Brazil Macro Daily(Beta Mode)

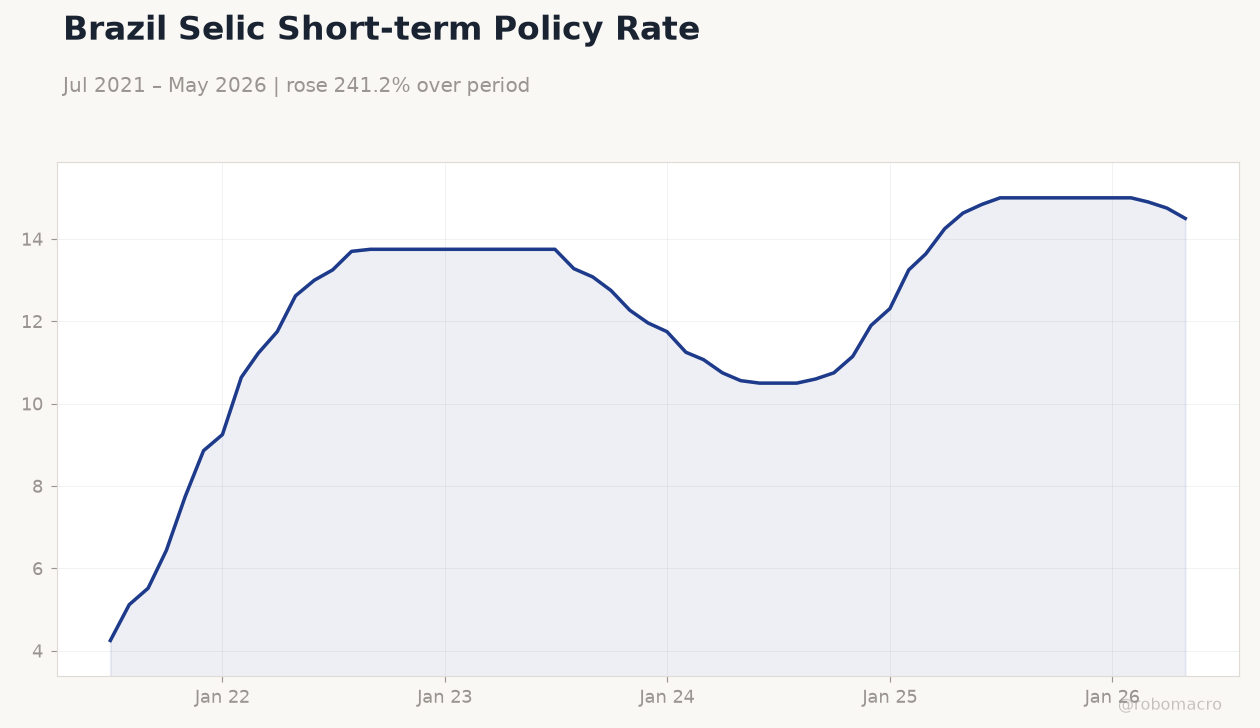

Selic Steady at 14.50% Ahead of Copom Minutes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 168,576.00 | +0.18% |

| USD/BRL | 5.14 | -0.77% |

| EUR/BRL | 5.89 | -0.74% |

| Vale | 15.43 | -0.68% |

| Petrobras | 16.49 | -1.82% |

| WTI Crude | 75.37 | -1.61% |

| Gold | 4,212.20 | -0.28% |

| Bitcoin | 64,098.67 | +1.36% |

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Selic Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Selic Short-term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-23) | |||

| BCB Copom Meeting Minutes | - | - | 03:00 |

| Friday (2026-06-26) | |||

| Headline Unemployment Rate | 5.80 | - | 04:00 |

- BCB minutes release tomorrow keeps markets focused on Selic path at 14.50%

- Bovespa rises 0.18% while USD/BRL drops 0.77% to 5.14 on commodity flows

- Citi flags higher global rates lifting Brazil fiscal costs amid competitiveness slide

Yesterday's Recap

Bovespa closed at 168,576, up 0.18%, as investors absorbed limited local data. USD/BRL fell 0.77% to 5.14 while EUR/BRL declined 0.74% to 5.89. Vale fell 0.68% to 15.43 and Petrobras dropped 1.82% to 16.49 amid softer WTI crude at 75.37, down 1.61%.

Brazil short-term rate held at 14.50%, down 1.69% on the day. No economic releases occurred yesterday, leaving price action driven by external commodity moves and positioning ahead of the Copom minutes. Bitcoin rose 1.36% while gold slipped 0.28%.

The Day Ahead

BCB Copom Meeting Minutes at 03:00 ET tomorrow will detail the latest policy discussion around the 14.50% Selic rate. Markets will parse any signals on the timing of future easing steps. Headline Unemployment Rate prints Friday at 04:00 ET, following the prior 5.8% print.

Analysts expect the labor data to influence front-end yields and BRL volatility. No other high-impact Brazilian releases are scheduled mid-week.

Other Economic Notes

Citi highlighted that elevated global rates are increasing Brazil’s debt-servicing costs and pressuring the fiscal trajectory. Brazil fell seven places to 65th in a global competitiveness ranking, posting the worst score in cost of capital and basic education. Iron-ore and soybean export volumes remain supportive for the trade balance, yet softening Chinese steel demand raises downside risks for 2026.

Fiscal supplementary budget requests continue to weigh on sentiment toward longer-dated NTN-Bs.

Global Macro News

Higher US Treasury yields are transmitting directly into wider spreads for Brazilian external debt. The Fed’s firm tone has reduced the probability of near-term dollar weakening, keeping USD/BRL supported above 5.10. Oil price weakness weighs on Petrobras cash flow and government fuel-subsidy calculations.

Iron-ore prices remain the key swing factor for Vale and BRL strength. Emerging-market portfolio managers are increasing Brazil allocations relative to peers, citing attractive carry at the current Selic level. Global risk sentiment will dictate whether the recent BRL rally extends through the minutes release.