Brazil Macro Daily(Beta Mode)

BRL Rises Ahead of Brazil Inflation Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,497.00 | +1.71% |

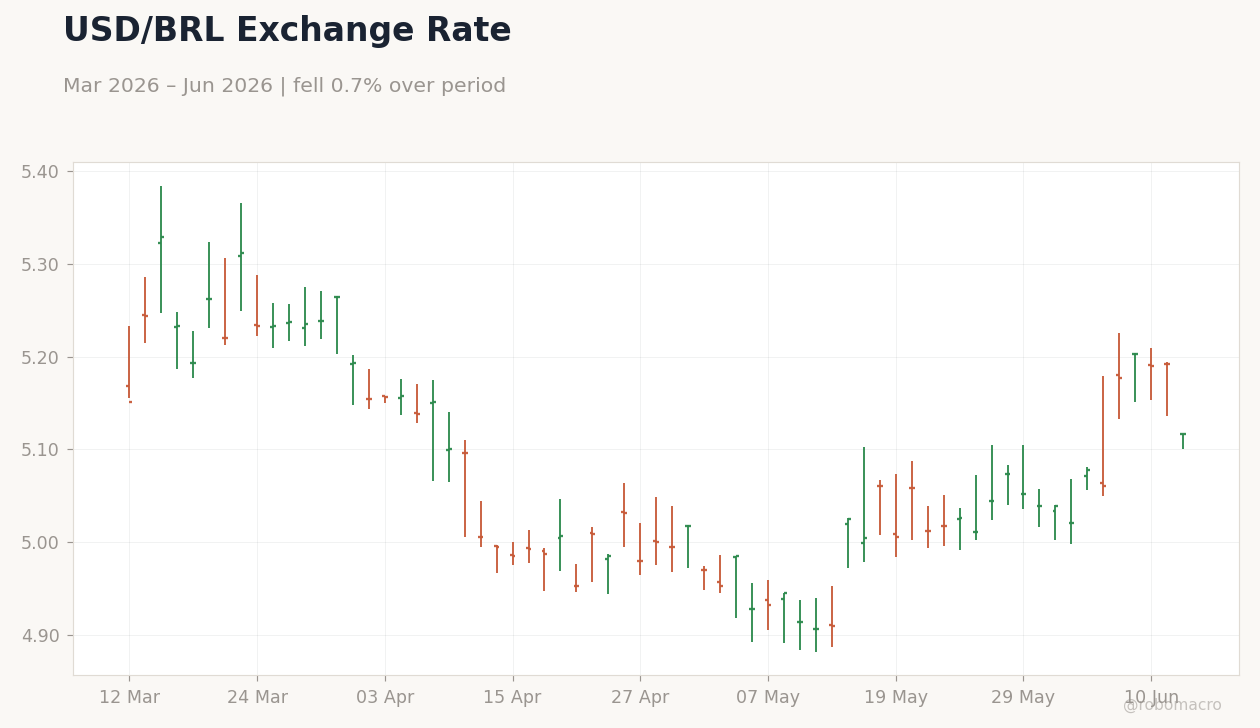

| USD/BRL | 5.12 | -1.45% |

| EUR/BRL | 5.92 | -1.04% |

| Vale | 15.36 | +2.88% |

| Petrobras | 18.24 | +0.72% |

| WTI Crude | 83.91 | -4.33% |

| Gold | 4,245.80 | +3.80% |

| Bitcoin | 63,410.65 | -0.24% |

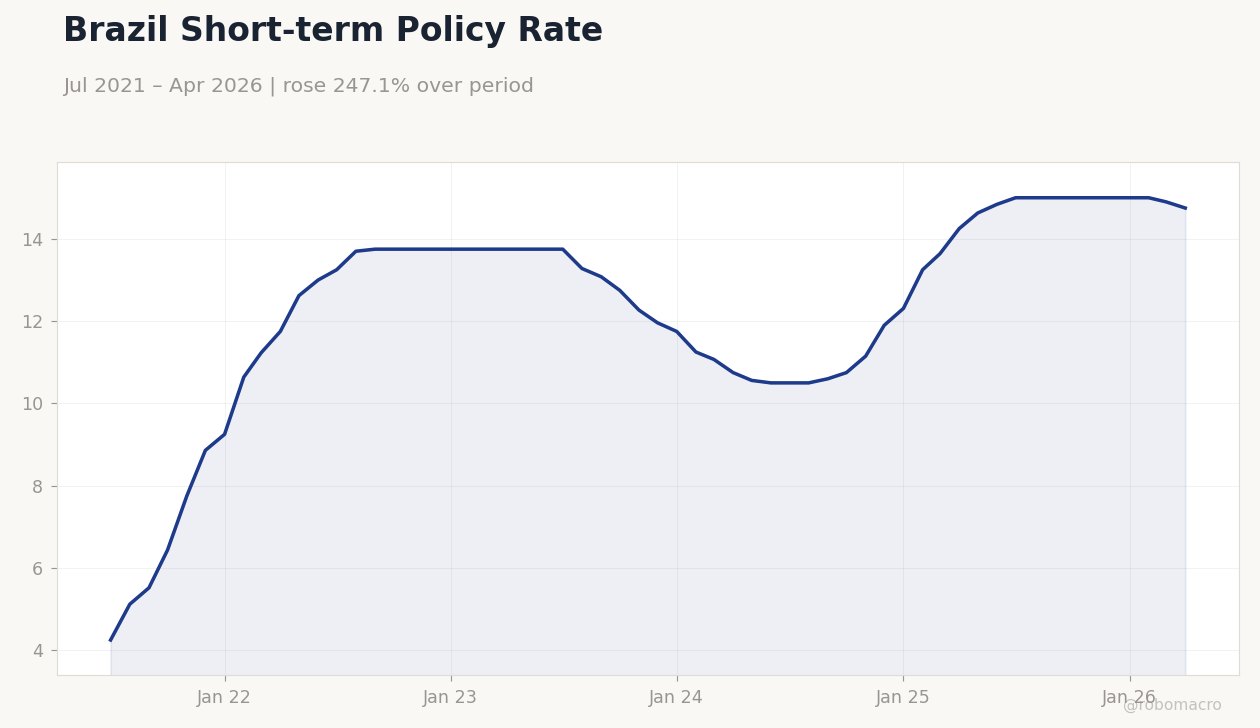

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Short-term Policy Rate | Type: macro_line | %: 14.75 (2026-04-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.75

Brazil Short-term Policy Rate | Type: macro_line | %: 14.75 (2026-04-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.67 | 0.53 | 04:00 |

| Inflation Rate Year-over-Year | 4.39 | 4.66 | 04:00 |

| Business Confidence Index | 47.20 | - | 05:40 |

- Bovespa climbs 1.71% to 171,497 on commodity gains

- USD/BRL drops 1.45% to 5.12 as risk appetite improves

- Selic steady at 14.75% while inflation data approach

Yesterday's Recap

Brazilian markets posted solid gains on June 11 with no major data releases. Bovespa advanced 1.71% to close at 171,497, driven by Vale shares rising 2.88% and Petrobras adding 0.72%. The real strengthened notably, sending USD/BRL down 1.45% to 5.12 and EUR/BRL lower by 1.04% to 5.92.

Short-term Brazilian rates eased 1.01% to 14.75%, reflecting reduced inflation concerns. Gold surged 3.80% to 4,245.80 while WTI crude fell 4.33% to 83.91, pressuring energy names modestly. Bitcoin slipped 0.24% to 63,410.65 amid mixed global flows.

