Brazil Macro Daily(Beta Mode)

Copom Cuts Selic to 14.25% on Weak Sales

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 168,454.00 | -0.70% |

| USD/BRL | 5.07 | -0.64% |

| EUR/BRL | 5.84 | -1.32% |

| Vale | 15.53 | -2.82% |

| Petrobras | 16.79 | -1.52% |

| WTI Crude | 73.97 | -3.67% |

| Gold | 4,295.40 | -1.46% |

| Bitcoin | 64,291.87 | -2.00% |

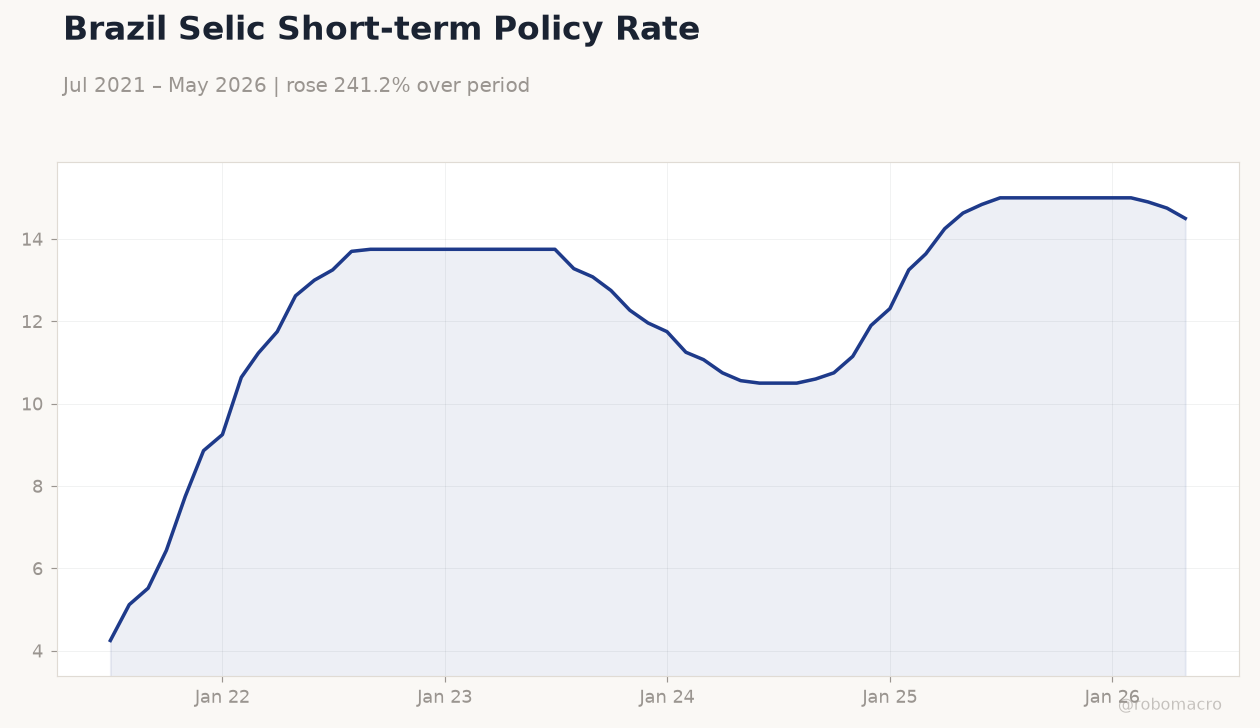

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

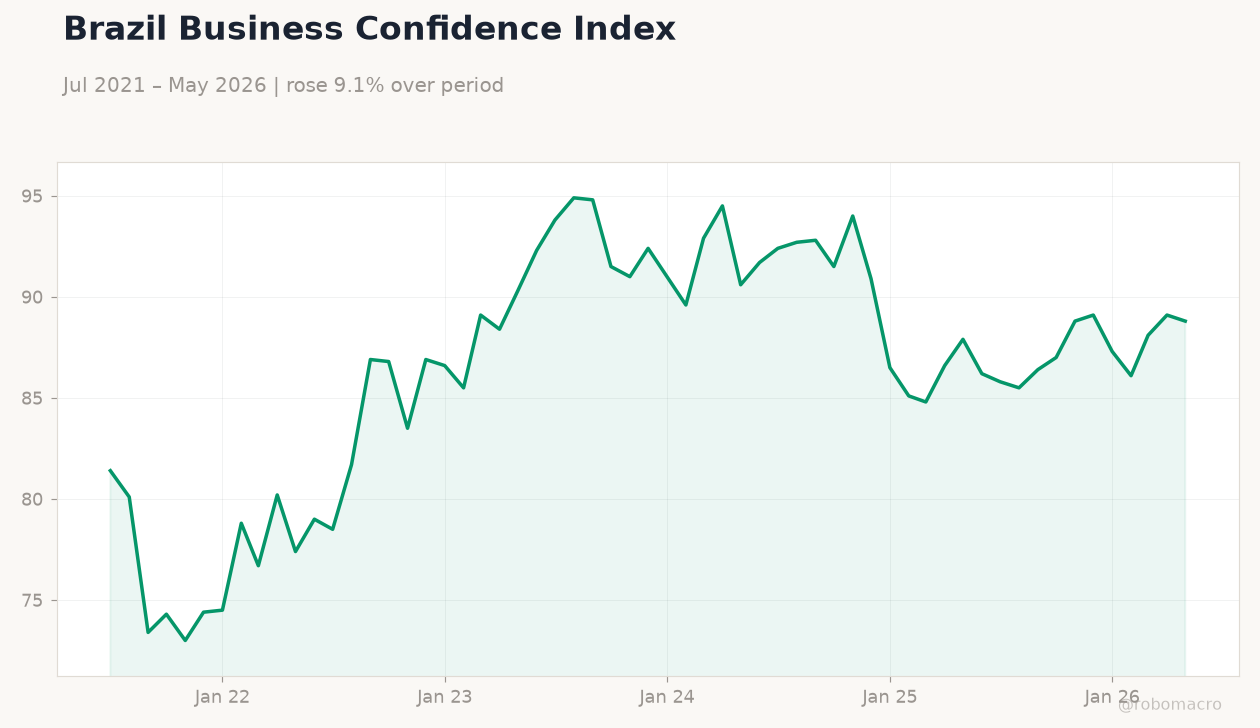

| Business Confidence Index | 47.20 | - | 46.70 |

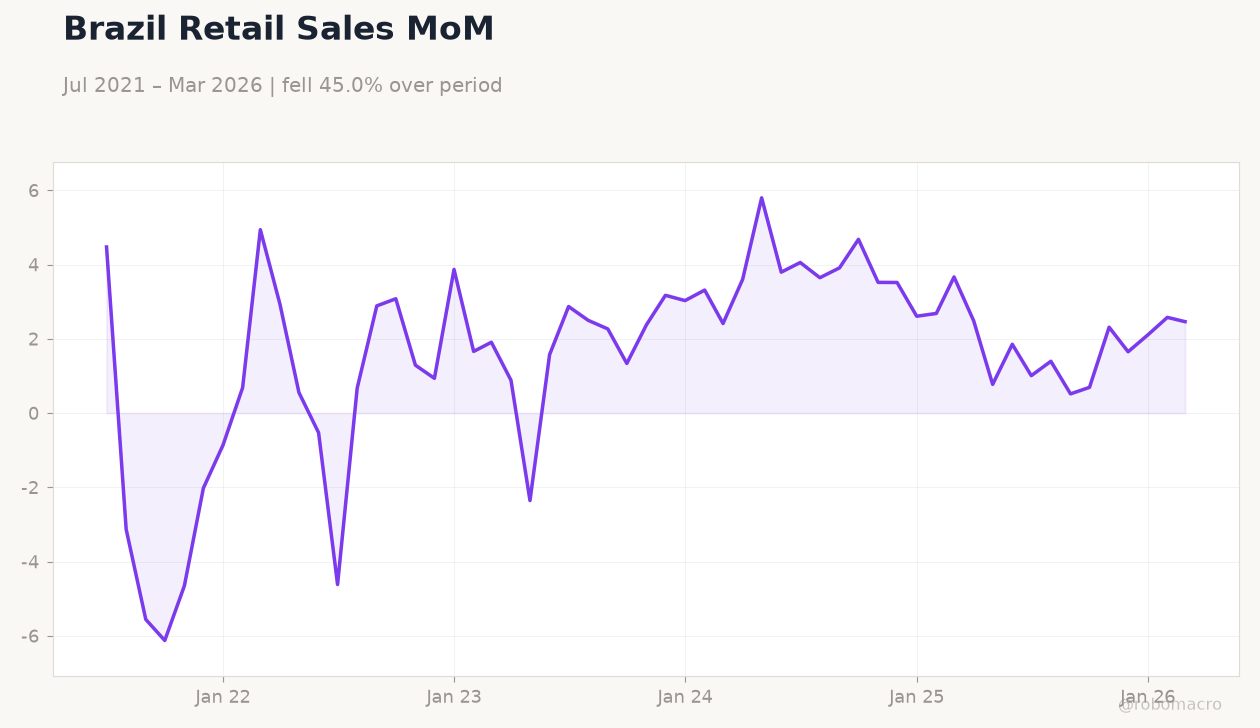

| Retail Sales Month-over-Month | 0.50 | -0.60 | -1.50 |

| Central Bank Interest Rate Decision | 14.50 | 14.25 | - |

Brazil Selic Short-term Policy Rate | Type: macro_line | Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Selic Short-term Policy Rate | Type: macro_line | Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Copom delivered a 25bp Selic cut to 14.25%, citing persistent inflation pressures and a tougher forward guidance.

