Brazil Macro Daily(Beta Mode)

Bovespa Rises as Real Firms After Copom Minutes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,990.00 | +0.87% |

| USD/BRL | 5.18 | -0.51% |

| EUR/BRL | 5.91 | -0.00% |

| Vale | 14.84 | -3.07% |

| Petrobras | 16.34 | -4.05% |

| WTI Crude | 69.39 | -3.52% |

| Gold | 4,048.80 | +0.45% |

| Bitcoin | 60,024.95 | +0.51% |

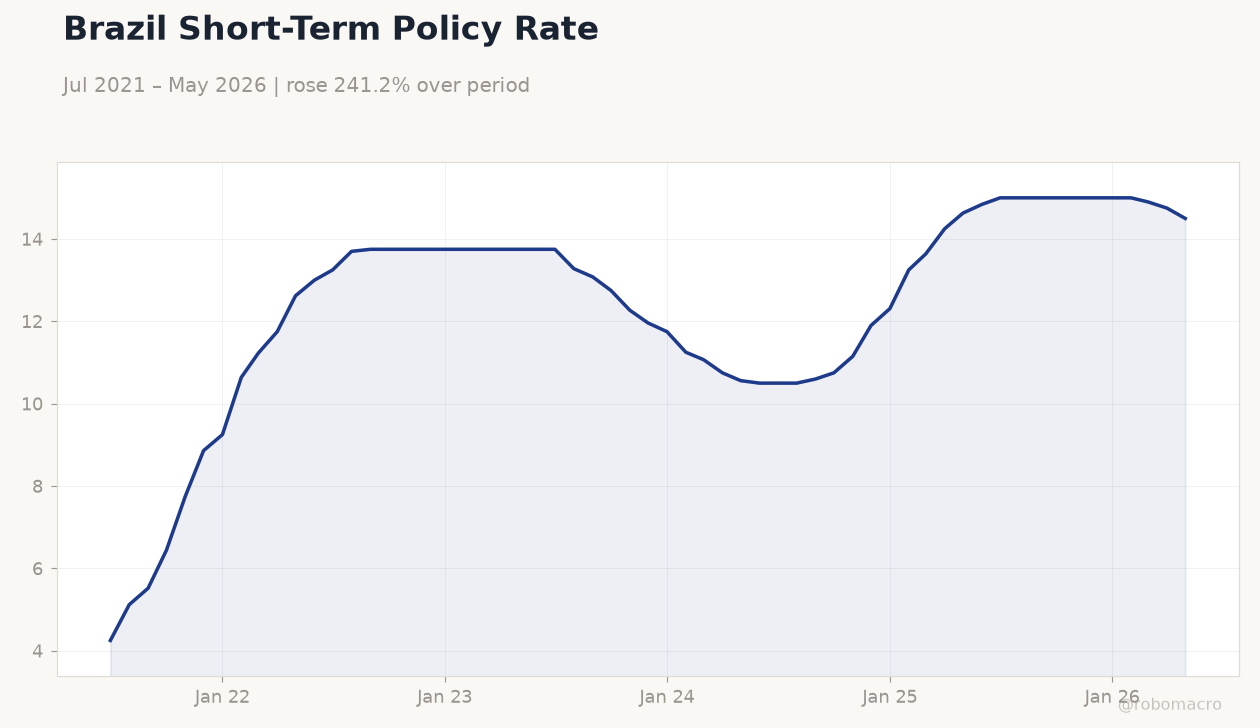

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BCB Copom Meeting Minutes | - | - | - |

Brazil Short-Term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Brazil Short-Term Policy Rate | Type: macro_line | Policy Rate %: 14.5 (2026-05-01) | Range: 4.25–15 | Trend(6pt): 4.25,13.75,12.27,12.31,14.9,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 5.80 | 5.60 | 04:00 |

- Bovespa rose 0.87% to 171,990 while USD/BRL fell 0.51% to 5.18 after release of Copom minutes.

- Brazil short-term rate held at 14.50% with markets showing limited conviction on near-term easing.

- S&P affirmed BB rating despite persistent fiscal fragility concerns highlighted in latest assessment.

Yesterday's Recap

Copom minutes released yesterday offered no fresh forward guidance on the Selic path, leaving markets to focus on incoming data. Bovespa advanced 0.87% to close at 171,990, led by financials amid stable rates. USD/BRL declined 0.51% to 5.18 as the real benefited from modest risk-on flows.

Vale fell 3.07% to 14.84 and Petrobras dropped 4.05% to 16.34 despite the broader equity gain. WTI crude slid 3.52% to 69.39 while gold edged 0.45% higher to 4,048.80. The Brazil short-term rate remained at 14.50%, down 1.69% on the day in yield terms.

No major surprises emerged from the minutes beyond confirmation of the committee’s data-dependent stance.

The Day Ahead

Headline unemployment rate for May prints at 04:00 ET with consensus at 5.6% versus 5.8% prior. Traders will parse any downside surprise for clues on labor-market cooling and its effect on inflation. The print could shift DI futures and USD/BRL if it undershoots expectations materially.

No senior BCB speakers are scheduled and COPOM minutes have already been digested. Focus remains on whether softer employment data revives cut bets for later meetings. Markets will also monitor any updates on the planned yuan-denominated bond issuance in China.

Other Economic Notes

S&P confirmed Brazil’s BB rating while underscoring ongoing fiscal fragility and reliance on external and monetary buffers. The Treasury continues preparations for its first yuan-denominated sovereign bond in China to diversify funding sources. Household financial vulnerability indices released this week show wide regional disparities that could pressure future social spending.

Petrobras confirmed diesel import resumption in July even as it accelerates domestic output projects. These developments highlight authorities’ efforts to manage external liquidity while domestic fiscal space stays constrained.