Canada Macro Daily(Beta Mode)

Canada Trade Gap Widens Sharply

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,840.60 | -0.84% |

| USD/CAD | 1.37 | +0.58% |

| EUR/CAD | 1.57 | -0.15% |

| WTI Crude | 93.73 | -2.09% |

| Natural Gas | 3.27 | +1.24% |

| Gold | 5,098.80 | -0.33% |

| Brent Crude | 99.09 | -1.36% |

| Bitcoin | 72,334.09 | +2.61% |

| Canada 2Y Govt Yield | 2.25% | -0.06% |

| Canada 10Y Govt Yield | 3.40% | +0.41% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | -1,300m | -900m | -3,650m |

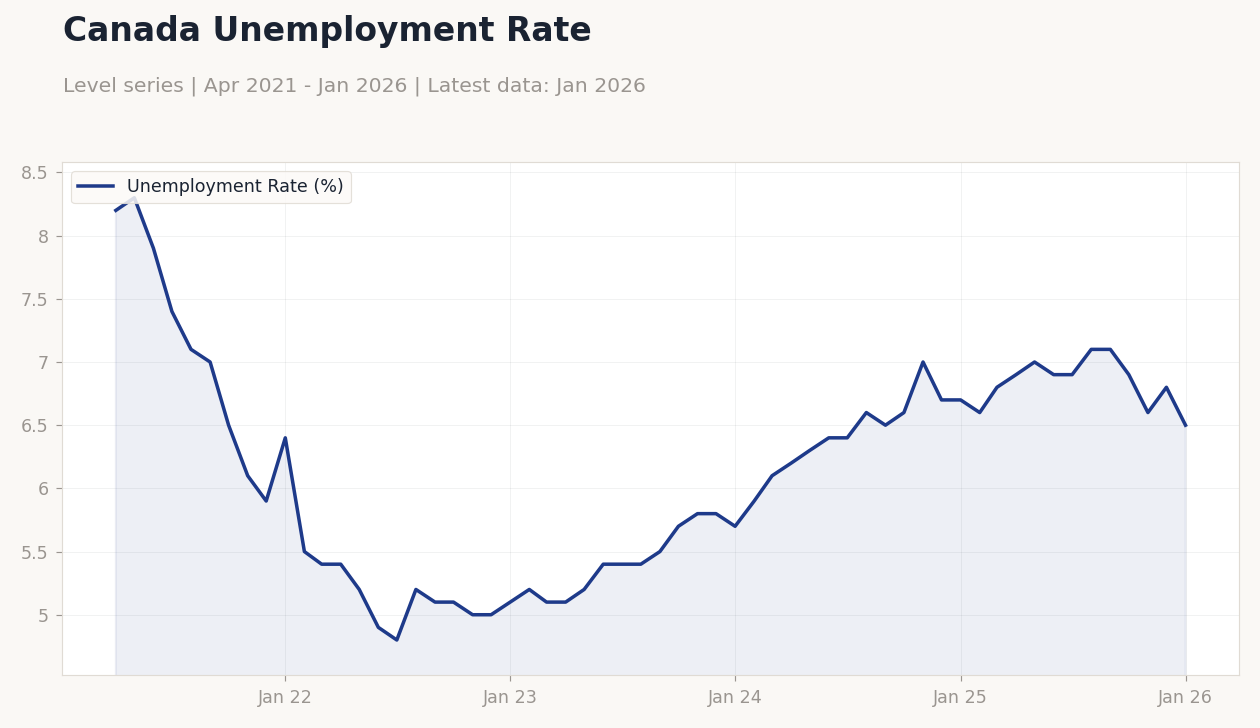

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(6pt): 8.2,4.9,5.4,6.6,6.8,6.5

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(6pt): 8.2,4.9,5.4,6.6,6.8,6.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6.50 | 6.60 | 04:30 |

| Employment Change | -24,800 | 10,000 | 04:30 |

| Full-Time Employment Change | 44,900 | - | 04:30 |

| Labor Force Participation | 65 | - | 04:30 |

| Part-Time Employment Change | -69,700 | - | 04:30 |

- Canada's January trade deficit surged to -C$3.65B, missing consensus of -C$0.9B and worsening from -C$1.3B prior, weighing on CAD.

- S&P/TSX dropped 0.84% amid energy sector weakness, with USD/CAD up 0.58% to 1.37 on dollar strength.

- February jobs data due today, with unemployment rate consensus at 6.6% vs. 6.5% prior, eyed for BoC implications.

Yesterday's Recap

Canada's January trade balance showed a wider-than-expected deficit of -C$3.65 billion, exceeding the consensus of -C$0.9 billion and deteriorating from the prior -C$1.3 billion, driven by falling exports amid soft global demand. This underscored vulnerabilities in the export sector, especially energy and commodities, adding to market pressures. The S&P/TSX Composite Index ended down 0.84% at 32,840.60, dragged by energy losses as WTI Crude declined 2.09% to $93.73 and Brent Crude fell 1.36% to $99.09.

USD/CAD climbed 0.58% to 1.37, reflecting CAD softness against a strong U.S. dollar, while EUR/CAD slipped 0.15% to 1.57. The Canada 10Y Government Yield increased 0.41% to 3.40%, indicating hawkish shifts, though the 2Y Yield edged down 0.06% to 2.25%.

Natural Gas rose 1.24% to $3.27 on supply factors. Gold dipped 0.33% to $5,098.80, while Bitcoin advanced 2.61% to $72,334.09, bucking the risk-off tone.

The Day Ahead

Focus today is on Statistics Canada's February labor market report, with the headline unemployment rate expected at 6.6% compared to 6.5% prior, possibly indicating easing job conditions amid economic challenges. Employment change is projected at +10,000, improving from January's -24,800, with details on full-time employment (prior +44,900), part-time (prior -69,700), and labor force participation (prior 65%) offering further workforce insights. Set for release at 4:30 ET, these high-impact figures could influence Bank of Canada policy expectations, particularly if they show increasing slack that might temper inflation.

Deviations from consensus could shift rate cut bets. No other key Canadian events are on tap, so attention remains on jobs data, with potential CAD and TSX volatility from global energy moves.

Other Economic Notes

Canada's economy faces ongoing inflation pressures from energy fluctuations, with CPI YoY at 2.32% as of March 2025, above the BoC's 2% target and hindering easing plans. The expanded trade deficit highlights export struggles in oil-reliant areas, amid volatile WTI and Brent prices that may strain fiscal balances. Geopolitical issues, including the Iran war, are stoking inflation worries and affecting CAD pairs.

(cont...)