Canada Macro Daily(Beta Mode)

Jobs Plunge, Rate Bets Cool

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,541.93 | -0.91% |

| USD/CAD | 1.37 | +0.39% |

| EUR/CAD | 1.57 | +0.06% |

| WTI Crude | 97.34 | -1.39% |

| Natural Gas | 3.08 | -1.69% |

| Gold | 5,004.00 | -0.96% |

| Brent Crude | 98.50 | -4.50% |

| Bitcoin | 73,682.15 | +1.23% |

| Canada 2Y Govt Yield | 2.25% | -0.06% |

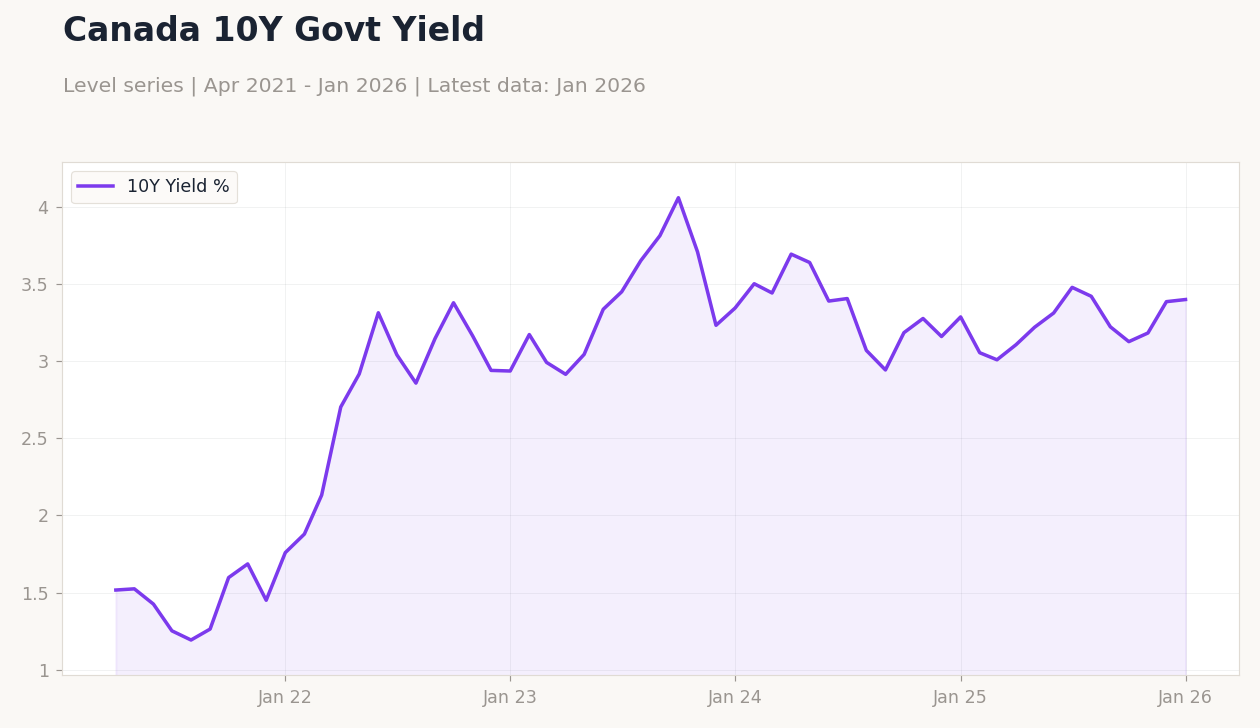

| Canada 10Y Govt Yield | 3.40% | +0.41% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada Unemployment Rate | Type: macro_line | Unemployment %: 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(6pt): 8.2,4.9,5.4,6.6,6.8,6.5

Canada Unemployment Rate | Type: macro_line | Unemployment %: 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(6pt): 8.2,4.9,5.4,6.6,6.8,6.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Housing Starts Level | 238,000 | 245,000 | 04:15 |

| Inflation Rate Year-over-Year | 2.30 | - | 04:30 |

| Core Inflation Rate Year-over-Year | 2.60 | - | 04:30 |

| Inflation Rate Month-over-Month | 0 | 0.60 | 04:30 |

| Wednesday (2026-03-18) | |||

| BoC Interest Rate Decision | 2.25 | 2.25 | 05:45 |

| BoC Press Conference | - | - | 06:30 |

| Friday (2026-03-20) | |||

| New Housing Price Index Month-over-Month | -0.40 | -0.30 | 04:30 |

| Retail Sales Excluding Autos Month-over-Month | 0.10 | 1.30 | 04:30 |

- Canadian economy shed 84,000 jobs in February, pushing unemployment to 6.7% and weakening CAD.

- Markets dipped with TSX down 0.91%, amid falling oil prices and rising bond yields.

- BoC rate hold expected Wednesday, clouded by job data and upcoming inflation figures.

Yesterday's Recap

Canadian markets closed lower yesterday amid disappointing February employment data, with the S&P/TSX Composite falling 0.91% to 32,541.93, pressured by losses in energy and materials sectors. The economy lost 84,000 jobs, far worse than expectations, driving the unemployment rate up to 6.7% and signaling labor market weakness that could influence Bank of Canada policy. USD/CAD strengthened 0.39% to 1.37, reflecting a softer loonie as rate cut bets increased on the jobs miss.

Energy prices weighed on sentiment, with WTI Crude dropping 1.39% to 97.34 and Brent Crude plunging 4.50% to 98.50, amid global supply concerns. Government bond yields diverged, with the 10-year rising 0.41% to 3.40% while the 2-year eased 0.06% to 2.25%, mirroring mixed inflation outlooks. Gold fell 0.96% to 5,004.00, and Natural Gas declined 1.69% to 3.08, adding to commodity-driven volatility in Canadian equities.

The Day Ahead

Today's calendar features key releases including Housing Starts at 04:15 ET, expected at 245,000 versus prior 238,000, which could signal housing sector resilience amid high rates. At 04:30 ET, February inflation data arrives, with YoY rate consensus absent but prior at 2.32%, and MoM expected at 0.6% from 0%; core YoY prior was 2.6%. These prints will be critical ahead of Wednesday's BoC decision, potentially swaying forward guidance on rates.

Wednesday brings the BoC Interest Rate Decision at 05:45 ET, consensus for hold at 2.25%, followed by a press conference at 06:30 ET. Friday rounds out the week with New Housing Price Index MoM expected at -0.3% and Retail Sales MoM at 1.5%, offering insights into consumer spending trends.

Other Economic Notes

Broader Canadian economic themes highlight labor market deterioration, with February's job losses exacerbating concerns over slowing growth and persistent unemployment at 6.7%. Housing affordability remains strained, as evidenced by upcoming starts and price index data, amid elevated mortgage rates and supply shortages. Energy sector dynamics, tied to volatile oil prices, continue to impact export revenues and inflation passthrough, with UBS warning of consumer squeeze from rising crude costs.