Brazil Macro Daily(Beta Mode)

Copom Set for 25bp Selic Cut

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,133.00 | -0.21% |

| USD/BRL | 5.07 | +0.13% |

| EUR/BRL | 5.88 | +0.18% |

| Vale | 15.71 | +2.28% |

| Petrobras | 18.38 | +0.77% |

| WTI Crude | 77.30 | -4.27% |

| Gold | 4,361.30 | +0.77% |

| Bitcoin | 66,428.72 | +0.21% |

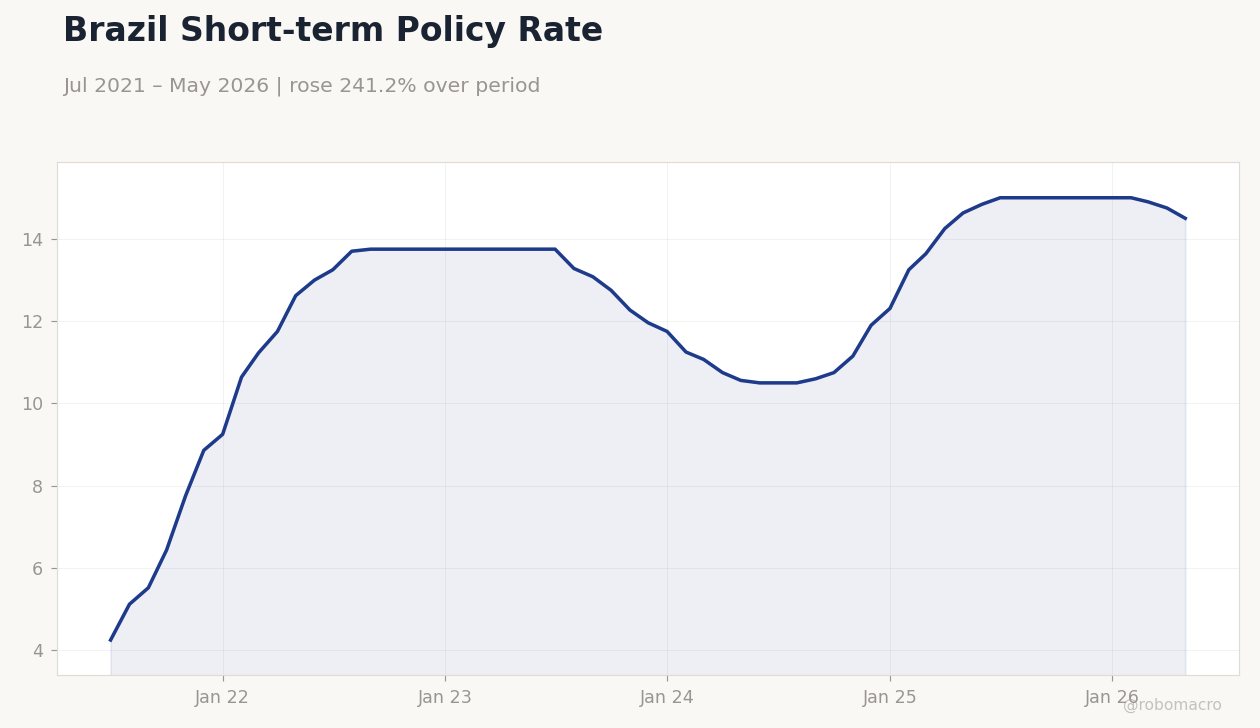

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47.20 | - | 46.70 |

Brazil Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Retail Sales Month-over-Month | 0.50 | -0.70 | 04:00 |

| Wednesday (2026-06-17) | |||

| Central Bank Interest Rate Decision | 14.50 | 14.25 | 13:30 |

- Business confidence slipped to 46.7 in May, extending the contractionary streak and signaling softer domestic demand ahead of the COPOM meeting.

- Retail sales are forecast to contract 0.7% m/m today, following a 0.5% gain in April, which could reinforce the case for a measured easing step.

- Markets price a 25bp Selic reduction to 14.25% tomorrow, with the committee likely to adopt a hawkish tone citing persistent 12-month inflation above target.

Yesterday's Recap

Brazil’s Business Confidence Index fell to 46.7 from 47.2, marking the third consecutive reading below 50 and highlighting weakening sentiment in manufacturing and services. Bovespa closed 0.21% lower at 171,133 while USD/BRL rose 0.13% to 5.07 amid thin volumes and positioning ahead of the COPOM decision. Vale gained 2.28% on firmer iron-ore prices while Petrobras advanced 0.77% despite a 4.27% drop in WTI crude to 77.30.

The short-term rate remained at 14.50% with the curve reflecting expectations of gradual easing. No BCB officials spoke publicly, leaving forward guidance unchanged from the May minutes. Equity and FX moves stayed contained as investors awaited today’s retail sales print and tomorrow’s policy announcement.

The Day Ahead

Retail sales month-over-month for May are due at 04:00 ET and will provide the last major data point before the COPOM decision. Consensus calls for a 0.7% contraction after April’s 0.5% increase, with downside surprises likely to support a 25bp cut. The COPOM meeting begins at 13:30 ET tomorrow and markets assign roughly 80% probability to a reduction from 14.50% to 14.25%.

No other high-impact Brazilian releases are scheduled for the remainder of the week. Attention will center on whether the statement signals a pause after this move or keeps the door open for further easing later in the year.

Other Economic Notes

Twelve-month inflation remains above the target band even as services prices show signs of cooling, creating a narrow window for the central bank to ease without losing credibility. Fiscal data released last week showed a primary deficit of 0.4% of GDP in May, remaining inside the government’s tolerance range but leaving little room for additional spending stimulus. Commodity export revenues continue to benefit from solid Chinese iron-ore demand, partially offsetting softer oil prices.

Nubank-related messaging glitches prompted a swift central-bank clarification but did not alter liquidity conditions or deposit flows.