Brazil Macro Daily(Beta Mode)

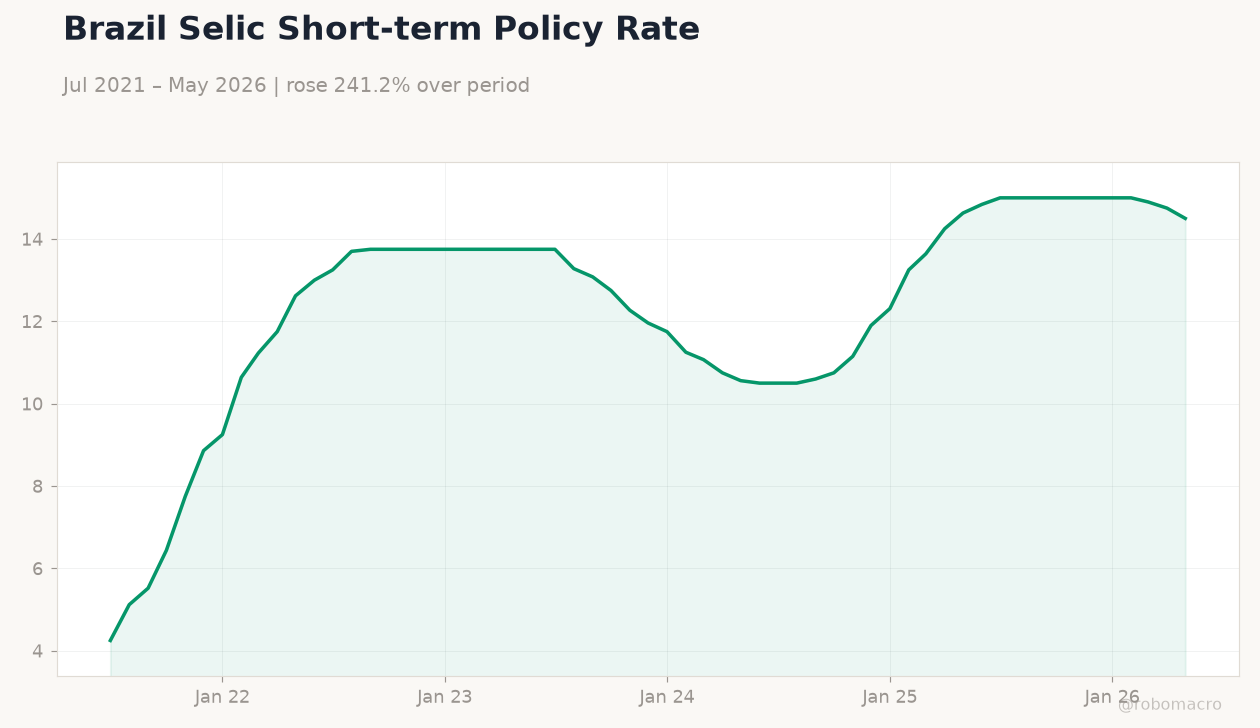

Selic Cut to 14.25% Amid Retail Sales Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 168,278.00 | -0.10% |