Equity and currency moves aligned with firmer iron-ore demand and broader EM inflows.

The Day Ahead

Markets focus on three medium-impact releases scheduled for June 12. Inflation Rate MoM is expected at 0.53% versus 0.67% prior, while the YoY reading is forecast to rise to 4.66% from 4.39%. Business Confidence Index follows at 05:40 ET with no consensus provided after printing 47.2 last month.

A cooler monthly inflation outcome could reinforce expectations for eventual policy easing despite the elevated Selic level. Stronger-than-expected prints risk lifting the real further and pressuring DI futures. No BCB speeches or minutes are slated.

Other Economic Notes

Brazilian credit continues to draw foreign interest according to Ibiuna, supporting local fixed-income flows. Pix expansion into automatic payments is reshaping retail finance and reducing reliance on traditional credit cards. Fiscal targets remain anchored at a 0.5% of GDP primary deficit for 2026, limiting debt-sustainability concerns.

Commodity export resilience, especially iron ore and soy, underpins the trade surplus and BRL valuation. Deforestation reductions provide diplomatic leverage against potential tariff threats.

Global Macro News

Global commodity swings directly influence Brazil’s terms of trade and currency. Gold’s 3.80% jump highlights safe-haven demand that often supports EM assets indirectly. Oil’s 4.33% decline weighs on Petrobras earnings prospects and fiscal revenues.

<i>↓ p.2</i>