Brazil Macro Daily(Beta Mode)

BRL Weakens as Jobs Cool, Subsidies Ease

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 171,689.00 | -0.19% |

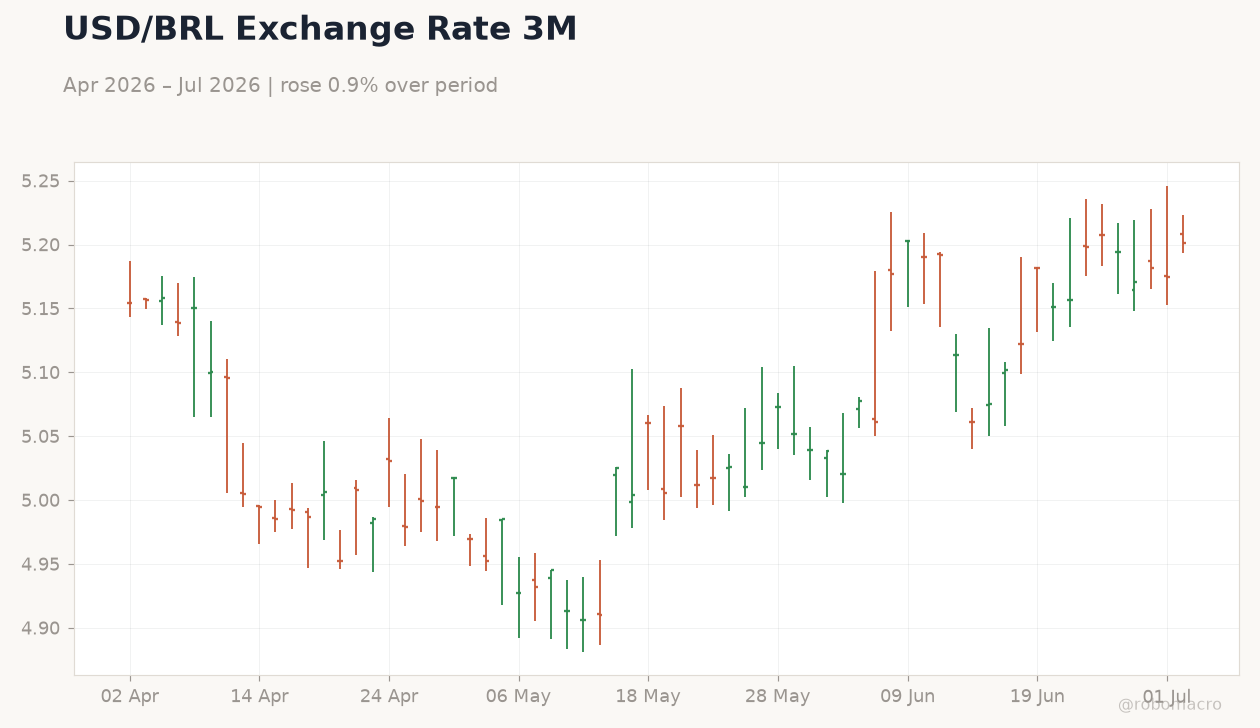

| USD/BRL | 5.21 | +0.66% |

| EUR/BRL | 5.94 | +0.65% |

| Vale | 14.90 | -0.93% |

| Petrobras | 15.99 | -1.05% |

| WTI Crude | 67.30 | -1.87% |

| Gold | 4,083.30 | +0.37% |

| Bitcoin | 61,220.62 | +2.03% |

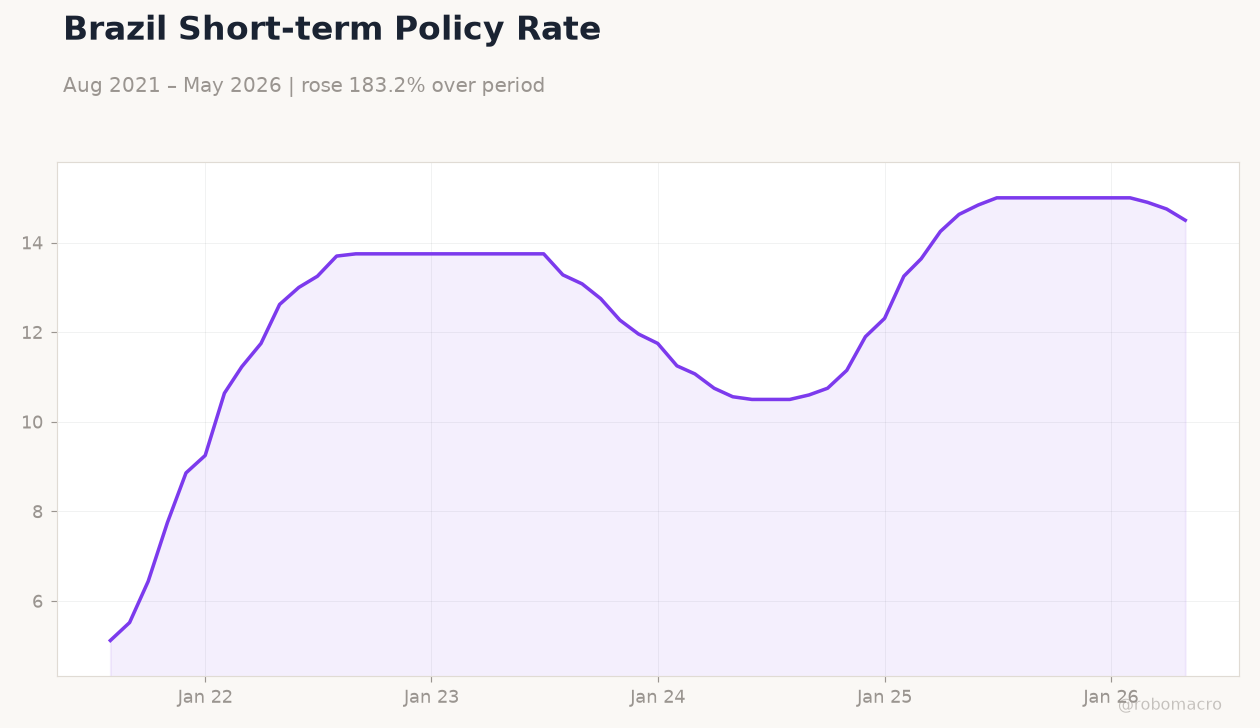

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

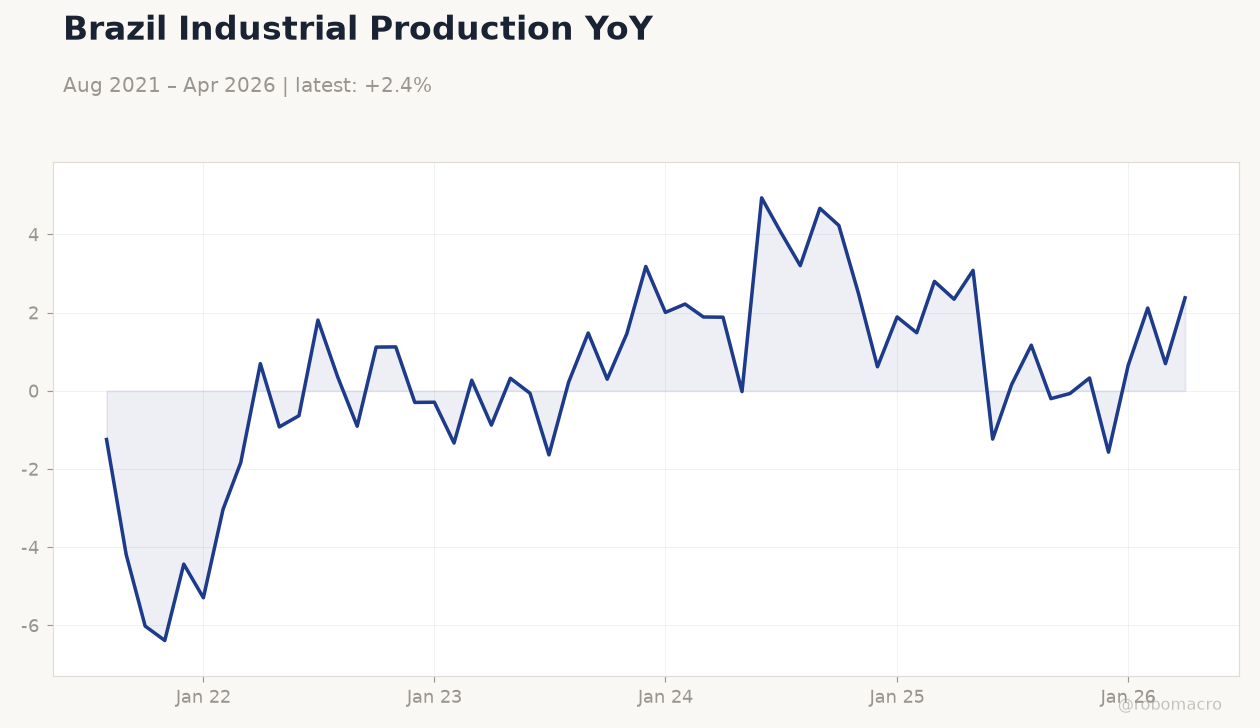

Brazil Industrial Production YoY | Type: macro_line | YoY %: 2.38 (2026-04-01) | Range: -6.386–4.937 | Trend(5pt): -1.245,1.119,3.181,1.486,2.38

Brazil Industrial Production YoY | Type: macro_line | YoY %: 2.38 (2026-04-01) | Range: -6.386–4.937 | Trend(5pt): -1.245,1.119,3.181,1.486,2.38

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-07-03) | |||

| Industrial Production Month-over-Month | 0.70 | 0.30 | 04:00 |

| S&P Global Services PMI | - | - | 05:00 |

- Bovespa fell 0.19% to 171,689 while USD/BRL rose 0.66% to 5.21 on thin volumes.

- Brazil short-term rate held at 14.50% with yields easing 1.69%.