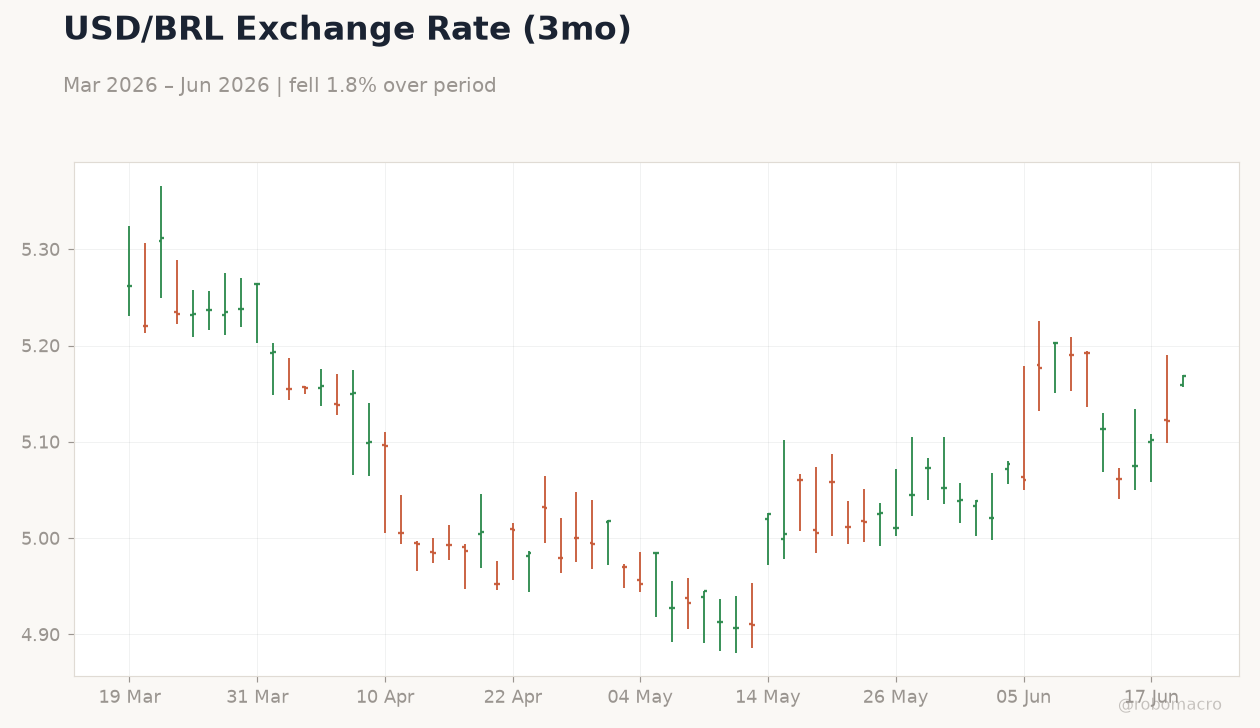

| USD/BRL | 5.17 | +0.90% |

| EUR/BRL | 5.92 | +0.54% |

| Vale | 15.43 | -0.68% |

| Petrobras | 16.49 | -1.82% |

| WTI Crude | 75.89 | -0.93% |

| Gold | 4,172.50 | -1.22% |

| Bitcoin | 62,393.77 | -0.80% |

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

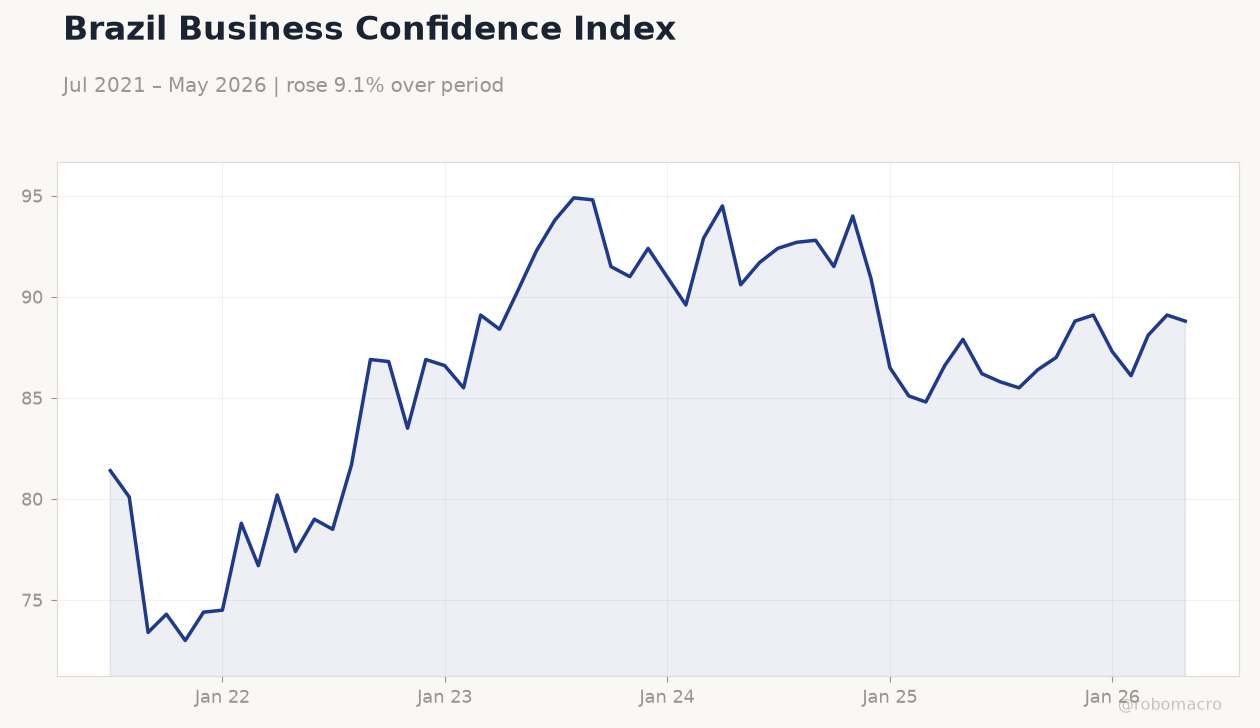

| Business Confidence Index | 47.20 | - | 46.70 |

| Retail Sales Month-over-Month | 0.50 | -0.60 | -1.50 |

| Central Bank Interest Rate Decision | 14.50 | 14.25 | 14.25 |

Brazil Business Confidence Index | Type: macro_line | Business Confidence: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Brazil Business Confidence Index | Type: macro_line | Business Confidence: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BCB delivers 25bp Selic cut to 14.25% amid cooling activity

- Retail sales plunge 1.5% MoM, business confidence slips to 46.7

- Bovespa falls 0.1%, USD/BRL jumps 0.9% to 5.17

Yesterday's Recap

Brazil’s central bank lowered the Selic rate by 25 basis points to 14.25%, matching consensus after the prior 14.50% level. Retail sales contracted 1.5% month-over-month, missing forecasts and reversing the prior 0.5% gain. Business confidence declined to 46.7 from 47.2, signaling further softening in private-sector sentiment.

Bovespa closed 0.1% lower at 168,278 while USD/BRL rose 0.9% to 5.17. Vale fell 0.68% and Petrobras dropped 1.82% as iron-ore and oil prices eased. The moves reflected both the policy easing and weaker domestic demand data.

The Day Ahead

