Brazil Macro Daily(Beta Mode)

Bovespa Rises as Real Firms on Selic Hold

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 173,295.00 | +0.76% |

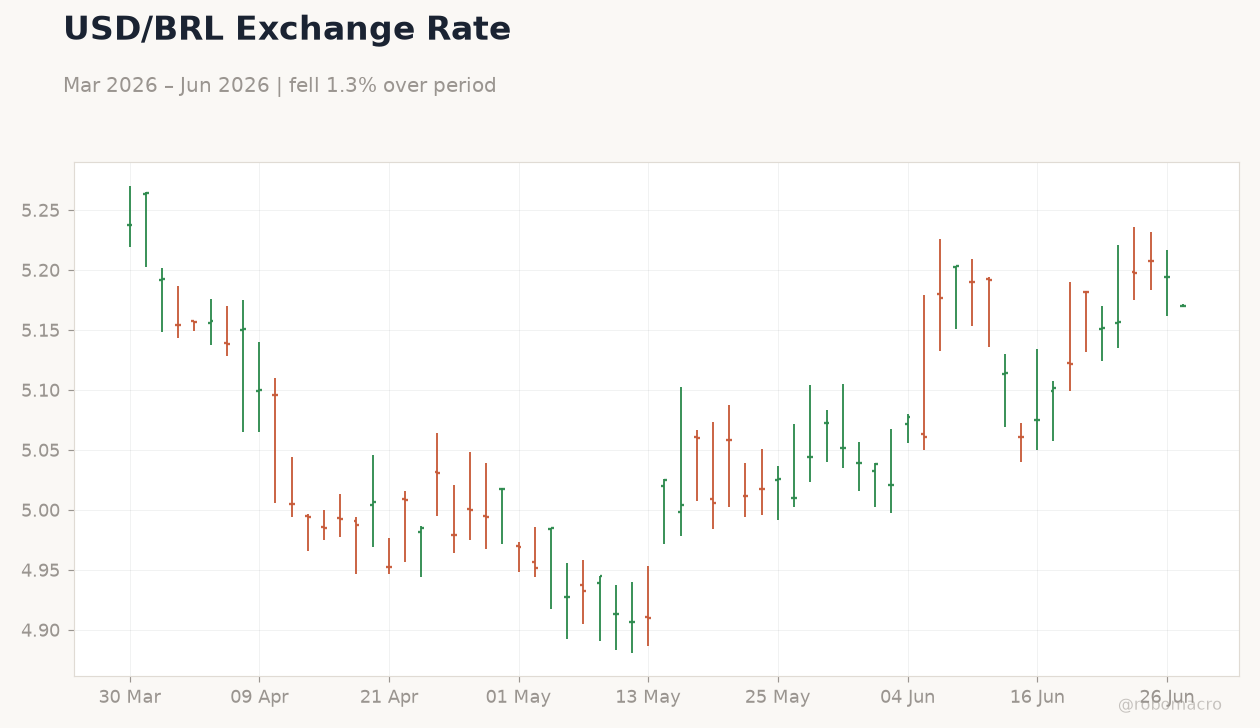

| USD/BRL | 5.17 | -0.46% |

| EUR/BRL | 5.89 | -0.03% |

| Vale | 15.07 | -0.33% |

| Petrobras | 16.29 | -1.39% |

| WTI Crude | 69.89 | +0.95% |

| Gold | 4,052.00 | -0.65% |

| Bitcoin | 60,069.96 | +0.90% |

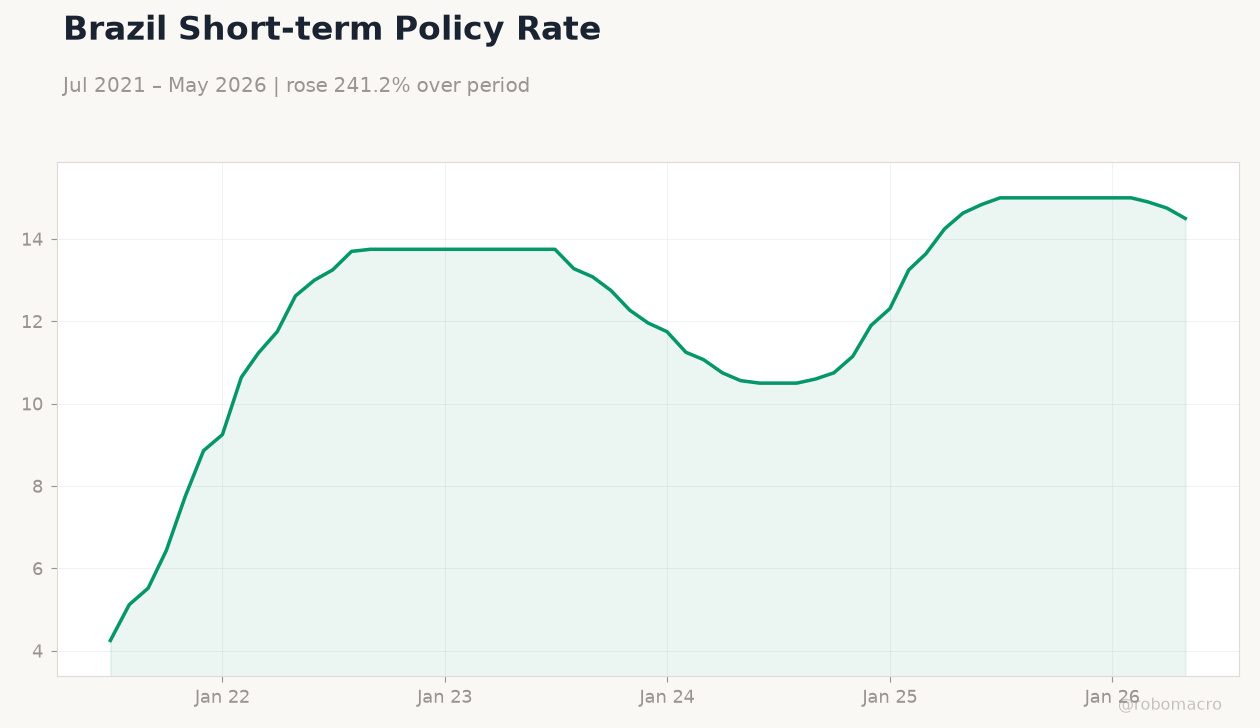

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

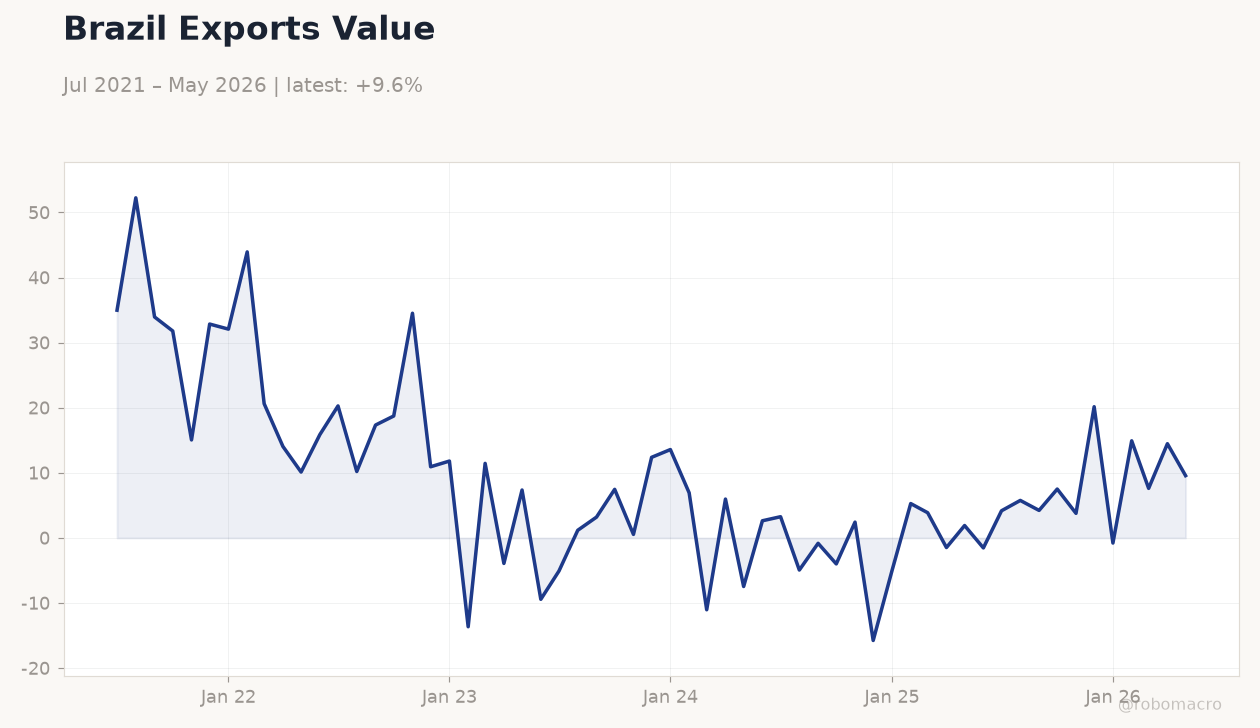

Brazil Exports Value | Type: macro_line | Exports (USD mn): 9.567 (2026-05-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.614,9.567

Brazil Exports Value | Type: macro_line | Exports (USD mn): 9.567 (2026-05-01) | Range: -15.76–52.25 | Trend(6pt): 34.98,17.34,0.5414,-5.056,7.614,9.567

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-07-02) | |||

| Industrial Production Month-over-Month | 0.70 | - | 04:00 |

| Friday (2026-07-03) | |||

| S&P Global Services PMI | - | - | 05:00 |

