Brazil Macro Daily(Beta Mode)

IP Beat Offset by Tariff Threat to BRL

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 170,331.00 | -2.22% |

| USD/BRL | 5.08 | +1.10% |

| EUR/BRL | 5.90 | +1.15% |

| Vale | 16.06 | -4.52% |

| Petrobras | 18.19 | -2.83% |

| WTI Crude | 94.75 | -1.32% |

| Gold | 4,489.80 | +1.20% |

| Bitcoin | 62,991.89 | -1.60% |

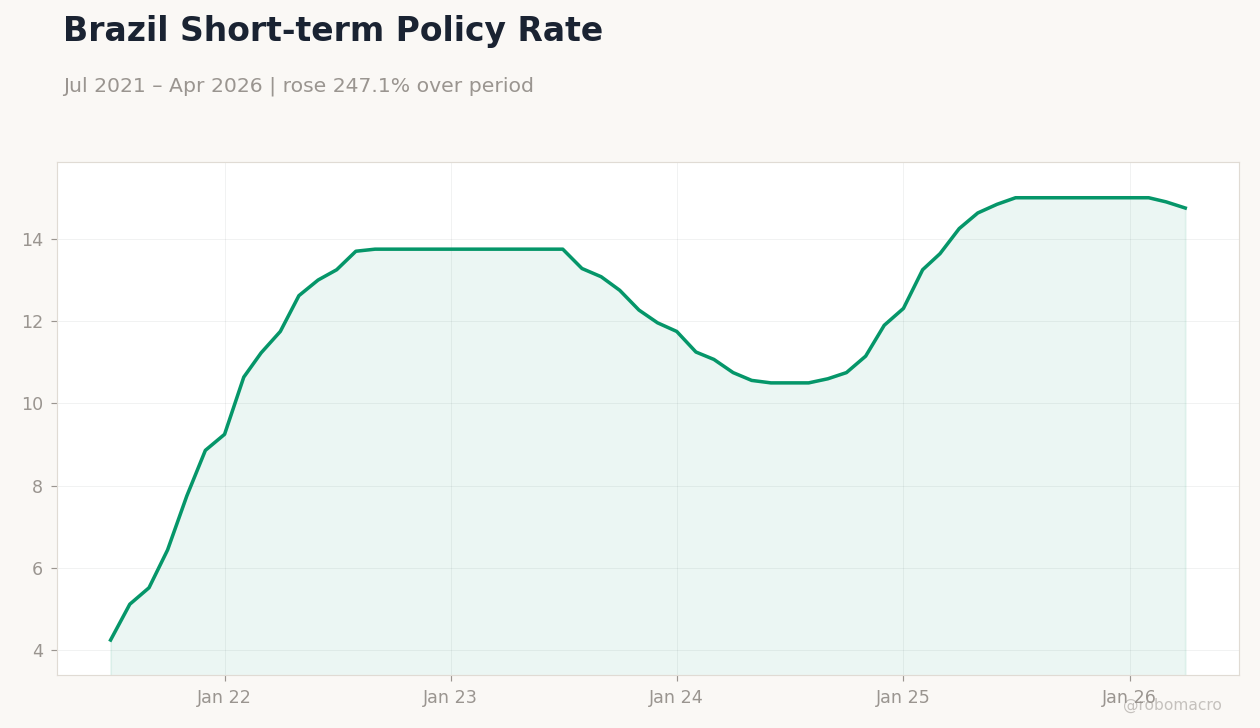

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Industrial Production Month-over-Month | 0.30 | 0.40 | 0.70 |

| S&P Global Services PMI | 52.30 | - | 50.40 |

| Trade Balance | 10,540m | 7,650m | 7,820m |

Brazil Trade Balance | Type: macro_line | USD mn: -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(5pt): -6.917e+04,-6.778e+04,-6.505e+04,-1.283e+05,-6.031e+04

Brazil Trade Balance | Type: macro_line | USD mn: -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(5pt): -6.917e+04,-6.778e+04,-6.505e+04,-1.283e+05,-6.031e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Industrial production rose 0.7% MoM, beating consensus, while services PMI fell to 50.4.

- Trade surplus narrowed to $7.82bn versus $10.54bn prior; Bovespa dropped 2.22%.

- USD/BRL climbed 1.10% to 5.08 amid 25% US tariff threat on Brazilian exports.

Yesterday's Recap

Brazilian industrial output expanded 0.7% month-over-month, exceeding the 0.4% consensus and prior 0.3% print, signaling resilient manufacturing. Services PMI contracted to 50.4 from 52.3, pointing to cooling momentum in the dominant services sector. The trade balance posted a $7.82bn surplus, missing both consensus and the prior $10.54bn level as imports held firm.

Equity markets sold off sharply, with the Bovespa falling 2.22% to 170,331 amid broad risk aversion. The real weakened, lifting USD/BRL 1.10% to 5.08 and EUR/BRL 1.15% to 5.90. Vale shares dropped 4.52% while Petrobras declined 2.83%, tracking softer iron ore and crude prices.

Short-term rates eased to 14.75%, reflecting limited immediate policy pressure.

The Day Ahead

Markets enter a data-light session with no scheduled Brazilian releases. Focus shifts to follow-through on US tariff proposals and Lula administration responses seeking alternative trade partners. Investors will monitor capital flow data and any BCB speeches for signals on Selic persistence at 14.75%.

Commodity exporters face continued scrutiny as iron ore and oil prices remain volatile. Local fixed-income markets may see limited movement absent fresh inflation prints or fiscal updates.

Other Economic Notes

Persistent capital outflows to US equities reflect concerns over Brazil’s fiscal trajectory, inflation path, and 2026 elections. Tourism employment reached record highs, providing a modest offset to manufacturing softness. Lithium reserves remain largely undeveloped, limiting near-term export diversification despite global demand.

Policymakers continue to emphasize new commercial ties to cushion potential tariff damage. Real dynamics stay supported by high nominal rates but face downside risks from external demand shocks.

Global Macro News

The Trump administration’s proposed 25% tariffs on Brazilian goods, citing unfair trade practices, introduce direct downside risks to exports of soybeans, iron ore, and oil. <i>↓ p.2</i>