Brazil Macro Daily(Beta Mode)

IP Slowdown, Services PMI in Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Bovespa | 172,788.00 | +0.64% |

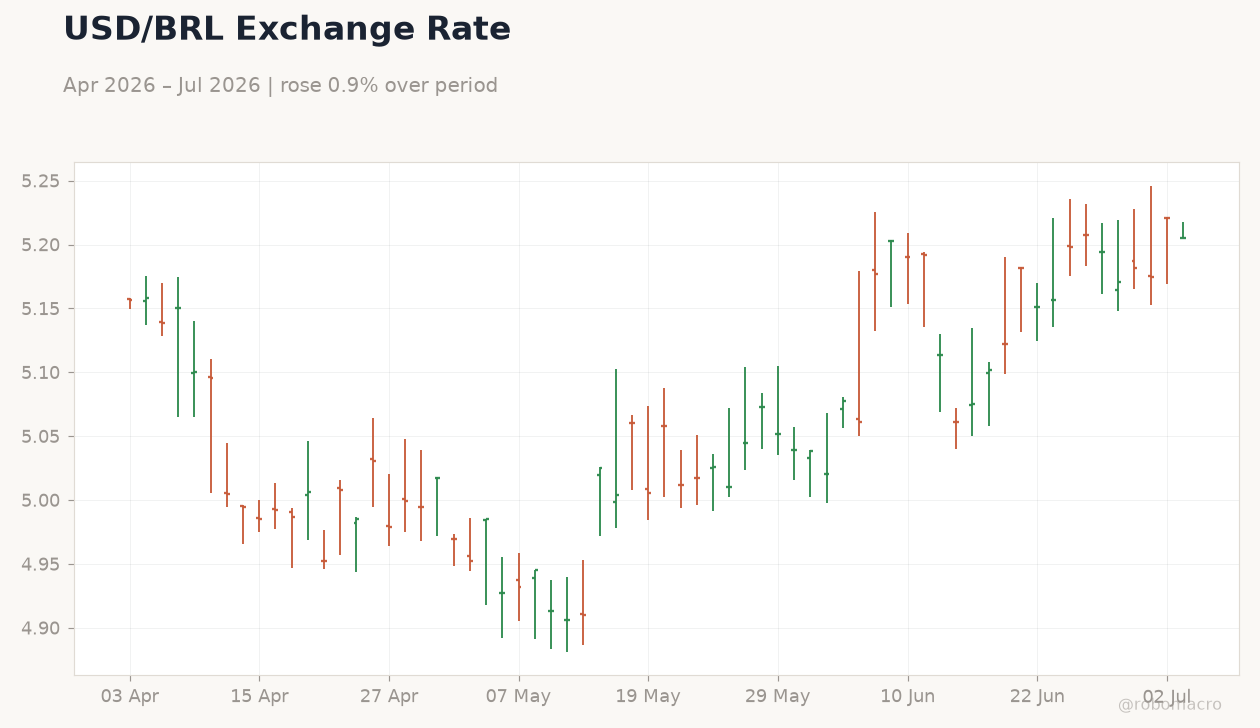

| USD/BRL | 5.21 | -0.30% |

| EUR/BRL | 5.98 | +0.68% |

| Vale | 14.99 | +0.60% |

| Petrobras | 16.11 | +0.75% |

| WTI Crude | 68.63 | -0.09% |

| Gold | 4,190.50 | +1.89% |

| Bitcoin | 61,485.33 | +0.00% |

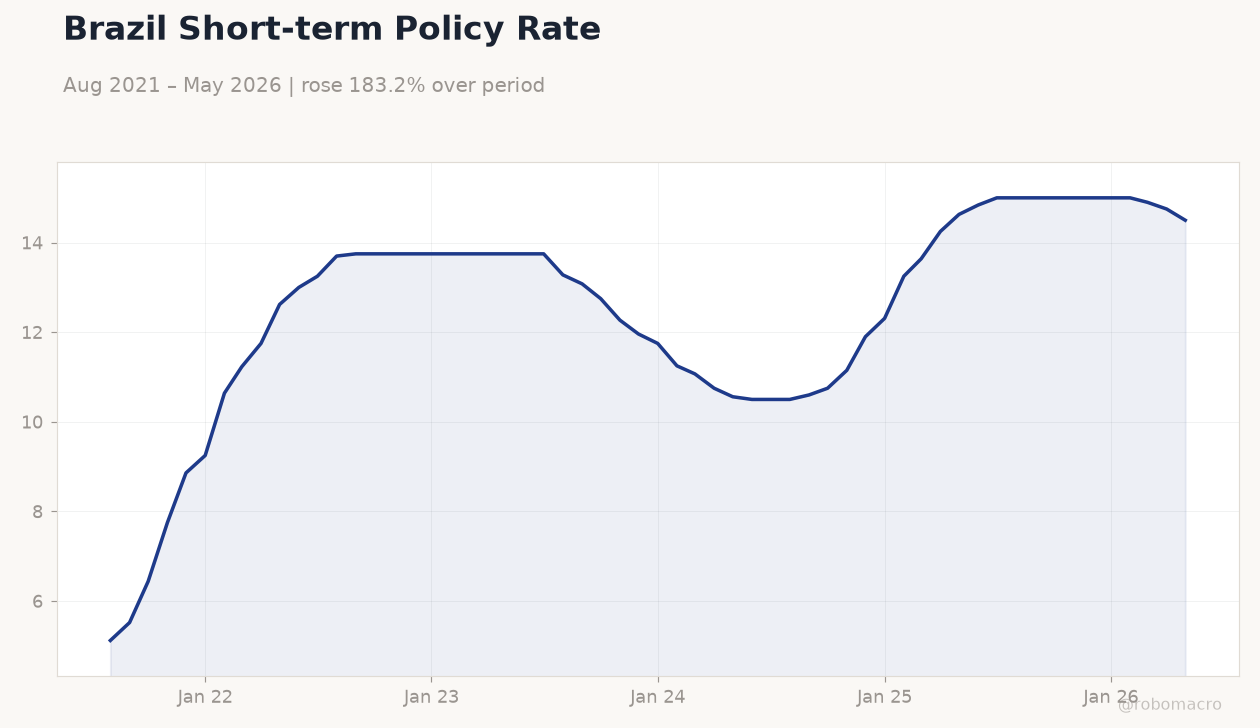

| Brazil Short-term Rate | 14.50% | -1.69% |

| Brazil Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brazil Short-term Policy Rate | Type: macro_line | Rate %: 14.5 (2026-05-01) | Range: 5.12–15 | Trend(6pt): 5.12,13.75,11.96,13.25,14.75,14.5

Brazil Short-term Policy Rate | Type: macro_line | Rate %: 14.5 (2026-05-01) | Range: 5.12–15 | Trend(6pt): 5.12,13.75,11.96,13.25,14.75,14.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | 0.70 | 0.30 | 04:00 |

| S&P Global Services PMI | - | - | 05:00 |

- Industrial production seen slowing to 0.3% MoM from 0.7% prior

- Bovespa rises 0.64% to 172,788 while USD/BRL eases 0.30% to 5.21

- Selic steady at 14.50% as fiscal risks temper cut expectations

Yesterday's Recap

Brazilian markets closed higher on July 2 with Bovespa advancing 0.64% to 172,788 amid firmer commodity prices. USD/BRL declined 0.30% to 5.21 while the short-term rate stood at 14.50%. Petrobras gained 0.75% and Vale added 0.60% on supportive iron-ore and oil moves.

Gold rose 1.89% to 4,190.50, providing further tailwinds for resource exporters. Fipe IPC inflation cooled to 0.18% in June from 0.45%, reinforcing the recent disinflation trend. No economic releases occurred, leaving price action driven by external flows and positioning ahead of today’s data.

