Brazil Macro Daily(Beta Mode)

IPCA Data Tests Selic Path as Bovespa Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 169,813.00 | +0.68% |

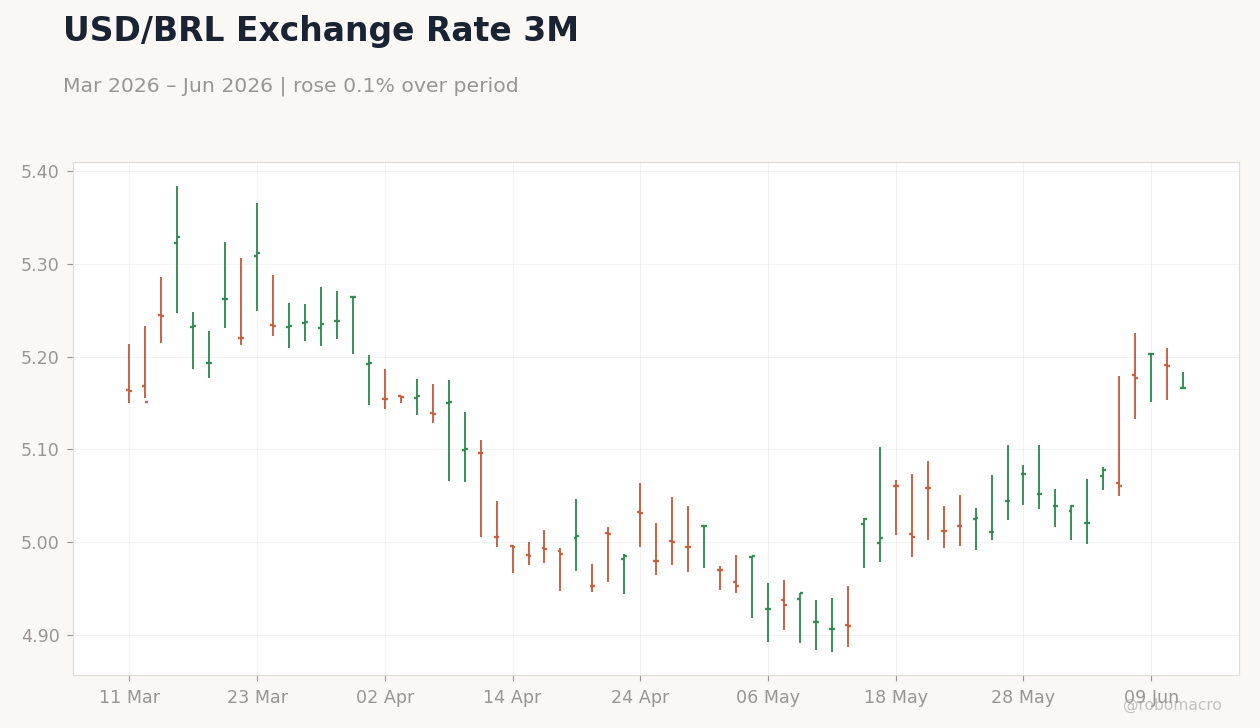

| USD/BRL | 5.17 | -0.46% |

| EUR/BRL | 5.96 | -0.30% |

| Vale | 14.95 | -1.29% |

| Petrobras | 17.90 | +0.45% |

| WTI Crude | 89.07 | -1.07% |

| Gold | 4,111.80 | +0.09% |

| Bitcoin | 62,841.17 | +2.27% |

| Brazil Short-term Rate | - | - |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/BRL Exchange Rate 3M | Type: market_hloc | USD/BRL: 5.166 (2026-06-11) | Range: 4.906–5.329 | Trend(6pt): 5.162,5.155,5.031,5.06,5.203,5.166

USD/BRL Exchange Rate 3M | Type: market_hloc | USD/BRL: 5.166 (2026-06-11) | Range: 4.906–5.329 | Trend(6pt): 5.162,5.155,5.031,5.06,5.203,5.166

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-12) | |||

| Inflation Rate Month-over-Month | 0.67 | 0.51 | 04:00 |

| Inflation Rate Year-over-Year | 4.39 | 4.65 | 04:00 |

| Business Confidence Index | 47.20 | - | 05:40 |

- May IPCA data due June 12 with MoM consensus at 0.51% and YoY at 4.65%, testing the 14.75% Selic path.

- Bovespa rose 0.68% to 169,813 while USD/BRL fell 0.46% to 5.17 on commodity and carry inflows.

- BTG flagged higher inflation risks and called for a Selic pause, aligning with Verde's zero BRL stance.

Yesterday's Recap

Markets closed higher on June 10 with no major data releases. Bovespa gained 0.68% to 169,813, led by Petrobras which rose 0.45% to 17.90. USD/BRL dropped 0.46% to 5.17 and EUR/BRL eased 0.30% to 5.96, reflecting softer external yields and local carry demand.

Vale fell 1.29% to 14.95 amid softer iron-ore margins in China. WTI Crude declined 1.07% to 89.07 while Bitcoin added 2.27% to 62,841.17. Lula's sovereignty remarks and Durigan's Pix defense added little market volatility.

Fiscal royalty inflows and stable commodity exports kept the real supported ahead of inflation prints.

The Day Ahead

Markets focus on the June 12 IPCA release at 04:00 ET. MoM inflation is expected at 0.51% versus 0.67% prior while YoY should reach 4.65% from 4.39%. Business Confidence Index follows at 05:40 ET with no consensus provided.

A cooler-than-expected print would ease pressure on the 14.75% Selic and support further BRL strength. No COPOM speakers are scheduled. Traders will also monitor US PPI and ECB decisions for global rate cues that could affect carry flows into Brazil.

Other Economic Notes

BTG Pactual revised inflation higher and argued the Selic easing cycle should pause after the next 25 bp cut. Verde Asset Management exited its BRL position citing an American policy ghost. Lula compared recent Mexican protests to Brazil's 2013 demonstrations during a sustainable development council meeting.

Durigan reaffirmed that Brazil will not bow to external pressure while defending Pix sovereignty. Iron-ore export volumes to China rose 8% y/y in May but steel margin weakness may limit further gains.

Global Macro News

US PPI and CPI prints highlighted persistent price pressures that could delay Fed cuts and support higher-for-longer global yields. ECB rate decision and services data in Brazil add to Thursday's calendar. Iran's stalled nuclear talks prompted Trump warnings of consequences that lifted oil volatility.

<i>↓ p.2</i>