Brazil Macro Daily(Beta Mode)

DI Futures Slide on Weak CAGED Jobs Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 172,024.00 | -0.68% |

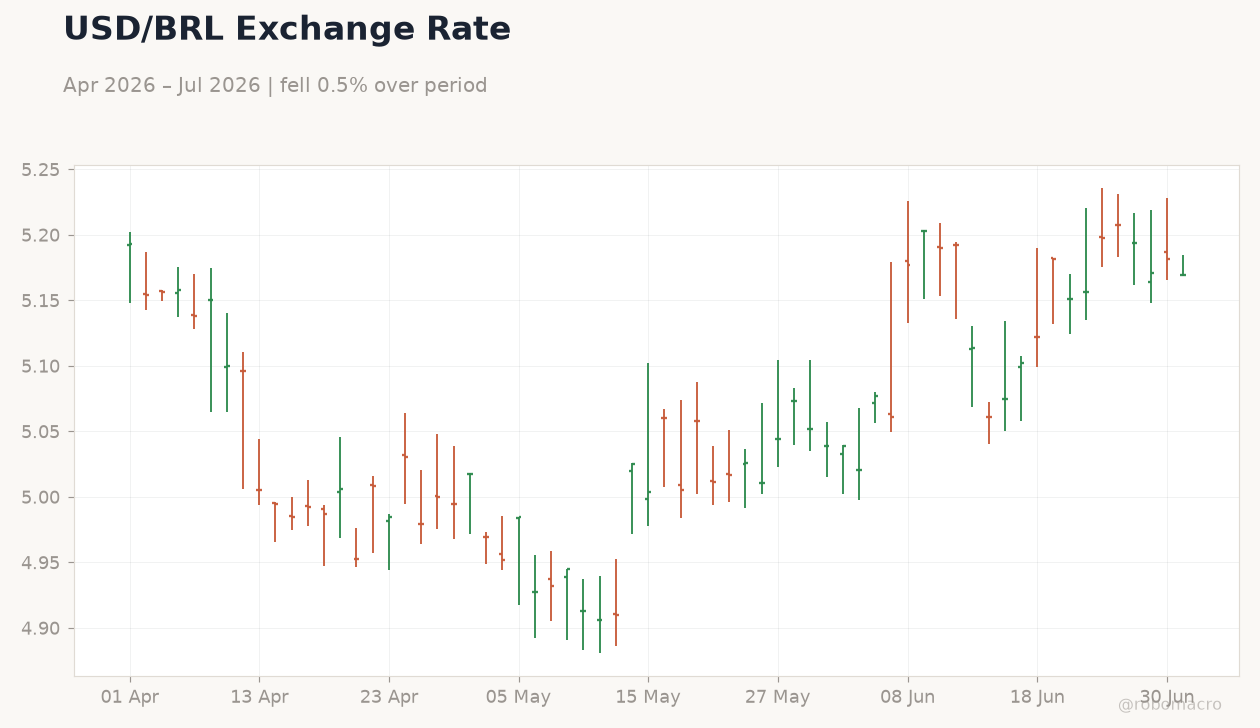

| USD/BRL | 5.17 | -0.24% |

| EUR/BRL | 5.89 | -0.44% |

| Vale | 15.04 | +0.07% |

| Petrobras | 16.16 | -0.74% |

| WTI Crude | 68.66 | -1.21% |

| Gold | 3,989.30 | -0.84% |

| Bitcoin | 58,900.24 | +0.58% |

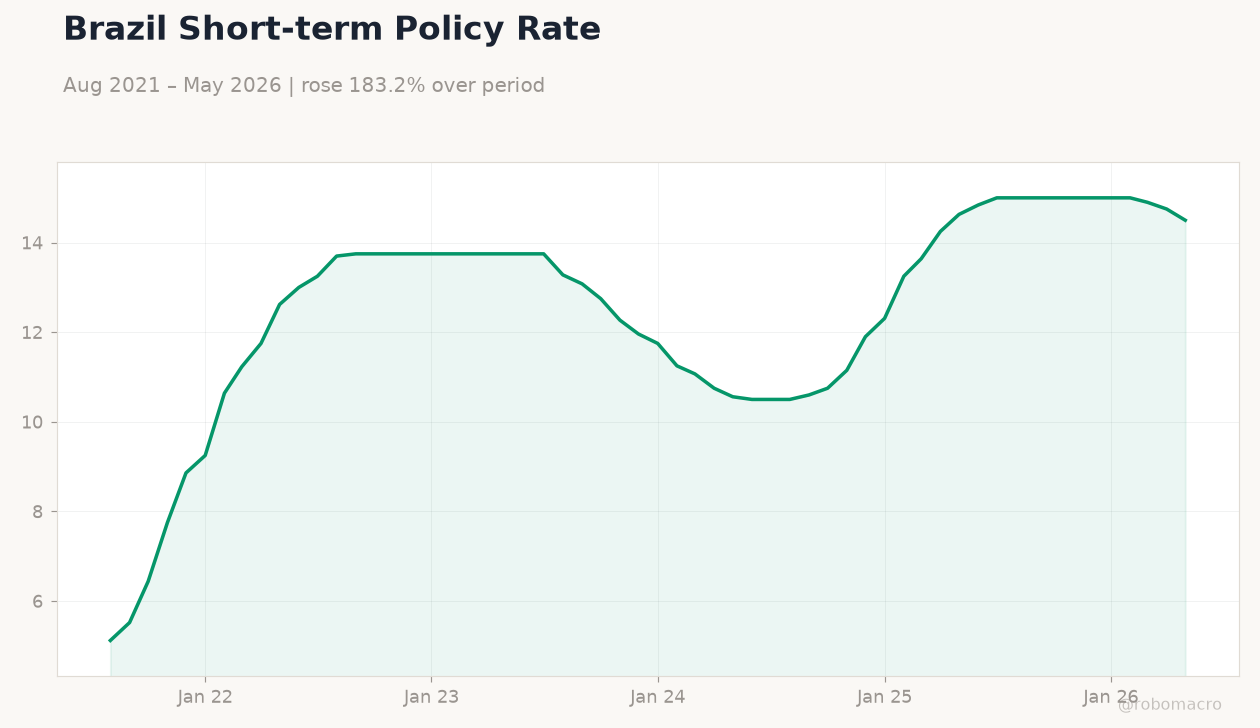

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

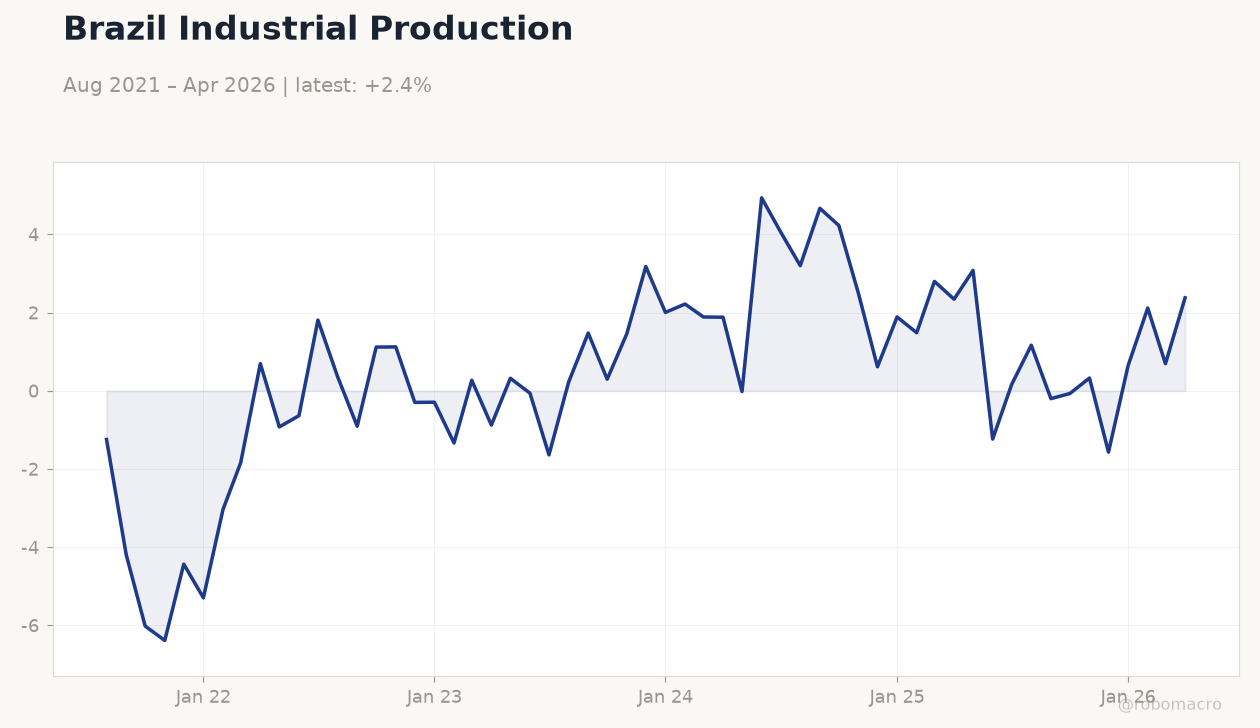

Brazil Industrial Production | Type: macro_line | Industrial Production (YoY %): 2.38 (2026-04-01) | Range: -6.386–4.937 | Trend(5pt): -1.245,1.119,3.181,1.486,2.38

Brazil Industrial Production | Type: macro_line | Industrial Production (YoY %): 2.38 (2026-04-01) | Range: -6.386–4.937 | Trend(5pt): -1.245,1.119,3.181,1.486,2.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-07-02) | |||

| Industrial Production Month-over-Month | 0.70 | - | 08:00 |

| Friday (2026-07-03) | |||

| S&P Global Services PMI | - | - | 09:00 |

| Monday (2026-07-06) | |||

| Trade Balance | 7,820m | - | 14:00 |

| Wednesday (2026-07-08) | |||

| Retail Sales Month-over-Month | -1.50 | - | 08:00 |

