Brazil Macro Daily(Beta Mode)

Retail Sales Slump Precedes BCB Rate Decision

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 169,649.00 | -0.45% |

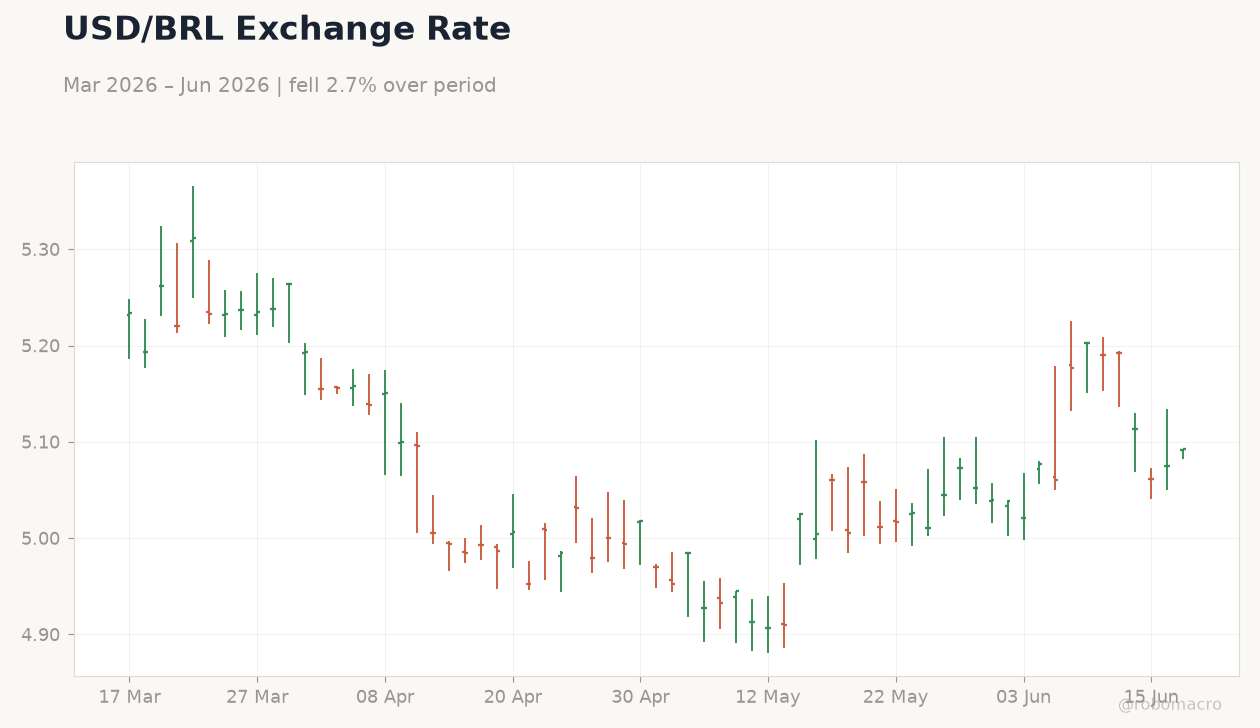

| USD/BRL | 5.09 | +0.34% |

| EUR/BRL | 5.90 | +0.37% |

| Vale | 15.98 | -0.12% |

| Petrobras | 17.05 | -1.67% |

| WTI Crude | 75.69 | -0.47% |

| Gold | 4,348.30 | +0.40% |

| Bitcoin | 64,700.55 | -1.37% |

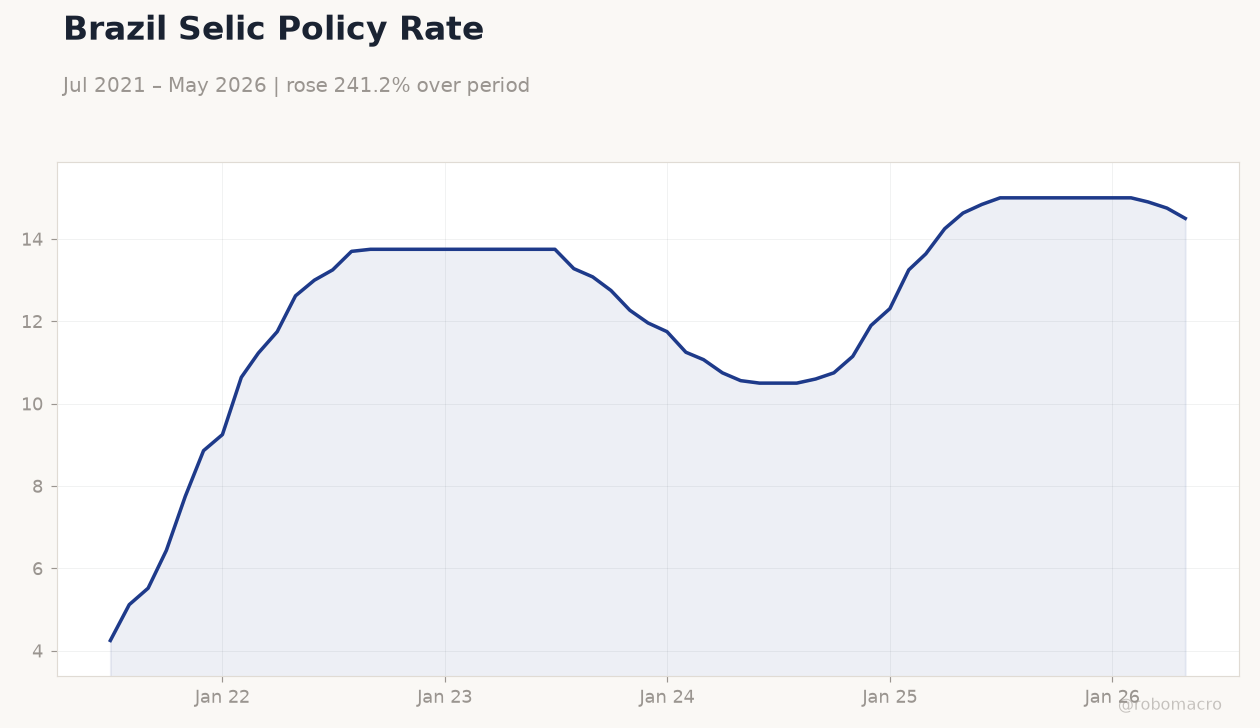

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47.20 | - | 46.70 |

| Retail Sales Month-over-Month | 0.50 | -0.60 | -1.50 |

Brazil Selic Policy Rate | Type: macro_line | Policy Rate (%): 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Selic Policy Rate | Type: macro_line | Policy Rate (%): 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 14.50 | 14.25 | 13:30 |

- Brazil retail sales contracted 1.5% MoM in May, well below consensus, signaling softening domestic demand ahead of the COPOM meeting.

- BCB is expected to cut the Selic rate by 25 bp to 14.25% today, extending the easing cycle amid contained inflation pressures.

- Bovespa fell 0.45% while USD/BRL rose 0.34% to 5.09 as markets priced in the policy shift and weaker activity data.

Yesterday's Recap

Brazil’s Business Confidence Index declined to 46.7 in June from 47.2 prior, reflecting subdued business sentiment. Retail sales posted a sharp -1.5% MoM contraction against expectations of -0.6%, confirming a clear loss of momentum in consumer spending. Equity markets closed lower with Bovespa dropping 0.45% to 169,649 led by a 1.67% decline in Petrobras shares.