- Bovespa rose 0.76% to 173,295 while USD/BRL fell 0.46% to 5.17 on steady Selic at 14.50%.

- IFI projects Brazil gross debt reaching 115% of GDP by 2036 amid persistent fiscal gaps.

- Industrial Production MoM and Services PMI scheduled for early July will test growth momentum.

Yesterday's Recap

Equity and currency markets advanced on June 28 with Bovespa closing at 173,295 after a 0.76% gain. USD/BRL eased to 5.17, reflecting a 0.46% real appreciation against the dollar. The short-term rate remained anchored at 14.50%.

Vale declined 0.33% to 15.07 while Petrobras fell 1.39% to 16.29 despite WTI crude rising 0.95% to 69.89. No economic releases occurred on the calendar. Bitcoin gained 0.90% to 60,069.96 and gold slipped 0.65% to 4,052.

Market participants focused on external commodity signals and the unchanged policy rate.

The Day Ahead

Industrial Production MoM for May releases at 04:00 ET on July 2 with a 0.7% prior reading. S&P Global Services PMI follows at 05:00 ET on July 3. The BCB Focus survey and FGV Consumer Confidence data are also due this week.

Markets will monitor whether production rebounds support the current Selic path. Any downside surprise in PMI could reinforce expectations for prolonged tightness at 14.50%. Traders will watch for revisions to growth forecasts ahead of the next COPOM meeting.

Other Economic Notes

Brazil’s fiscal trajectory remains under pressure after the IFI warned of debt climbing to 115% of GDP by 2036. Stronger tax receipts produced a narrower primary deficit in May, yet spending rigidities persist. A new tax office opened in Beijing to streamline trade procedures with China, Brazil’s largest iron-ore buyer.

These measures aim to support export revenues but do not alter near-term debt dynamics. Analysts continue to flag limited fiscal space for additional stimulus while the Selic stays elevated.

Global Macro News

The dollar’s recent firmness globally has been tempered by softer US data, aiding the real’s 0.46% gain. WTI crude at 69.89 supports Brazil’s oil export receipts despite Petrobras share weakness. Iron-ore futures benefited from China’s industrial output beat, providing a modest lift to Vale.

<i>↓ p.2</i>