The Day Ahead

Markets will focus on June industrial production due at 04:00 ET, with consensus at 0.3% MoM against a 0.7% prior reading. S&P Global Services PMI follows at 05:00 ET and will be watched for employment and new-orders signals. Both releases carry medium impact and could shift BRL volatility if outcomes deviate sharply.

Traders will also monitor any follow-through from recent state-owned company profit figures and dividend trends. A soft IP print may reinforce expectations for steady policy while a resilient services reading could support the real.

Other Economic Notes

Fiscal primary results and state-owned earnings highlight concentrated gains at Petrobras yet shrinking transfers to the Union. Infrastructure spending linked to data-center expansion is projected to draw up to US$5.5 trillion globally by 2030, offering Brazil new capex channels in energy and telecom. A major appliance maker’s shift of production from Argentina to Brazil underscores regional cost advantages.

These developments occur against persistent warnings from former officials that fiscal slippage could constrain any future easing cycle.

Global Macro News

Iron-ore and oil price stability continues to underpin Brazilian export revenues despite mixed global inventory data. Gold’s 1.89% advance reflects safe-haven demand that often correlates with BRL strength during risk-off episodes. Norges Bank’s stake reduction in Smartfit illustrates selective foreign positioning in Brazilian equities.

<i>↓ p.2</i>