Brazil Macro Daily(Beta Mode)

Copom Minutes to Clarify Rate Path

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 170,370.00 | +1.06% |

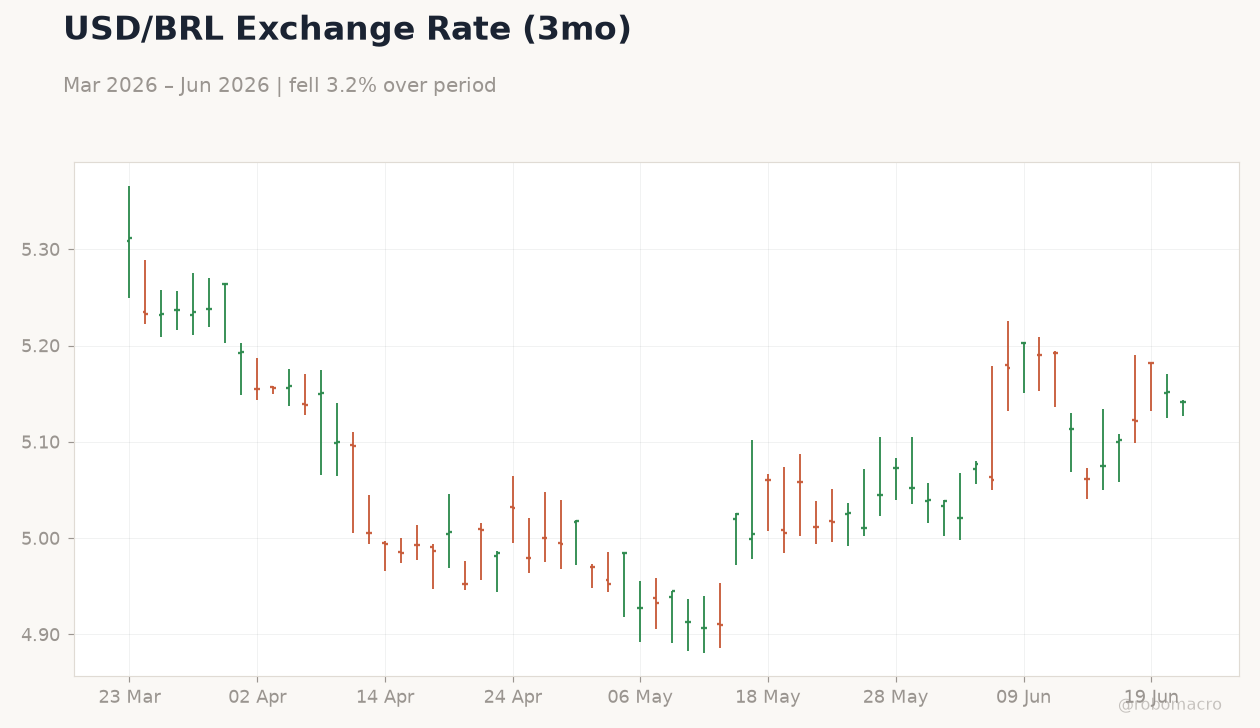

| USD/BRL | 5.14 | -0.20% |

| EUR/BRL | 5.86 | -0.54% |

| Vale | 15.43 | -0.68% |

| Petrobras | 16.49 | -1.82% |

| WTI Crude | 73.45 | -1.83% |

| Gold | 4,125.00 | -1.36% |

| Bitcoin | 62,334.51 | -2.53% |

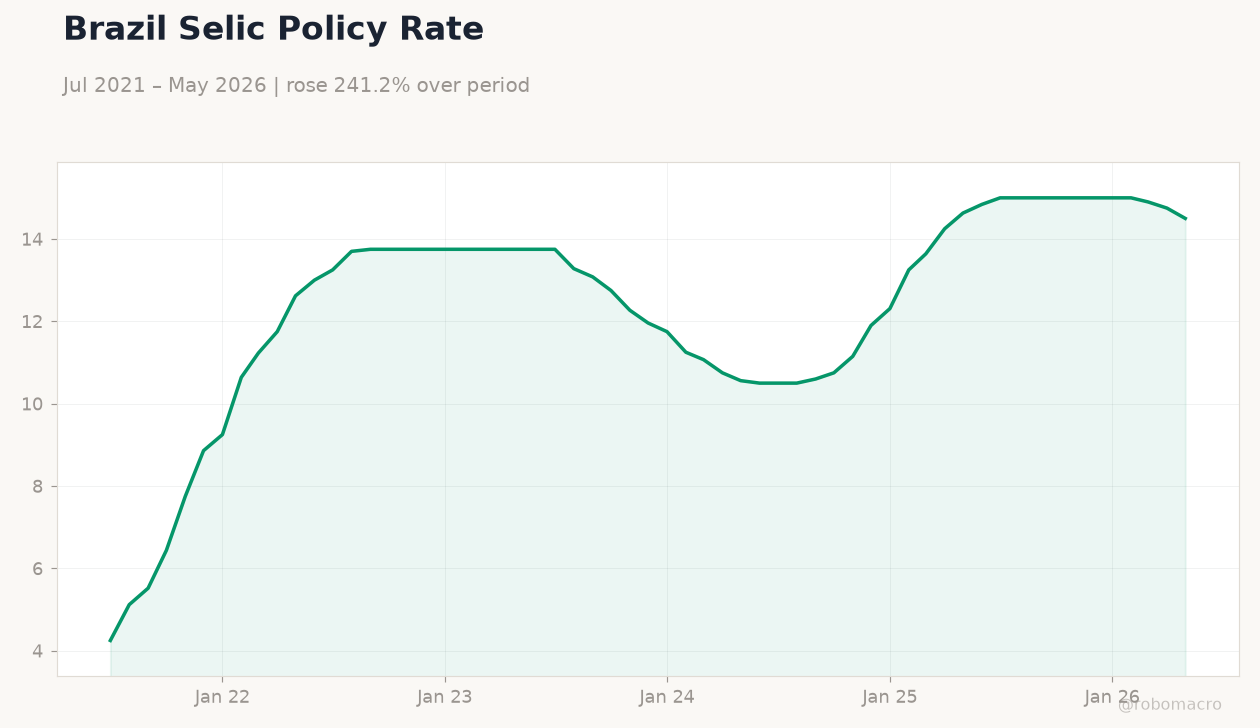

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

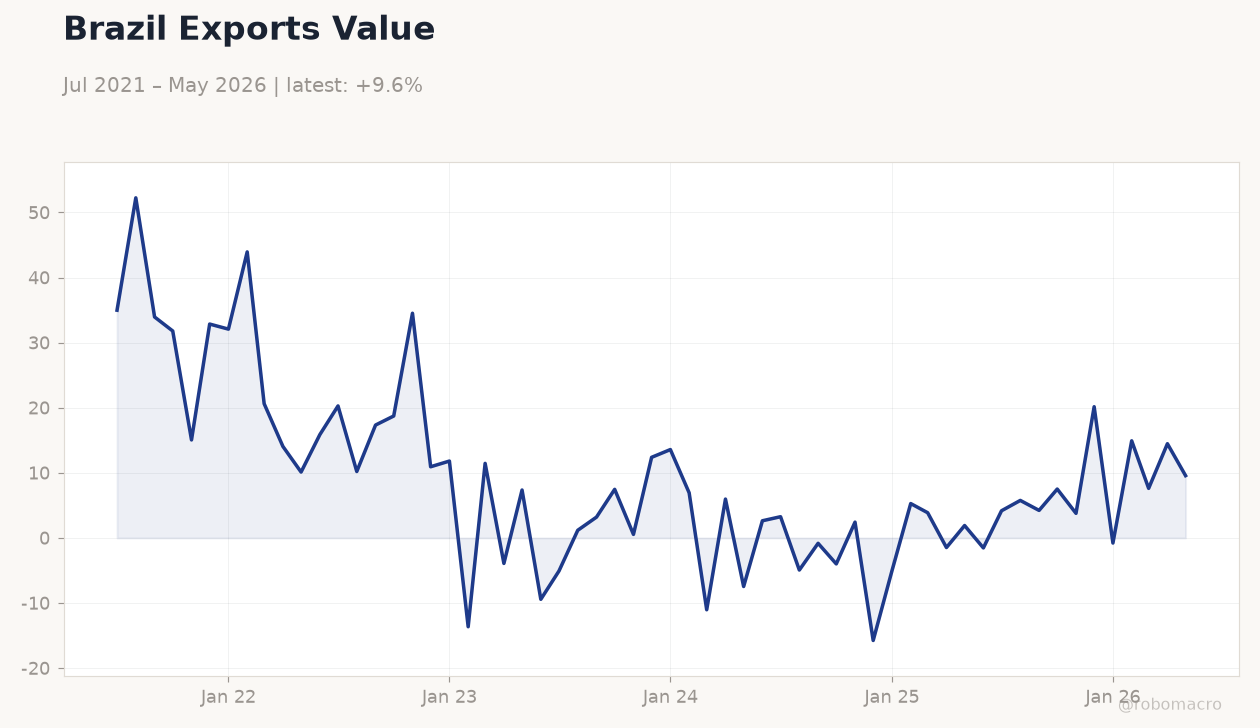

Brazil Exports Value | Type: macro_line | Exports (USD mn): 9.567 (2026-05-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.614,9.567

Brazil Exports Value | Type: macro_line | Exports (USD mn): 9.567 (2026-05-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.614,9.567

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | 03:00 |

| Friday (2026-06-26) | |||

| Headline Unemployment Rate | 5.80 | - | 04:00 |

- BCB Copom minutes due today after confusing decision

- Bovespa rises 1.06% while USD/BRL falls to 5.14

- Brazil exports to US hit 30-year low on tariffs

