Brazil Macro Daily(Beta Mode)

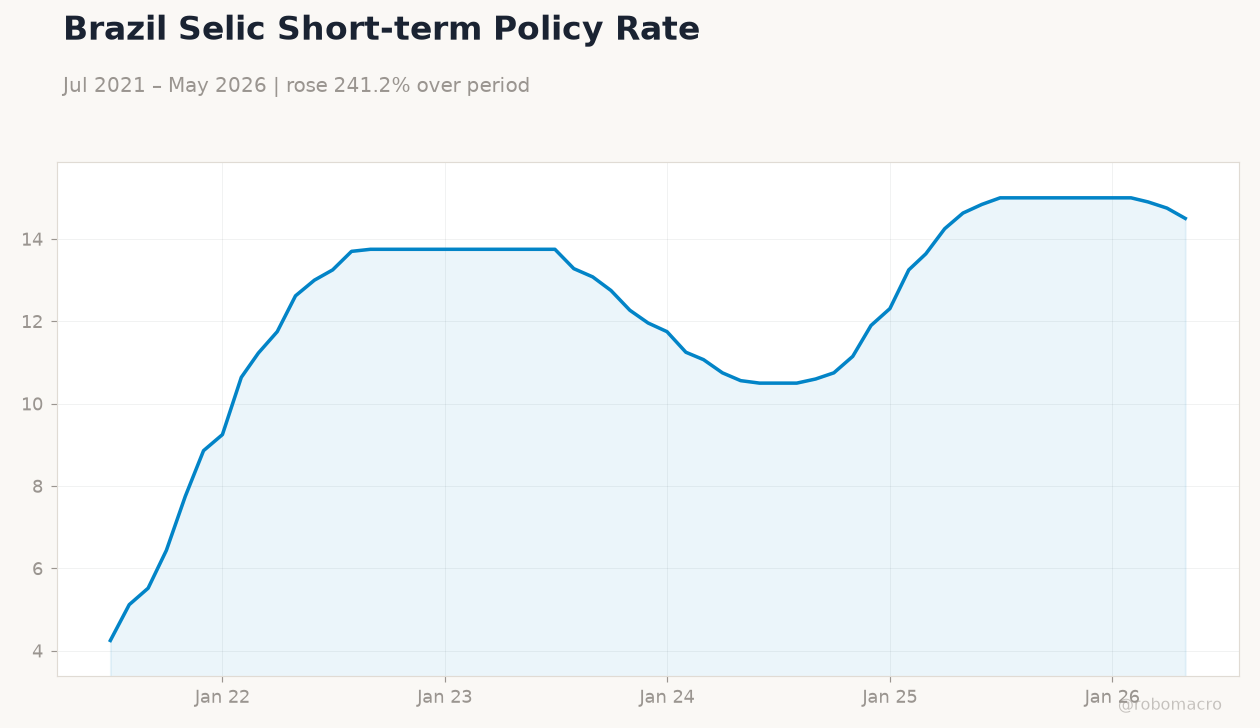

Copom Minutes Reinforce Cautious Stance

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 170,507.00 | -0.44% |

| USD/BRL | 5.20 | +0.01% |

| EUR/BRL | 5.90 | -0.12% |

| Vale | 14.92 | -2.55% |

| Petrobras | 16.34 | -4.05% |

| WTI Crude | 69.56 | -1.11% |

| Gold | 4,000.30 | +0.25% |

| Bitcoin | 61,383.37 | +0.64% |

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | - |

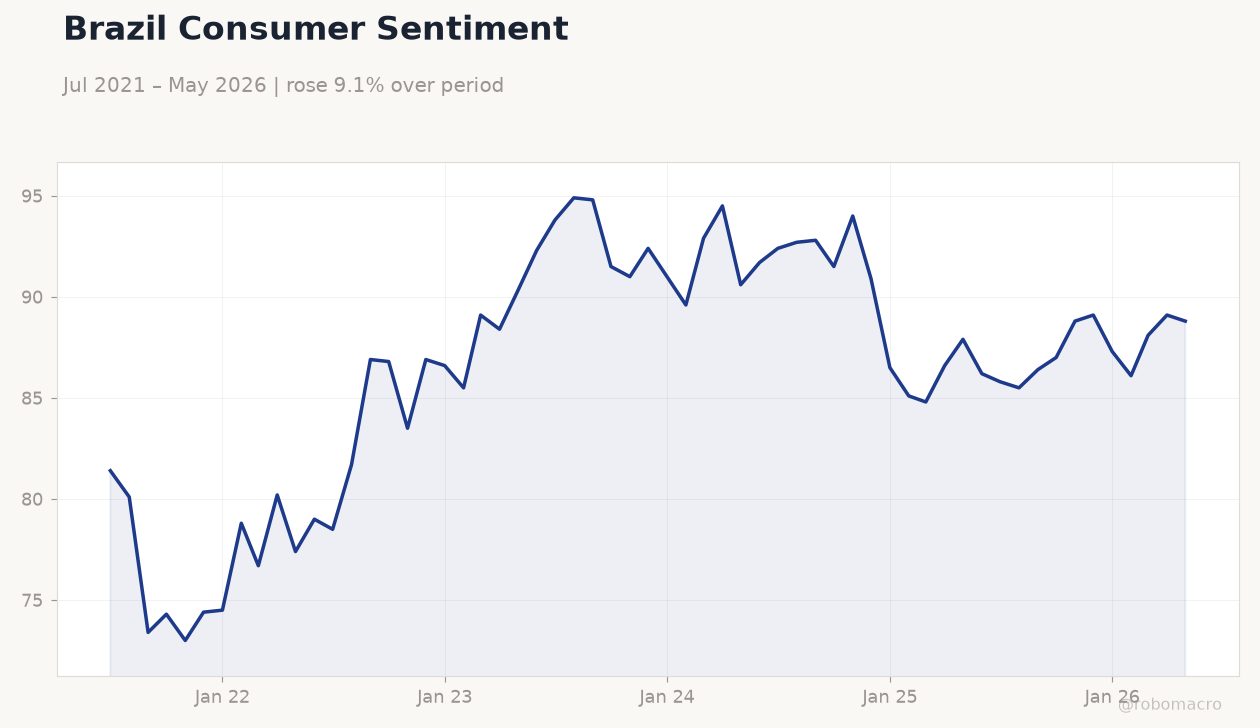

Brazil Consumer Sentiment | Type: macro_line | Index: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Brazil Consumer Sentiment | Type: macro_line | Index: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-26) | |||

| Headline Unemployment Rate | 5.80 | 5.60 | 04:00 |

- Copom minutes underscore data-dependent approach after recent Selic cut to 14.50%.

- Bovespa fell 0.44% as Petrobras and Vale shares dropped over 4% and 2.5%.

- Unemployment print due tomorrow expected to ease to 5.6% from 5.8%.

Yesterday's Recap

The BCB released Copom meeting minutes on June 24, highlighting the committee’s focus on inflation convergence within the target range while acknowledging persistent services price pressures. Markets digested the communication without major surprises, leaving the Selic at 14.50% after the prior reduction. Bovespa closed 0.44% lower at 170,507 amid broad commodity weakness.

Petrobras shares declined 4.05% to 16.34 while Vale fell 2.55% to 14.92 as iron ore prices softened. USD/BRL edged 0.01% higher to 5.20, showing limited reaction to the minutes. Short-term Brazilian rates eased 1.69% to 14.50%, reflecting market pricing of a stable policy stance ahead of fresh labor data.

The Day Ahead

Brazil’s headline unemployment rate for May is scheduled for release at 04:00 ET tomorrow, with consensus pointing to a 5.6% reading versus 5.8% previously. Analysts will assess whether the improvement supports household consumption or signals slower hiring momentum. No other high-impact domestic releases are listed for today.

Market participants will monitor global commodity flows, particularly iron ore and oil, given their direct influence on BRL and fiscal revenues. Attention also turns to any follow-up comments from BCB officials on the minutes.

Other Economic Notes

Social mobility indicators have improved modestly yet remain vulnerable to labor market slack and inflation volatility, according to Valor International analysis. A new platform launched this week aims to channel Chinese capital into Brazilian equities, potentially broadening the investor base for B3 listings. Fiscal sustainability concerns persist as commodity export receipts face downside risks from softer global demand.

Fixed-income strategists at Empiricus note that the recent Selic cut opens opportunities in select credit instruments while cautioning on duration exposure.

Global Macro News

Seth Klarman highlighted value in Brazilian bonds following recent price dislocations, signaling selective foreign interest in local debt. WTI crude fell 1.11% to 69.56, weighing on Petrobras and government oil-linked revenues. <i>↓ p.2</i>