Brazil Macro Daily(Beta Mode)

World Bank Cuts Brazil Growth Outlook

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,133.00 | -0.21% |

| USD/BRL | 5.06 | -0.98% |

| EUR/BRL | 5.88 | -0.65% |

| Vale | 15.71 | +2.28% |

| Petrobras | 18.38 | +0.77% |

| WTI Crude | 80.50 | -5.16% |

| Gold | 4,356.80 | +3.36% |

| Bitcoin | 65,639.35 | +1.89% |

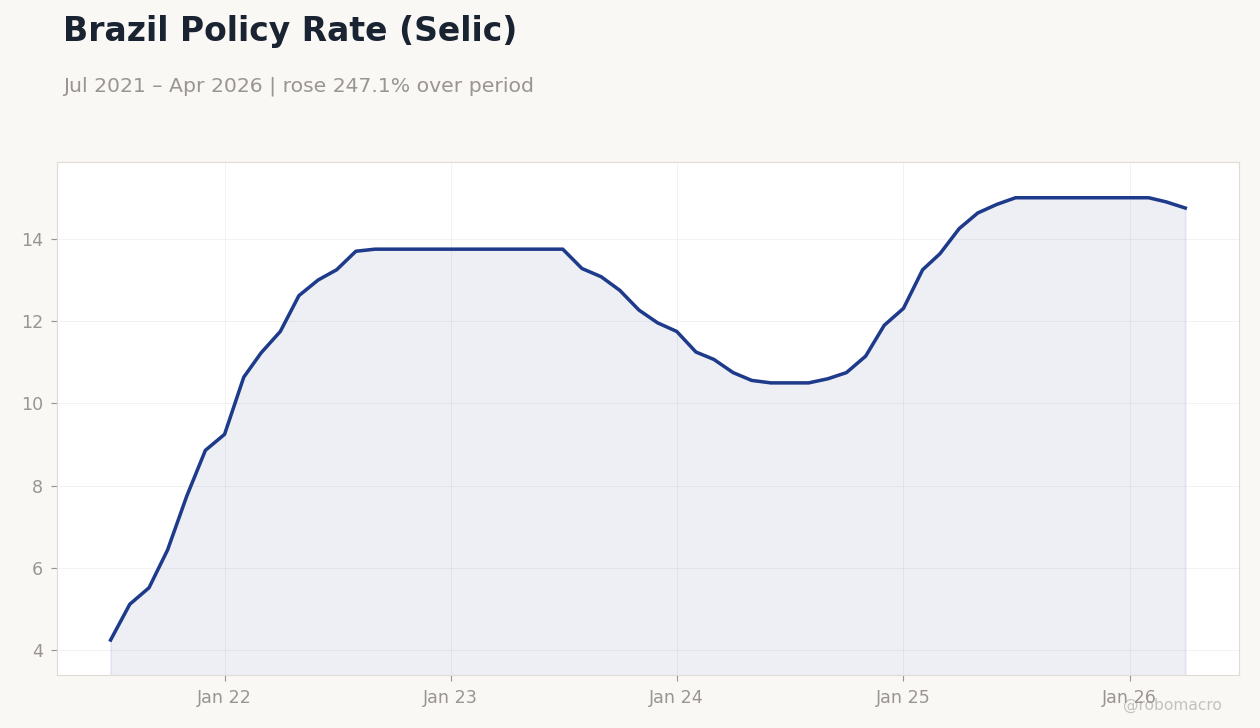

| Brazil Short-term Rate | 14.75% | -1.01% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Policy Rate (Selic) | Type: macro_line | %: 14.75 (2026-04-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.75

Brazil Policy Rate (Selic) | Type: macro_line | %: 14.75 (2026-04-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-16) | |||

| Retail Sales Month-over-Month | 0.50 | - | 04:00 |

| Wednesday (2026-06-17) | |||

| Central Bank Interest Rate Decision | 14.50 | - | 13:30 |

- World Bank lowered 2026-2027 GDP forecasts amid fiscal pressures.

- Bovespa fell 0.21% while USD/BRL dropped 0.98% to 5.06.

- Copom set to decide on Selic at 14.75% on June 17.

Yesterday's Recap

Markets digested the absence of fresh data releases on June 14. Bovespa closed 0.21% lower at 171,133 while USD/BRL fell 0.98% to 5.06. Vale rose 2.28% on firmer iron-ore prices and Petrobras gained 0.77%.

Brazil’s short-term rate stood at 14.75%. WTI crude dropped 5.16% to 80.50, weighing on energy exporters. Gold climbed 3.36% to 4,356.80, offering a safe-haven bid for local assets.

Bitcoin added 1.89%, reflecting broader risk-on flows into emerging-market currencies.

The Day Ahead

Retail sales month-over-month for May print at 04:00 ET on June 16, with the prior reading at 0.5%. Markets will watch for signs of consumer resilience ahead of the Copom meeting. The central bank interest-rate decision follows at 13:30 ET on June 17, with the Selic last recorded at 14.75%.

Analysts expect either a hold or a pause given sticky inflation. No other major Brazilian releases are scheduled before the policy announcement. Focus will remain on forward guidance and any shift in the inflation-targeting framework.

Other Economic Notes

The World Bank trimmed its 2026 and 2027 growth projections for Brazil, citing weaker fiscal momentum. FGV Ibre urged overhaul of the oil-revenue fiscal framework to stabilize public accounts. President Lula will meet President Trump to discuss economy and security, potentially shaping trade and investment flows.

BTG lowered its equity recommendation on Brazil, joining other global banks in dialing back exposure. These moves highlight persistent concerns over fiscal sustainability and commodity dependence.

Global Macro News

Lower WTI prices reduce Brazil’s oil-export receipts and fiscal receipts from Petrobras. Gold’s advance to 4,356.80 supports BRL as a commodity-linked currency. Bitcoin’s 1.89% gain signals renewed risk appetite that can lift Bovespa flows.

The Lula-Trump meeting may influence bilateral trade terms and capital-market sentiment. Broader Latin-American blue-economy initiatives offer long-term investment channels but limited near-term price impact. <i>↓ p.2</i>