- June industrial PMI rose to 50.8, signaling expansion, yet formal jobs data showed continued cooling.

Yesterday's Recap

Equity markets closed lower with Bovespa down 0.19% at 171,689 amid profit-taking in Vale and Petrobras, which declined 0.93% and 1.05%. The real weakened as USD/BRL climbed 0.66% to 5.21 and EUR/BRL gained 0.65% to 5.94. Short-term rates remained anchored at 14.50% while WTI crude dropped 1.87% to 67.30, pressuring commodity exporters.

Gold advanced 0.37% to 4,083.30 on safe-haven demand. Bitcoin rose 2.03% to 61,220.62. No major data releases occurred on July 1, leaving focus on the formal employment slowdown reported in recent weeks and the start of fuel subsidy phase-outs as oil prices eased.

The Day Ahead

Industrial Production MoM is due at 04:00 ET with consensus at 0.3% after 0.7% prior, a medium-impact print for BRL and yields. S&P Global Services PMI follows at 05:00 ET. Markets will watch for any revisions that could shift GDP nowcasts for 2026.

No COPOM speeches or minutes are scheduled. Traders will also monitor iron-ore export data to China for signs of sustained demand.

Other Economic Notes

Brazil’s formal job market continues its gradual slowdown, reducing wage pressures but highlighting softer labor demand. The government has begun phasing out fuel subsidies as global oil prices ease, supporting fiscal consolidation efforts. Industry showed renewed growth in June per PMI data, yet sales and production components softened, pointing to uneven momentum.

Fiscal targets for 2027 remain in focus after recent confirmations of a 0.5% GDP primary surplus goal. Crypto-asset service providers face tighter rules from 2027 onward, aiming to strengthen oversight.

Global Macro News

US sanctions on two Brazilians and three firms linked to PCC allegations add external pressure on bilateral ties and compliance costs. HKMA’s push for greater cross-border yuan usage could indirectly support BRL-yuan trade corridors for commodity flows. Middle East tensions easing could reduce oil-price volatility, benefiting Brazil’s import bill and Petrobras margins.

Latin American equities remain in a holding pattern, though Morgan Stanley keeps an overweight stance on Brazil despite domestic risks. Iron-ore and soybean export resilience to China continues to anchor the trade balance.