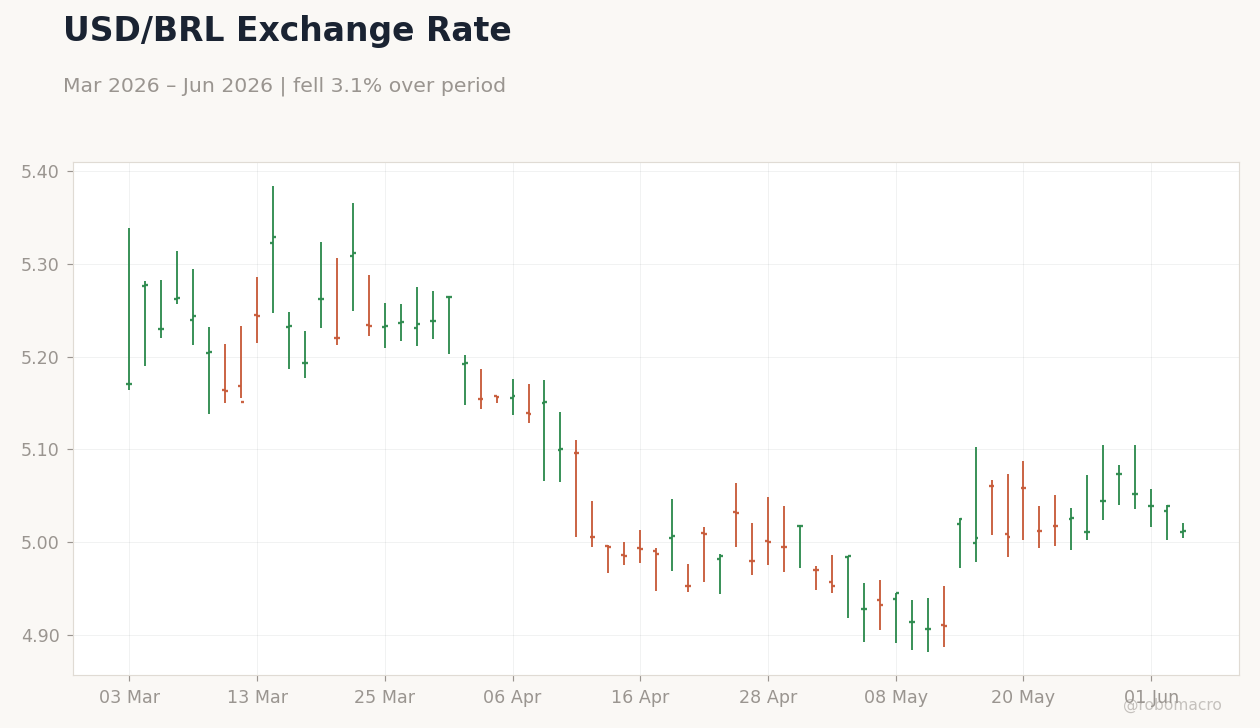

| USD/BRL | 5.01 | -0.54% |

| EUR/BRL | 5.82 | -0.67% |

| Vale | 16.82 | +3.19% |

| Petrobras | 18.72 | -0.74% |

| WTI Crude | 96.26 | +2.67% |

| Gold | 4,474.90 | -0.32% |

| Bitcoin | 66,933.99 | +0.35% |

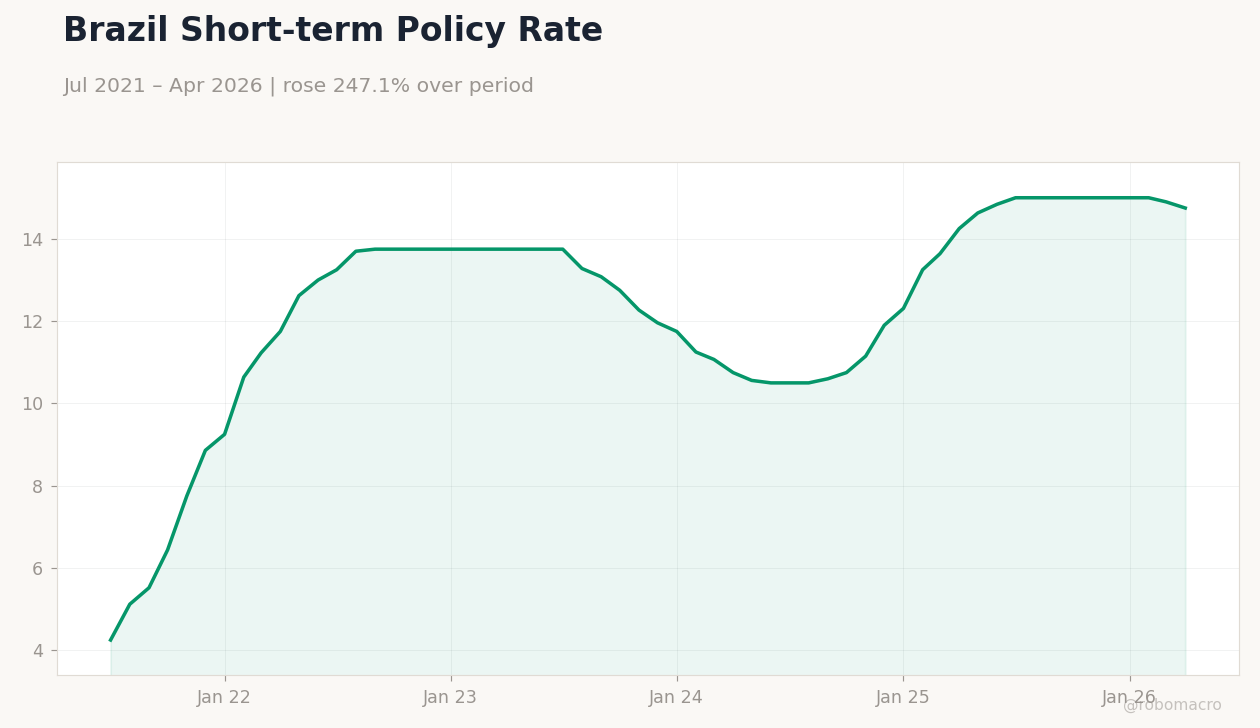

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

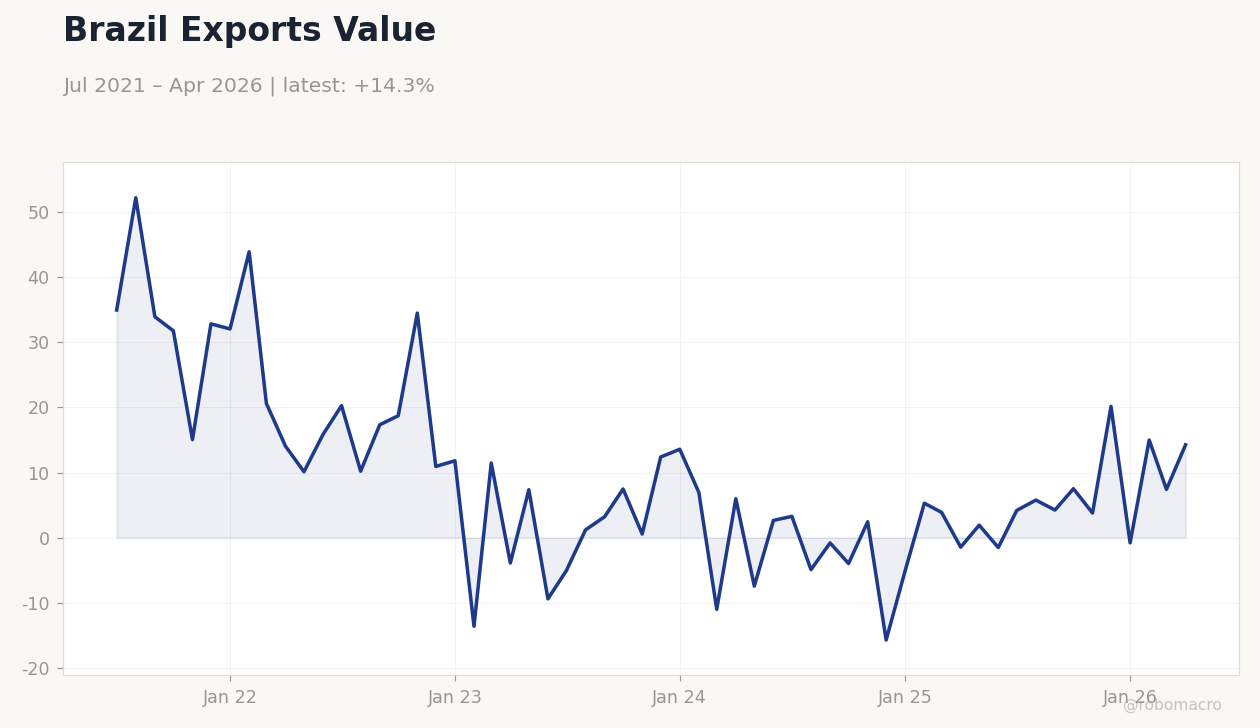

Brazil Exports Value | Type: macro_line | USD millions: 14.26 (2026-04-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.406,14.26

Brazil Exports Value | Type: macro_line | USD millions: 14.26 (2026-04-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.406,14.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | 0.10 | 0.40 | 04:00 |

| S&P Global Services PMI | 52.30 | - | 05:00 |

| Trade Balance | 10,540m | 7,650m | 10:00 |

- Industrial production and trade balance releases today may shift Q2 GDP views

- Bovespa gains 1.16% to 174,198 while USD/BRL drops to 5.01 on risk appetite

- Santander estimates shorter workweek could trim Brazil GDP by 2.5%

Yesterday's Recap