Yesterday's Recap

Markets digested the prior COPOM decision with Bovespa advancing 1.06% to 170,370 amid firmer commodity sentiment. USD/BRL eased 0.20% to 5.14 as the short-term rate held at 14.50%. Treasury canceled a scheduled domestic bond auction to reduce volatility after the decision drew criticism for mixed signals.

Brazil exports to the US dropped to a 30-year low following new tariffs, weighing on trade balances. Investor focus shifted to today's minutes for clearer forward guidance on the Selic path. No data releases occurred on June 22, leaving price action driven by external flows and policy noise.

The Day Ahead

BCB releases COPOM meeting minutes at 03:00 ET, expected to address the dovish tone that triggered negative market reaction. The print will likely shape expectations for any further easing from the current 14.50% Selic level. On Friday, the headline unemployment rate is scheduled for 04:00 ET with the prior print at 5.8%.

Markets will monitor whether labor data reinforces resilience or adds pressure on fiscal accounts. No other Brazil-specific events are listed through tomorrow.

Other Economic Notes

High Selic rates continue to constrain domestic demand while fiscal policy remains the key offset for growth. China signaled higher beef import volumes, with Brazil already using 70% of its 1.106 million ton quota and seeking tariff relief. Previ, Brazil's largest pension fund, adopted a hands-off stance on Vale chairperson selection to promote independent oversight.

Office supply in Sao Paulo is set for its largest delivery in a decade, testing absorption in the Pinheiros district.

Global Macro News

US tariffs have sharply reduced Brazilian shipments, amplifying pressure on export revenues and the trade surplus. China’s rising beef demand offers partial offset but tariff renegotiation remains critical for margins. Softer oil prices supported broader EM currencies including the real overnight.

Indonesia’s $1.48bn stimulus targets energy and currency stability, illustrating regional responses to similar external shocks. Yen weakness persists absent a hawkish BOJ pivot, limiting safe-haven flows away from BRL assets. Global risk sentiment stayed cautious with Bitcoin and gold both declining.