Markets enter a data-light period with no scheduled Brazilian releases today or tomorrow. Focus will remain on incoming inflation prints and fiscal updates later in the month. Traders will monitor any follow-up comments from Copom members on the pace of further easing.

Global commodity prices and USD direction will continue to drive BRL flows. Local equity and rates desks are expected to position ahead of month-end flows.

Other Economic Notes

Brazil slipped to 65th in a global competitiveness ranking of 70 countries, highlighting structural bottlenecks. FGV estimates the economy expanded just 0.1% in April despite elevated rates and oil-price pressure. M&A activity stayed robust, with Brazil accounting for nearly half of Latin American deals in 2025.

IPCA-linked NTN-B yields hit fresh highs near 8.5% above inflation, reflecting persistent real-rate demand. These trends underscore that growth alone has not resolved competitiveness or fiscal challenges.

Global Macro News

China outlined 20 digital-economy projects for potential investment in Brazil, offering a counterweight to slower domestic demand. A fractured global trading system is raising costs for Brazilian exporters through higher barriers and supply-chain fragmentation. Lula pressed EU leaders to ease tariffs on Brazilian meat and steel during meetings in Brussels.

Studies showed the 2026 World Cup will have only marginal effects on Brazilian inflation. Mexico and other peers are advancing sustainable tourism corridors that could compete with Brazilian coastal offerings. Overall external demand remains sensitive to commodity price swings and U.S.

<i>↓ p.2</i>