Markets closed higher on June 2 with Bovespa advancing 1.16% to 174,198 led by Vale’s 3.19% rally on iron-ore strength. USD/BRL fell 0.54% to 5.01 and EUR/BRL eased 0.67% to 5.82 as commodity currencies benefited from firmer WTI crude at 96.26. Petrobras slipped 0.74% while short-term rates held at 14.75%.

No economic data printed, leaving focus on external drivers and tariff headlines. Iron-ore exports and tourism inflows provided underlying support for equities. The session reflected steady foreign appetite for Brazilian assets despite looming US trade measures.

The Day Ahead

Industrial production month-over-month is due at 04:00 ET with consensus at 0.4% after 0.1% prior. S&P Global Services PMI follows at 05:00 ET, tracking service-sector momentum after last month’s 52.3 reading. Trade balance data at 10:00 ET is expected to show a US$7.65 bn surplus versus US$10.54 bn previously.

Weak IP could reinforce expectations for policy easing later this year. Markets will parse the prints for implications on Q2 activity and the Selic path. No COPOM speakers are scheduled.

Other Economic Notes

Santander analysis highlights that a shorter workweek risks shaving 2.5% from annual GDP through reduced output and labor costs. Fiscal targets remain anchored after the Treasury set a R$25 bn primary deficit goal for 2026. Tourism job creation and visitor spending reached record levels, adding a positive buffer to services activity.

BRICS engagement with China continues to support commodity export revenues, particularly iron ore and soybeans. These themes offset some external tariff pressure in the near term.

Global Macro News

The Trump administration proposed 25% tariffs on Brazilian goods citing unfair trade practices including PIX and digital piracy concerns. The measures come despite a US trade surplus with Brazil and would replace earlier 50% duties on select items. Strategic sectors appear spared from the new tariff list.

President Lula is set to discuss economy and security at the White House, seeking to ease tensions. BRICS coordination with China offers Brazil alternative export channels if tariffs materialize. <i>↓ p.2</i>