- Brazil retail sales fell 1.5% MoM, missing consensus by a wide margin and signaling softening domestic demand.

- Bovespa declined 0.70% while USD/BRL eased 0.64% as markets digested the rate decision and political noise.

Yesterday's Recap

Brazil’s Business Confidence Index slipped to 46.7 in June from 47.2, extending the weak sentiment streak. Retail sales contracted 1.5% MoM versus an expected 0.6% decline, confirming a sharper-than-forecast pullback in consumer spending. Copom lowered the Selic rate by 25bp to 14.25%, matching the pre-meeting consensus but adopting a more hawkish tone on inflation.

The Bovespa closed at 168,454, down 0.70%, with Vale falling 2.82% on softer iron-ore prices. USD/BRL traded at 5.07, strengthening 0.64% as the rate cut was already priced in. Short-term Brazilian rates moved in line with the new policy rate.

Political headlines around Lula’s rebuke of Trump added volatility but did not alter the market’s focus on the monetary decision.

The Day Ahead

No major Brazilian data releases are scheduled for 18–19 June, leaving markets to react to global flows and follow-up commentary from Copom members. Focus will remain on inflation prints due next week and any fiscal updates from Brasília. Equity and FX desks will monitor iron-ore and oil prices given their weight in the trade balance.

Analysts expect limited volatility absent surprises from the G7 fallout or commodity swings. Positioning for the next Copom meeting will likely dominate local rates trading.

Other Economic Notes

The combination of lower business confidence and weak retail sales raises downside risks to second-quarter GDP. Fiscal sustainability concerns persist as debt-service costs remain elevated despite the Selic reduction. Commodity exporters continue to benefit from still-supportive global prices, yet softening domestic demand may weigh on imports and the current-account balance.

Credit managers are selectively adding corporate debt, viewing the post-cut environment as an opportunity in utilities and consumer-facing sectors.

Global Macro News

Lula’s public warning to Trump to stay out of Brazilian elections introduced political noise that briefly pressured risk assets. <i>↓ p.2</i>