Brazil Macro Daily(Beta Mode)

Copom Minutes Signal Data-Dependent Easing

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,259.00 | +0.52% |

| USD/BRL | 5.19 | +0.66% |

| EUR/BRL | 5.89 | +0.06% |

| Vale | 15.43 | -0.68% |

| Petrobras | 16.49 | -1.82% |

| WTI Crude | 72.06 | -1.57% |

| Gold | 4,096.10 | -0.82% |

| Bitcoin | 62,614.19 | -0.09% |

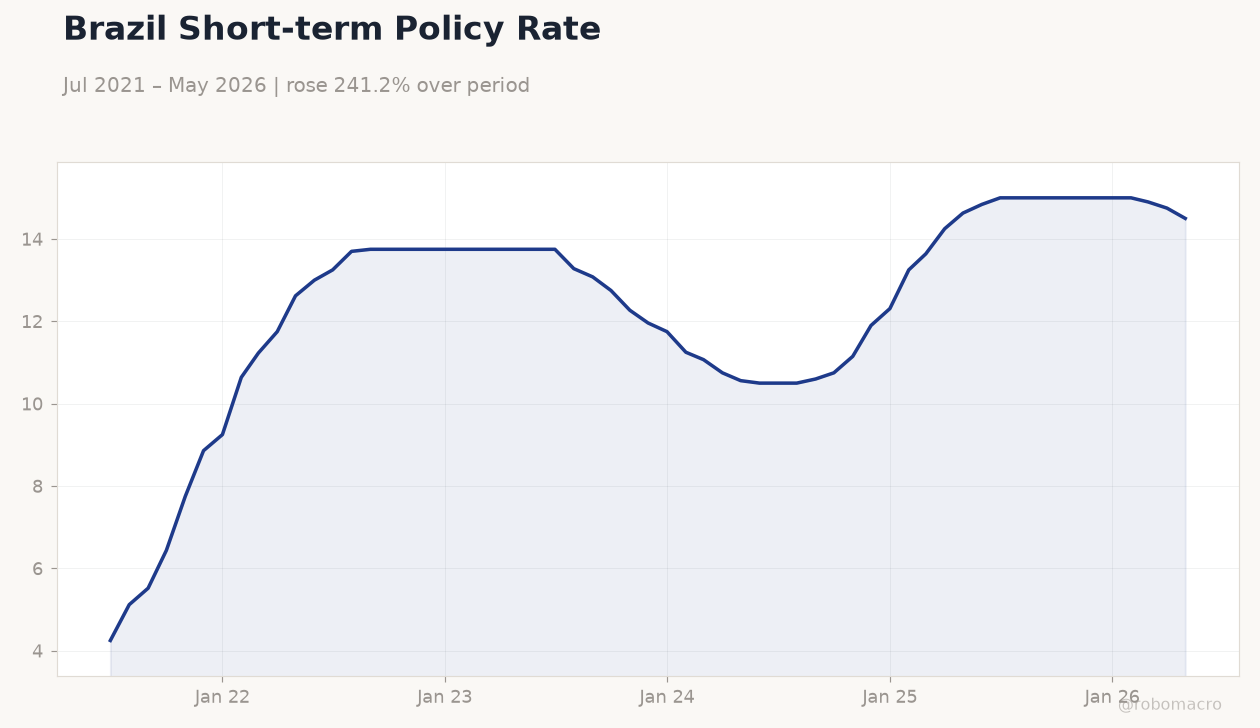

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | - |

Brazil Short-term Policy Rate | Type: macro_line | Selic Rate (%): 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Short-term Policy Rate | Type: macro_line | Selic Rate (%): 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-26) | |||

| Headline Unemployment Rate | 5.80 | 5.60 | 04:00 |

- BCB minutes underscore cautious easing amid rising risks, keeping Selic at 14.50%.

- Bovespa rose 0.52% while USD/BRL climbed 0.66% to 5.19 on mixed commodity flows.

- Unemployment print due Friday offers next key signal for COPOM timing.

Yesterday's Recap

The BCB released COPOM meeting minutes that stressed adjustments to the easing cycle will depend on incoming data after policymakers reviewed multiple Selic paths. Markets digested the cautious tone with Bovespa advancing 0.52% to 171,259 while the short-term rate fell 1.69% to 14.50%. USD/BRL rose 0.66% to 5.19, reflecting modest real depreciation, and EUR/BRL edged 0.06% higher.

Vale declined 0.68% and Petrobras fell 1.82% as WTI crude dropped 1.57%. The minutes reinforced that the committee will calibrate future moves strictly on inflation and activity prints rather than pre-commit to a fixed pace.

The Day Ahead

Attention turns to Friday’s headline unemployment rate, expected at 5.6% versus 5.8% prior, which will feed directly into BCB labor-market assessments. No domestic releases are scheduled for today, leaving room for external drivers such as iron-ore and oil prices to influence BRL flows. Regional political developments in Colombia may also shape investor perceptions of Latin American policy convergence.

Liquidity data and any follow-up COPOM commentary could provide incremental color on the Selic trajectory.

Other Economic Notes

Brazil’s primary fiscal balance printed a stronger-than-expected surplus last month, trimming pressure on longer-term yields. Commodity export revenues remain supported by China’s steady iron-ore demand, though JBS has paused beef shipments after quota thresholds that could trigger higher tariffs. The Pemex-Petrobras cooperation agreement opens scope for joint upstream and refining projects, potentially lifting medium-term oil output.

Global Macro News

China’s iron-ore import growth continues to underpin Brazilian export earnings despite softer global prices. Middle East supply concerns lifted WTI earlier in the week before today’s pullback, keeping oil-linked revenues volatile. Apple’s Brazil tax concessions have drawn scrutiny over their impact on local developer incentives versus Chinese competition.

Broader Latin American rightward political shifts may improve external perceptions of Brazilian fiscal discipline. <i>↓ p.2</i>