The BRL weakened modestly, lifting USD/BRL to 5.09 and EUR/BRL to 5.90. Short-term Brazilian rates eased to 14.50% as markets positioned for today’s policy announcement. Commodity prices offered little support, with WTI crude falling 0.47% and iron-ore linked Vale shares slipping 0.12%.

Overall risk appetite remained cautious ahead of the COPOM decision.

The Day Ahead

Markets will focus squarely on the BCB’s interest-rate decision scheduled for 13:30 ET. Consensus expects a 25 bp cut that would lower the Selic rate to 14.25%. No other high-impact Brazilian data releases are calendared for the session.

Attention will center on any revisions to forward guidance and the committee’s assessment of the recent inflation trajectory. Global commodity moves and external risk sentiment may also influence BRL and equity flows during the afternoon.

Other Economic Notes

Fitch’s affirmation of Brazil’s BB sovereign rating underscores the resilience of the diversified economy despite fiscal pressures. Government primary deficit data released earlier this month came in narrower than expected, supporting debt-sustainability narratives. Iron-ore export volumes to China continued to expand, providing a modest offset to weaker domestic indicators.

Discussions at the G7 on pandemic preparedness carry limited immediate market implications for Brazil but highlight ongoing multilateral engagement by the Lula administration.

Global Macro News

Softer Chinese demand signals weighed on global oil prices, indirectly pressuring Brazilian energy exporters. <i>↓ p.2</i>