- Brazil's May Caged jobs print of 72,960 fell short of expectations, pushing DI futures lower and lifting odds of an August Selic cut.

- Bovespa closed 0.68% lower at 172,024 while USD/BRL eased 0.24% to 5.17 amid thin holiday-week volumes.

- Selic held at 14.50% with markets now pricing roughly 25 bp of easing by the August COPOM meeting.

Yesterday's Recap

Equity and rates markets digested the weaker-than-expected Caged employment release for May, which showed only 72,960 formal jobs added. DI futures across the curve declined as participants increased bets on an August Selic reduction. Bovespa fell 0.68% to 172,024 while Petrobras shares dropped 0.74%.

USD/BRL traded 0.24% lower at 5.17, supported by softer US data and thin pre-holiday liquidity. The Brazil short-term rate remained at 14.50%. No major data releases occurred on June 30, leaving the Caged print as the dominant driver of price action.

The Day Ahead

Industrial Production MoM for May is due Thursday at 08:00 ET, with markets expecting a modest rebound after April's 0.7% gain. S&P Global Services PMI follows on Friday, providing an early read on July activity. Trade balance figures arrive Monday and Retail Sales MoM on July 8, both carrying medium impact.

Traders will also monitor any BCB speakers for clues ahead of the next COPOM decision. Thin holiday liquidity may amplify moves in USD/BRL and DI futures.

Other Economic Notes

UBS data showed Brazil added 9,200 millionaires in 2025 while average real wealth fell 3.13% since 2020, underscoring persistent inequality. The government will reauction power transmission assets following a legal settlement, potentially unlocking fresh infrastructure investment. Tax exemptions granted for the 2027 Women's World Cup services aim to support event-related spending without straining municipal budgets.

Commodity exporters continue to benefit from steady iron ore and oil demand despite softer global growth signals.

Global Macro News

UK GDP outperformance lifted G7 growth rankings and supported risk sentiment for EM currencies including BRL. The RBA warned that high rates are weighing on activity yet signaled further tightening may still be required, keeping commodity currencies in focus. Japan's yen weakness to multi-decade lows raises imported inflation risks that could indirectly pressure Brazilian terms of trade.

<i>↓ p.2</i>