Brazil Macro Daily(Beta Mode)

Selic Holds at 14.50% as Bovespa Stays Flat

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 173,205.00 | -0.05% |

| USD/BRL | 5.17 | -0.08% |

| EUR/BRL | 5.89 | +0.05% |

| Vale | 15.03 | -0.27% |

| Petrobras | 16.28 | -0.06% |

| WTI Crude | 70.68 | -0.10% |

| Gold | 4,030.20 | +0.20% |

| Bitcoin | 59,261.30 | -1.46% |

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

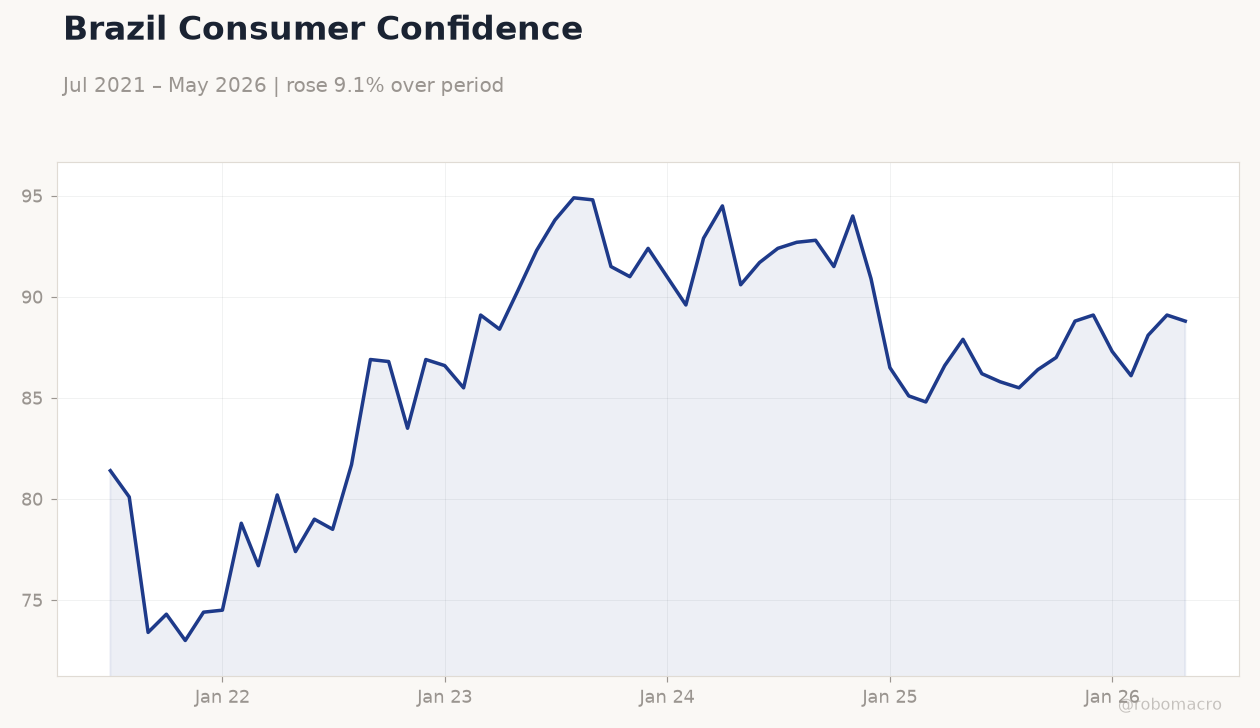

Brazil Consumer Confidence | Type: macro_line | Index: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Brazil Consumer Confidence | Type: macro_line | Index: 88.8 (2026-05-01) | Range: 73–94.9 | Trend(6pt): 81.4,86.9,91,86.5,88.1,88.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-07-02) | |||

| Industrial Production Month-over-Month | 0.70 | - | 04:00 |

| Friday (2026-07-03) | |||

| S&P Global Services PMI | - | - | 05:00 |

- Bovespa closed at 173,205 (-0.05%) with USD/BRL at 5.17 (-0.08%) as the Selic rate remained at 14.50%.

- No data releases occurred on June 29, leaving markets focused on fiscal signals and labor-market disconnects.

- Industrial Production MoM and Services PMI scheduled for early July will test domestic demand resilience.

Yesterday's Recap

Brazilian markets recorded minimal moves on June 29 with the Bovespa ending 0.05% lower at 173,205 and USD/BRL slipping 0.08% to 5.17. The short-term rate held at 14.50% after a 1.69% daily decline in the benchmark futures contract. No economic indicators were released, so price action reflected thin positioning ahead of the July holiday period.

Vale fell 0.27% and Petrobras declined 0.06% despite stable WTI crude at 70.68. EUR/BRL edged 0.05% higher to 5.89 while gold rose 0.20% to 4,030.20. Bitcoin dropped 1.46% to 59,261.30.

The absence of fresh data left the curve and currency range-bound.

The Day Ahead

Industrial Production Month-over-Month for May releases at 04:00 ET on July 2 and carries medium impact. The print follows a 0.7% prior reading and will inform Q2 manufacturing momentum. S&P Global Services PMI appears at 05:00 ET on July 3, providing the first services-sector gauge for June.

Both releases arrive before the July 4 holiday and could shift short-end DI futures if surprises exceed 0.5 percentage points. Traders will also monitor any BCB speeches for clues on the 14.50% Selic path.

Other Economic Notes

Brazil’s labor market remains firm yet consumer confidence has not improved, according to Valor International analysis, highlighting weak transmission from employment to spending. Franklin Templeton warned the country risks another “chicken flight” episode given poor fiscal dynamics and limited market pressure for policy change. The government committed US$100 million annually to the Mercosul structural convergence fund, a modest fiscal outlay unlikely to alter primary-balance targets.

Iron-ore and soybean export volumes continue to support the trade surplus despite softer global prices.

Global Macro News

WTI crude settled at 70.68, down 0.10%, limiting upside for Petrobras and the BRL despite steady Chinese demand signals. Gold advanced 0.20% to 4,030.20, offering a modest safe-haven bid that capped USD/BRL losses. <i>↓ p.2</i>